Part III.

Liberating the Captured Economy

By Brink Lindsey & Samuel Hammond

I n the previous section, we set forth an agenda for structural reform of the labor market. There, our commitment to a high road economy took center stage, as we made the case for a robust system of social insurance that invests in ordinary citizens’ capabilities and shields them from downside risks. At the same time, our distinctive approach prioritizes high performance, by reducing the frictions that depress workforce participation and slow down the transitions and reallocations necessitated by creative destruction.

While the previous section focused mainly on upgrading the public sector, in this section and the one that follows we shift our attention to a reform agenda for the private sector. Here the concern in the foreground is moving toward high performance – restoring the American economy’s dynamism, boosting innovation, and restoring vibrant growth in productivity and output. Meanwhile, though, the agenda we put forward also aims to lift us onto the high road, by fighting back against ill-gotten gains at the top and promoting dynamism that is both socioeconomically and geographically inclusive.

In the section that follows this one, we propose policy changes to improve the functioning of American capitalism – by providing necessary public goods, and sharpening incentives for entrepreneurship, competition, and innovation. But before we get to that, we must first attend to the grimier task of rooting out dysfunction. The object of reform here is reversing regulatory capture in key policymaking domains and unwinding the massive misallocations of resources that such capture has produced.

The Scale of the Problem

Before proceeding to policy recommendations, we want to begin by providing a better sense of the scale of the problem. Over the past few decades – at a time when American-style capitalism was widely touted as the model for the rest of the world to follow – the gap between that model and policy reality here in the United States was growing ever larger. The model was one of freewheeling, wide-open competition and creative destruction spurred by vigorous, unrestrained entrepreneurship; the emerging policy reality was one in which powerful insider interests progressively twisted the rules in their favor, inflating their own incomes by limiting and distorting competition and blocking entry by potential rivals.

The scale of the mismatch between model and reality can be seen in huge misallocations of resources afflicting vital sectors of the economy. We will focus here on what has gone wrong in three important sectors: finance, health care, and housing.

Finance

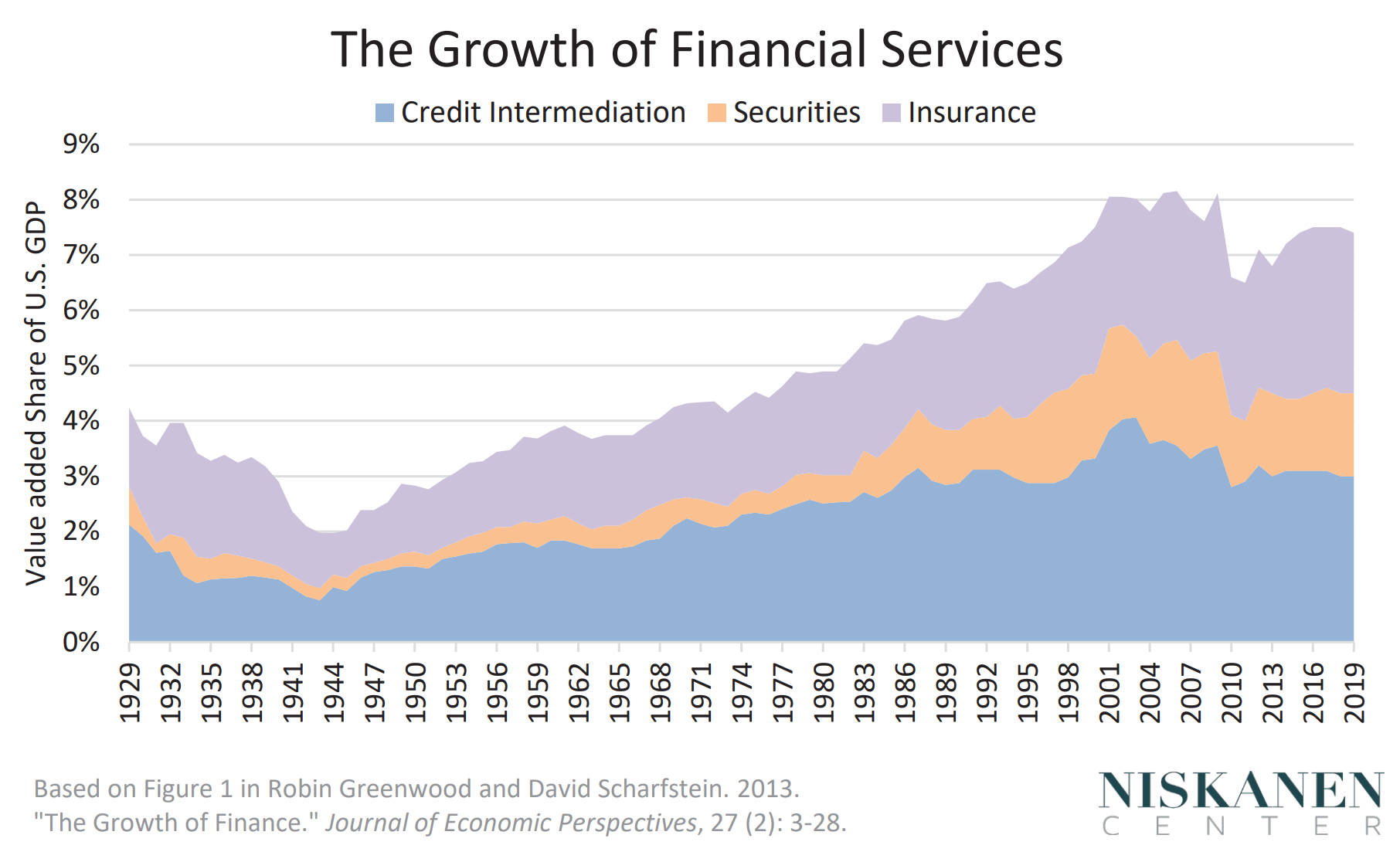

The U.S. financial sector has ballooned in recent decades: Its share of GDP rose from 4.9 percent in 1980 to 8.3 percent in 2006. [1] Although the sector took a big hit during the financial crisis, it has largely rebounded since. Meanwhile, the sector’s share of corporate profits spiked from around 10 percent in 1980 to 40 percent in the early 2000s; now it stands at around 30 percent. [2] During the run-up of "financialization," this growth was attributed to razzle-dazzle financial innovation and widely portrayed as a major American success story. Then came the collapse of the housing bubble and a financial meltdown that nearly cratered the global economy.

In the ensuing decade of disillusionment, evidence has mounted that the rapid growth of finance has been a colossal waste of resources. First, of course, there is the cost of the financial crisis. According to one Federal Reserve Bank estimate, the long-term price tag of the crisis in terms of reduced output ranges from $6 trillion to $14 trillion. [3] In terms of the needless suffering from mass foreclosures and job losses, and the subsequent derangement of politics by the rise of authoritarian populism, the larger price tag is incalculable. Meanwhile, cross-country research shows that when financial sectors grow too large (private credit in excess of 100 percent of GDP), there is a chronic drain on productivity and output growth due to misallocation of resources. [4] The United States stands well on the wrong side of that threshold, with private domestic credit close to 200 percent of GDP.

Although it’s a drag on the overall economy, financialization has been very good for people in finance. Back in 1980, workers with equivalent skills were making the same in finance as in other industries, but by 2006 jobs in finance were paying 50 percent more and top executives were making 250 percent more than their peers in other sectors. [5] Financial executives and professionals comprise 14 percent of the top 1 percent of earners, and 18 percent of the top 0.1 percent. [6]

The hypertrophy of finance was fueled by massive subsidies: subsidies for borrowing (e.g., the deductibility of interest payments), subsidies for saving (e.g., 401(k) and 529 plans), and most importantly, subsidies for financial institutions in the form of an elaborate safety net, both formal (access to the Fed discount window, deposit insurance) and informal (ad hoc bailouts). Financialization is typically portrayed as the result of deregulation, and it’s true that removing interest rate caps and branching restrictions on banks did allow and encourage expansion and financial "innovation." But allowing financial institutions to move into new activities and run greater risks within a larger regulatory framework of crisis-prone leverage and safety-net-induced moral hazard is emphatically not a move in a pro-market direction. On the contrary, it’s an engraved invitation to gamble with taxpayers’ money. [7]

Health care

The U.S. health care system is notorious for its runaway spending, now accounting for just under 18 percent of GDP. By way of comparison, health expenditures in other rich democracies typically comprise around 10 or 11 percent of GDP – with treatment outcomes generally comparable to those here, and with average life expectancies years longer than ours. It should come as no surprise, then, that America’s profligate health care system includes enormous amounts of waste – spending that is either ineffective or affirmatively counterproductive in advancing patient welfare. According to the most recent in-depth study, the amount of money wasted every year ranges from $760 to $935 billion – or roughly 25 percent of total spending. [8] Earlier studies found waste ranging from 30 to 35 percent of the total. [9]

This prodigious waste works out very well for doctors, as they constitute nearly 16 percent of the top 1 percent of earners. [10] Among American physicians and surgeons, some 31 percent make it into the top 1 percent – the best odds of any of the 480 occupational categories for which records are kept. [11]

The health care system’s fundamental design flaw is that it was designed by physicians to maximize their professional autonomy and incomes rather than high-quality and cost-effective care for patients. Decades before the federal government began paying for health care through Medicare and Medicaid, state governments were busy regulating it – at the behest and for the benefit of doctors. State licensing laws gave the medical profession numerous mechanisms for boosting physicians’ incomes by limiting supply: first, requiring doctors to complete four years of college and then four years of medical school (in many advanced countries you can save two years by getting a six-year medical degree immediately after high school); second, limiting the number of medical schools through the American Medical Association’s authority to grant accreditation; third, requiring completion of a U.S. residency (many other advanced countries recognize residencies completed abroad); fourth, requiring would-be doctors to pass a state licensing exam; and finally, defining the scope of medical practice so broadly as to give doctors a monopoly over many tasks that do not remotely require such rigorous training and screening. [12]

Not satisfied with controlling supply, the medical profession succeeded during the middle decades of the 20th century in systematically suppressing the emergence of group practices in which doctors were paid fixed salaries and patients charged flat annual fees. Further, they succeeded in getting almost all states to ban the corporate practice of medicine – that is, to make it illegal for nonphysicians to manage doctors in the practice of medicine. The medical profession thus succeeded in preserving the fee-for-service payment model that is at the root of so much unnecessary and ineffective medical treatment. [13]

As medical progress yielded an ongoing proliferation of new, useful, and highly expensive treatments, third-party payment – first by private insurance companies, and then by the federal government – gradually assumed the central role in financing health care. But since the health care system that was the beneficiary of these new sources of funding was organized to systematically suppress incentives for cost-effectiveness, the result has been double-barreled dysfunction. First, of course, health care spending has skyrocketed – increasing six-fold on an inflation-adjusted, per capita basis since 1970, and rising from under 7 percent of GDP back then to nearly 18 percent today. Second, a big and growing chunk of that spending goes to never-ending administrative warfare between insurance companies trying to contain costs from the outside and providers bent on maximizing payments. American consumers and taxpayers now spend nearly five times as much per capita on health care administrative costs as do the citizens of other rich democracies, as keeping up with the blizzard of paperwork now employs one billing professional for every two doctors. [14]

Another important source of wasteful health care spending and unjust enrichment at the top can be found in the pharmaceutical industry. Drug makers are able to game the U.S. patent system to extend patent monopolies far beyond their normal 20-year terms. A study of the nation’s 12 top-selling drugs reveals an average of 71 patents granted per drug and 38 years of attempted patent protection. Prices for these drugs have shot up by 68 percent on average since 2012. [15] Pharmaceutical companies also exploit cumbersome FDA regulations on approving generic drugs to exclude competition and jack up prices – recall the recent scandals over Martin Shkreli and Daraprim, and Mylan’s extortionate price hikes for EpiPens. Big Pharma’s skill at regulatory capture translates into abnormally high returns, with profit margins for the industry averaging above 17 percent. [16]

Housing

A third gross distortion of the U.S. economy brought about by regulatory capture involves housing. Here the sacrifice of economic sanity has taken the form of death by a thousand cuts. Local control over zoning and land use, and the capture of that control by "NIMBY" ("not in my back yard") interests opposed to new housing construction, have resulted in a housing availability crisis in many American cities – as well as environmentally noxious sprawl and morally noxious racial and socioeconomic segregation.

Zoning has been widespread in the United States for the better part of a century, and its exclusionary effects have been central to its political appeal from the outset. Until recently, though, zoning’s major impact was in determining where housing would be located in a given metro area – not how much of it would be built. Since the 1970s, though, tighter limits on land use combined with exhausted opportunities for sprawl have imposed an increasingly restrictive constraint on new housing supply, especially in big coastal cities, resulting in a dramatic run-up in housing prices. Artificial scarcity created by withholding permission to build now accounts for some 20 percent of the price of housing in Washington, D.C., and Boston; 30 percent in Los Angeles and Oakland; and 50 percent in San Francisco, San Jose, and Manhattan. [17]

Just as this dynamic got underway, these same big coastal cities became the engines of America’s information economy. Attracting increasingly high concentrations of college-educated workers, these "human capital hubs" now boast the country’s highest incomes and fastest productivity growth. Yet because of sky-high housing prices, many people who would otherwise have moved there – and who could have bettered their condition considerably by doing so – have not. The result has been the breakdown of regional economic convergence and the emergence of stark geographic inequality, especially along the urban-rural divide. And this breakdown, in turn, has led to a growing spatial misallocation of America’s population – not enough people in the country’s most dynamic and productive places. The cost of this spatial mismatch is staggering – several percentage points of GDP, according to various estimates. [18]

Here again, what’s bad for the country as a whole has been immensely beneficial for a narrow group of insiders – in this case, incumbent homeowners in high-price markets. Windfall gains created by regulatory moats around the most desirable places to live have been an important driver of rising wealth inequality. [19] Indeed, there is strong evidence to suggest that the rise in capital’s share of national income is due entirely to zoning-fueled appreciation of housing wealth. [20]

The brief case studies provided above suffice to demonstrate just how serious the problem of regulatory capture has become, and it should be noted that the problem crops up in many other sectors as well. To liberate the captured economy and restore free and open competition where it has been systematically twisted and squelched, we propose here a four-part agenda: (1) shrink the bloated financial sector; (2) roll back "intellectual property" excesses; (3) improve access to health care through supply-side reforms to boost competition; and (4) reduce regulatory barriers to new housing.

Shrink the Bloated Financial Sector

Prior to the financial crisis, the rapid growth of finance was widely heralded — by policymakers, economists, and of course industry representatives — as a glittering success story. Supporting that assessment was an impressive body of economic scholarship showing a strong correlation between the size of a country’s financial sector and the size and growth rate of its overall economy. [21]

In the aftermath of the economic ruin and political convulsions that followed the crisis, we now know that those earlier findings are in need of a critical qualification. Namely, they emerged from analysis that focused largely on poorer, less developed economies. In those countries, deliberate financial repression through interest rate caps along with unreliable legal systems combine to stymie financial development and prevent the fertile union of money and good ideas. But this state of affairs is dramatically different from conditions in rich countries like ours: In the world’s lowest-income countries, private bank lending amounts to only 11 percent of GDP, compared to 87 percent in the highest-income countries.

This earlier literature does confirm that financial sectors can indeed be too small. But what has become clear since the collapse of the housing bubble is that advanced economies can face the opposite problem: financial sectors that are excessively large. Recent research reveals that, across the span of economic development, the relationship between financial sector size and economic performance is shaped like an inverted U. According to one estimate, once total private credit goes past the sweet spot of around 100 percent of GDP, further expansion starts to become counterproductive. [22] In the United States, that ratio is now above 185 percent – down only slightly from its 2007 peak, when it surpassed 200 percent. [23]

Moving past this aggregated analysis and looking at the details of U.S. financial sector growth only strengthens the conclusion that this growth has been excessive. The main drivers of U.S. financial sector expansion were dramatic run-ups in (1) household credit, in particular residential mortgages, and (2) assets under active management. [24] The former, of course, ended in disaster, and there is strong evidence more generally, in research looking at dozens of countries over a 50-year period, that rising household debt is a harbinger of reduced GDP growth and higher unemployment. [25] In particular, the diversion of resources into mortgage-financed single-family housing not only carries the risk of financial meltdown, but also sustains and deepens a misbegotten dependence on home ownership for wealth-building, and with it a host of social ills — among them, environmentally harmful sprawl, racial and socioeconomic segregation, runaway housing prices in much of the country, and elevated wealth inequality. [26] As to the latter, the sizeable fees extracted from investors are inevitably a collective waste of money, as they are premised on promises to beat the market that cannot be realized for the market as a whole. Yes, deep and liquid credit and capital markets are vital fuel for economic progress — but not this kind of credit, not these kinds of markets.

America’s bloated, crisis-prone financial sector is sustained by massive government subsidies – including tax preferences for debt, tax preferences for savers that disproportionately benefit the well-off while boosting business for asset managers (e.g., 401(k) retirement plans and 529 college savings plans), and a raft of subsidized loan programs. But the biggest and most pernicious subsidy is inherent in the basic design of the U.S. financial regulatory system.

At the root of the problem is financial institutions’ extreme reliance on debt financing, with debt-to-asset ratios well in excess of 90 percent as the industry norm. This level of debt dependency is inherently destabilizing, making financial firms highly vulnerable to both liquidity and insolvency crises. Unfortunately, the regulatory system is premised on the assumption that extreme leverage is natural, unavoidable, and even desirable. So rather than eliminating this fundamental cause of financial instability, policymakers have chosen to try to regulate around it with detailed controls on the risks that financial institutions can take. Over the long run, such regulation resembles putting a lid on a pot while leaving the burner on high: Sooner or later, the lid will get knocked off and the pot will boil over. [27]

To rein in our run-amok financial sector and steer the economy away from debt dependency and chronic misallocations of resources, we need to unwind the subsidies that have brought us to this pass. To that end, the highest priority is to impose strong capital requirements on financial institutions. There are many attractive reform proposals in circulation [28] , but the necessary elements of effective reform include (1) a requirement that banks hold equity capital equal to at least 20 percent of assets, and (2) anti-circumvention rules that either tax or ban outright the use of short-term debt financing by nonbank or "shadow" financial institutions.

At the same time as we are trying to limit leverage within the financial system, we should be undertaking reforms that reduce debt dependency in the rest of the economy and constrict the flow of funds into a volatile system whose excessive size contributes to its undue and destructive influence over policymaking. The most obvious step toward this end is to eliminate, or reduce as much as possible, both the general tax preference for debt and the specific tax preference for mortgage debt.

Beyond that, there is a strong case to be made for some kind of public option for savings and checking accounts. One promising proposal, advanced by Vanderbilt University law professor Morgan Ricks, is to allow individuals, businesses, and other private institutions to maintain bank accounts with the Federal Reserve. [29] As Ricks and co-authors point out, banks currently hold such accounts, which pay higher interest than commercial banks and allow for instantaneous clearance of payments. Considerations of horizontal equity thus favor extending this advantageous privilege, now exclusively enjoyed by banks, to the rest of us. Beyond leveling the playing field, a public banking option would be a boon for the 25 percent of U.S. households who are now unbanked or underbanked. [30] Access to central bank accounts with no fees and no minimum balances would give these households the conveniences and advantages of banking that the rest of us take for granted, thereby helping to integrate them better into the market economy.

Finally, there are important considerations of political economy at play here. One important reason for the financial lobby’s outsized political influence is commercial banking’s inextricable connection to the payments system on which the day-to-day functioning of the American economy depends. A public option, with terms that commercial banks would find difficult to match, would reduce deposits with commercial banks, thereby serving to attenuate the systemic risks posed by bank failures and thus the leverage that the financial lobby has to demand bailouts and other subsidies.

Roll Back "Intellectual Property" Excesses

Protection of patents and copyrights in this country dates back to the dawn of the republic. "To promote the progress of science and the useful arts," the Constitution expressly authorizes Congress to "secur[e] for limited times to authors and inventors the exclusive right to their respective writings and inventions." Congress moved quickly to exercise that authority, enacting both the first Patent Act and first Copyright Act in 1790. For nearly two centuries, these laws provided modest protections that allowed authors and artists to make a living from their work and encouraged inventors to bring new products to market and, through disclosure requirements, share their innovations with the public.

In the past few decades, however, patent and copyright laws have been transformed beyond recognition. Longstanding limits on the scope and duration of the exclusive rights they provide have been systematically shredded. For copyright, terms have now been extended for generations past the life of the author; the elimination of registration requirements and other formalities means that everything written down is now copyrighted; and digital anti-circumvention rules have gutted the preexisting right to fair use. For patents, expanding definitions of what can be patented and increasingly lax standards for granting patents have boosted the annual number of patents granted nearly fivefold since the early 1980s. The results of these dramatic changes are an utter perversion of the laws’ original purposes. Far from incentivizing creative works and technological innovation, the primary effects of these laws at present are to generate massive windfalls for giant corporations in heavily concentrated industries, legal uncertainty for actual artists and innovators, and exposure to maddening and expensive shakedowns for purchasers and users of copyrighted and patented products.

The reckless mission gallop at work here has been greatly aided by the simultaneous rise in popularity of the term "intellectual property" to describe patents and copyrights. This rhetorical coup allows interest groups seeking what amount to legally enforced (if temporary) monopolies to grab an undeserved moral high ground. They are able to claim that they are merely defending their rightful due against "theft" and "piracy," while portraying any effort to push back against their rent-seeking as an attack on the very institution of private property itself.

But the argument that patents and copyrights are analogous to private property in physical objects is extremely weak. Physical property is an elegant and extremely robust solution to an unavoidable problem: how to allocate rights over scarce goods whose use, consumption, and control are inherently rivalrous. Ideas, by contrast, are nonrivalrous: If I use a recipe to bake a cake, or a formula to solve an equation, or sheet music to play a song, I have done nothing to diminish others’ ability to do likewise. Accordingly, creating exclusive rights over ideas, rather than allocating naturally occurring scarcity, creates artificial scarcity where none existed before. For other types of this kind of "property," think taxi medallions – or the old robber barons of the Rhine, who strung big cables across the river to stop passing ships and hold them up for tolls.

Another way of saying that patents and copyrights create artificial scarcity is that they make everybody poorer – specifically, by depriving them of access to things that would otherwise be freely available. The only justification for doing this is that it provides some larger public benefit. And indeed, that justification can apply to patents and copyrights: Without exclusive rights, artists and inventors would sometimes be unable to earn sufficient returns from even commercially successful products to recoup their investments and make their efforts economically viable. The promise of patents and copyrights, then, is a greater level of artistic creation and technological innovation than would otherwise be the case.

But this promise holds only under quite narrow circumstances – when considerations of commercial gain (as opposed to, say, artistic self-expression) predominate, when the costs of innovation are relatively high but the costs of imitation are relatively low, and when other methods of monetizing one’s work (e.g., through live concerts for recording artists, or service contracts for software developers) are insufficient. Remember, all that is needed to solve the incentive problem is sufficient returns to justify the effort; anything beyond that is, in economists’ parlance, a rent. Patent and copyright laws in their current state, having pushed monopoly privileges far past sufficiency and well into wretched excess, are thus paradigmatic cases of rent-seeking.

The harms caused by patent and copyright overreach are widespread and substantial. In the case of pharmaceuticals, drug companies game the system by piling up patents for trivial and therapeutically irrelevant "innovations," allowing them to extend monopoly privileges – and the ability to raise prices – well beyond the intended 20-year term. [31] For software, the direct costs every year of defending infringement suits from so-called "nonpracticing entities" – better known as patent trolls – come to more than 10 percent of total annual R&D spending by all U.S. businesses. [32] Copyright law, which is supposed to give us more creative works to enjoy, regularly suppresses and blocks them: To cite just one jarring example, Amazon offers more books from the 1850s than from the 1950s, because copyright keeps so many of the latter out of print. [33] Meanwhile, anti-circumvention rules hinder everyone from farmers to soldiers in making needed repairs to equipment with copyrighted software. [34]

Over the long term, the stakes will only get higher. The defining feature of today’s knowledge economy is that ideas and know-how have supplanted land and physical plant and equipment as the predominant and most important form of wealth. Continuing the trend we are now on, and locking up ever greater shares of this wealth to be exploited by a privileged few at the expense of the rest of us, is a recipe for stagnation and plutocracy. It is imperative that we reverse course.

Doing so will not be easy. Patent and copyright lobbies have succeeded not only in perverting U.S. law, but in enshrining those perversions in multiple treaties and international agreements. But however difficult the path, here are some of the most important steps toward restoring sanity to this area of the law:

- End the patentability of software and business methods. Such patents suffer a fundamental defect, in that the scope of what is protected is necessarily described by abstract language whose extent cannot be known ahead of litigation. A system of "property" where nobody knows where the boundaries are is not a system at all; it is chaos. The muddle we have today may be great for patent trolls and their lawyers, but it’s bad for everybody else.

- Require that new pharmaceutical patents can be granted only for drugs that represent a substantial therapeutic advance over existing medicines. This would end the current practice of creating patent thickets for trivial improvements (e.g., a one-a-day pill instead of a two-a-day pill, a capsule instead of a tablet) that work to extend monopoly privileges beyond the intended 20-year term.

- Remove financial incentives for lowering patent standards. The U.S. Patent and Trademark Office is a fee-funded agency, which means that it receives more revenues for issuing more patents. These unhealthy incentives need to be eliminated by making the USPTO’s funding independent of patenting activity. At the same time, there is a need for healthy budget increases for USPTO, as current underfunding means too few examiners and thus the inability to scrutinize applications appropriately.

- Dramatically shorten copyright terms. The original U.S. law provided for a 14-year term with the option for a single 14-year extension. Research shows that the incentive benefits of anything longer than this are minimal.

- Restore copyright registration requirements to eliminate the problem of orphan works. As an alternative, institute a system of nominal copyright taxes under which failure to pay leads to reversion to the public domain.

- Revoke the Digital Millennium Copyright Act’s anti-circumvention rules. At the very least, modify those rules to guarantee the right of owners to repair products as they see fit.

Improve Access to Health Care through Supply-Side Reforms to Boost Competition

The decades-long national debate over improving access to health care has focused overwhelmingly on the issue of financing – in other words, on who pays the bills. Progressives, for whom accessible health care has long been a priority, have concentrated their efforts on making sure more people have insurance coverage – in particular, by expanding the government’s provision of such insurance.

Along the way, there has been much less attention to why the bills are so high. Or rather, that question has been treated as subsidiary to the more fundamental issue of who pays. The progressive assumption has been that a larger government role in providing health insurance will also solve the problem of high prices and runaway spending, first by eliminating duplicative administrative costs, and second by using government’s monopsony power to bargain down prices and refuse payment for treatments that aren’t cost-effective. The flimsiness of that assumption, though, is revealed by even a quick glance at the relevant history. After all, the United States has had single-payer health care for Americans 65 and older for more than a half-century now – precisely the period over which medical prices and spending have exploded. Recall, in particular, the annual spectacle of the "doc fix" earlier this century. As Medicare spending regularly exceeded the "Sustainable Growth Rate" set to tie spending increases to the rate of GDP growth, Congress would dutifully rush in to appropriate extra money instead of allowing cuts in payments for physician services.

Here then is the lesson of experience: If health care providers have captured the system for determining how medical care is paid for, expanding the government’s role in paying the bills will not succeed in getting those bills under control, and indeed will undermine the case for social insurance because of the hemorrhaging red ink it leads to.

As discussed earlier in this paper, we support a robust system of public health insurance that delivers universal access to health care. We do not believe, however, that it is either necessary or advisable for government to fully supplant private health insurance. Most well-functioning health systems around the world guarantee universal access without resorting to a single-payer model; and in the United States, with medical care organized as it currently is, a single-payer system would be fiscally disastrous. Our preferred approach, universal catastrophic coverage, focuses the government role on handling big-ticket expenses while allowing private insurance to deal with more routine items. This division of labor between the private and public sectors allows each to operate where it is most effective.

In our view, though, the most pressing priority in health care reform is putting downward pressure on the bills, not changing who pays them. Prices are too high, and too much of the care that is provided is wasteful. To address these ills, the most effective approach is to unleash competition – which health care providers have systematically throttled in order to pad their incomes. And where competition remains artificially weak, government must use its powers as purchaser and regulator to keep prices and spending from spinning out of control.

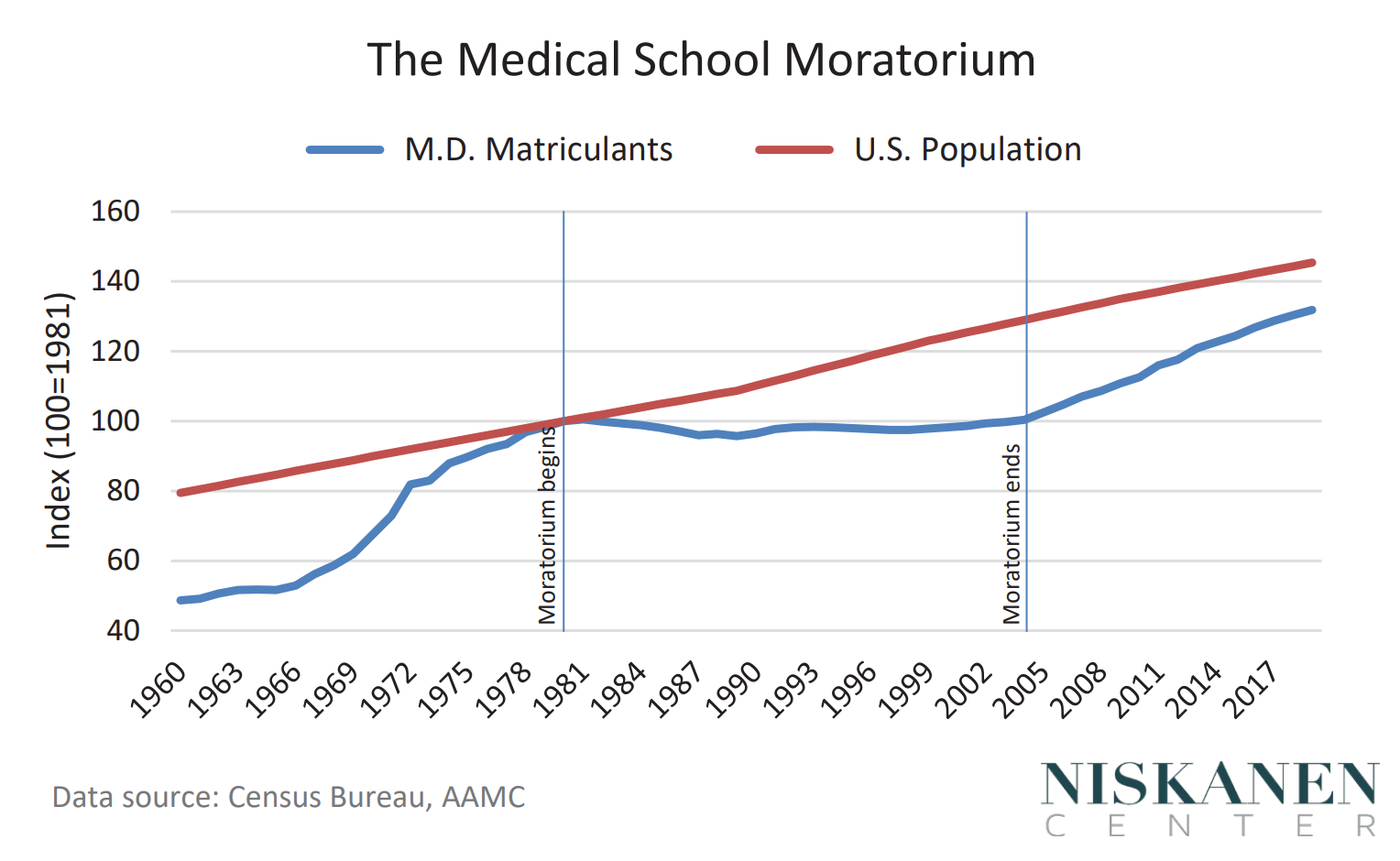

American doctors earn dramatically more than their peers in other countries, [35] and it is perhaps not coincidental that there are too few of them. There are 2.6 doctors per 1,000 people in the United States, as compared to 3.6 in Australia, 3.2 in France, 4.2 in Germany, and 4.2 in Switzerland. [36] The U.S. shortfall is no accident, but rather the result of deliberate policy: In particular, in response to bogus fears of a looming "physician surplus," the United States imposed a moratorium on expanding the number of medical school slots from 1980 to 2005. [37] Meanwhile, the Association of American Medical Colleges forecasts a growing shortfall of doctors relative to demand that could exceed 120,000 by 2032. [38] Against this background, it should be screamingly obvious that one promising way to make health care more affordable is to increase the supply of health care providers.

That supply is artificially suppressed by medical licensing laws. Under those laws, completion of a U.S. residency is with very few exceptions required before one can obtain a medical license. However, the number of residency slots funded through Medicare has been frozen for more than 20 years, so that available residencies have increased only 1 percent a year since 2002 even as the number of medical school slots has grown 52 percent over the same period. [39] The misguided freeze on residencies should be ended, but so too should the U.S. residency requirement. Canada, for example, allows residency training in select other countries – including Australia, Hong Kong, Singapore, Ireland, Switzerland, the United Kingdom, New Zealand, South Africa, and the United States – to substitute for completion of a Canadian residency for purposes of obtaining a medical license. [40] The United States should move in the same direction.

The available supply of health care providers can also be expanded by facilitating the delivery of services across state and national borders. Telemedicine holds out considerable promise for increased convenience and expanded treatment options, eliminating unnecessary and time-consuming office visits and extending high-quality care to patients in remote areas. Numerous regulatory barriers, however, thwart the realization of telemedicine’s potential, including state-based licensing that prevents a doctor from serving patients in other states and in some cases requires in-person meetings with patients. These barriers need to be eliminated, and the federal government can play a constructive role in encouraging mutual recognition of licenses and repeal of anti-competitive restrictions.

Access to cost-competitive outside suppliers could also be improved by allowing private insurers and Medicare to establish reference pricing that pays patients to travel out of state to receive less expensive care or else apply that lower reimbursement amount plus the travel allowance to the cost of local care. This same system could be extended internationally to encourage medical travel abroad to appropriately certified facilities. [41]

Of all options to expand supply and increase competition in the provision of health care services, probably the lowest-hanging fruit is to end state-level scope-of-practice restrictions that prevent mid-level health care professionals – nurse practitioners, dental hygienists, optometrists, midwives – from operating independently. [42] Here the main responsibility for reform lies with the states, but federal authorities can use funding levers to push states in the right direction.

Hospital care is currently the single biggest item in the U.S. health care budget, accounting for 33 percent of total spending. [43] Here again, prices in the United States are abnormally high: According to one recent estimate, the average cost per day of hospital stays is 2.6 times higher than the OECD average. [44] And once more, problems of weakened and suppressed competition play a big role in jacking up prices and spending.

A merger wave that took off in the 1990s and then never stopped has produced a highly concentrated industry led by regional hospital chains with considerable market power. The median market’s Herfindahl-Hirschman Index (a leading measure of market concentration) as of 2013 stood at 2,800 and rising, up from 1,600 in 1990. According to the Federal Trade Commission, industries with an HHI score of 2,500 or above are considered highly concentrated. This growing market power translates into higher prices: A 2011 study found that prices for six widely used procedures averaged 44 percent higher in more concentrated hospital markets. [45]

The market power gained through mergers has been consolidated and buttressed by various anti-competitive laws at the state level. Certificate-of-need laws inhibit the building of new hospitals, while "any willing provider" and "network adequacy" laws force insurers to contract with hospitals regardless of how much they charge – thus undermining insurers’ bargaining power over prices.

The first step in bringing competition back to the hospital sector is to make further mergers much more difficult. Doing so will require substantial additions to the Federal Trade Commission’s staff and resources. Although necessary, closing the barn door alone is insufficient when so much of the herd has already escaped. Accordingly, we need something along the lines of a proposal advanced by the Foundation for Research on Equal Opportunity: Hospital chains in markets above some threshold of market concentration would be required either to divest holdings to bring concentration below that threshold or else have payments capped at the median rate paid by a Medicare Advantage plan in that region. In addition, the federal government should use its funding leverage to encouragschare states to repeal the anti-competitive laws that prop up hospitals’ market power. [46]

Drug makers, like physicians and hospitals, are too often able to overcharge because of restrictions on competition. Earlier in this paper we addressed the major barrier to competition in pharmaceuticals – patents and the temporary monopolies they confer – and suggested reforms that could mitigate problems of patent abuse. But even when drugs go off-patent, the Food and Drug Administration grants additional monopolies to producers of generic drugs under certain circumstances – for example, in the case of "orphan drugs" for rare diseases and drugs that were originally on the market before the FDA’s regulatory authority kicked in. And sometimes surrounding patents on the manufacturing process or drug delivery device continue to inhibit competition from new suppliers. Although in general the U.S. generic drug market is a big health-policy success story (between 80 and 90 percent of all U.S. prescriptions are now for generic drugs at significantly lower prices than the branded competition), regulatory barriers do cause big problems in certain cases – recall the outrageous price hikes for Daraprim by Martin Shkreli’s Turing Pharmaceuticals and for EpiPens by Mylan. Meanwhile, the relatively straightforward process for approving generic small-molecule drugs does not exist in the case of large-molecule biologics. Approval for generic "biosimilar" alternatives requires extremely expensive Phase III clinical trials not needed for small-molecule generics. As a result, biosimilars typically sell for only a modest 10-20 percent discount, while the introduction of small-molecule generics regularly leads to price declines of 80 percent. [47]

Although there are various tweaks that could improve the FDA’s regulation of generics and biosimilars, by far the most effective policy response would be to allow importation and sale of any drugs approved in other advanced countries. [48] Full-fledged reciprocity is the cleanest and best approach, but a more modest move in the right direction would be to permit importation only in designated circumstances – specifically, when U.S. drug prices exceed certain thresholds.

There is no way to sugarcoat the political difficulty of actually delivering on the kinds of supply-side reforms discussed here. It is probably no accident that most of the energy in health care reform has been directed toward financing: Insurance companies make for much more inviting political targets than doctors, hospitals, and drug makers. Doctors regularly top polls as the most admired profession in the country; hospitals are large and fast-growing employers who frequently serve as anchors for local economies; drug makers may not enjoy the popular support that doctors and hospitals can count on, but they do have very deep pockets and long experience in playing the Washington game. Accordingly, providers’ lobbies have a great deal of political muscle, and over the years they have made clear they are willing to flex it with ferocity. But however daunting the challenge that confronts us, there is simply no alternative to making the effort. The only way to restore sanity to the American health care system is to somehow make it through the buzz saw of provider opposition.

Reduce Regulatory Barriers to New Housing

Regulatory restrictions on the construction of new housing are typically imposed at the local level, but their effects scale up to a series of serious nationwide problems. Housing affordability is a major concern [49] across extensive stretches of the country: The home ownership rate for young adults is at the lowest point in decades [50] ; roughly two-fifths of renters pay 50 percent or more of their income for housing [51] ; and homelessness is on the rise again in recent years, driven by a surge in California. [52] Misallocation of the population away from the country’s most productive cities is reducing total U.S. economic output by multiple percentage points every year. [53] Land use restrictions contribute to racial and socioeconomic segregation [54] and limit access to high quality public schools, [55] reducing opportunities and discouraging upward mobility for minorities and other disadvantaged groups. Finally, zoning’s artificial restrictions on density exacerbate urban sprawl, thereby worsening the problems of climate change by increasing transit-related carbon emissions. [56]

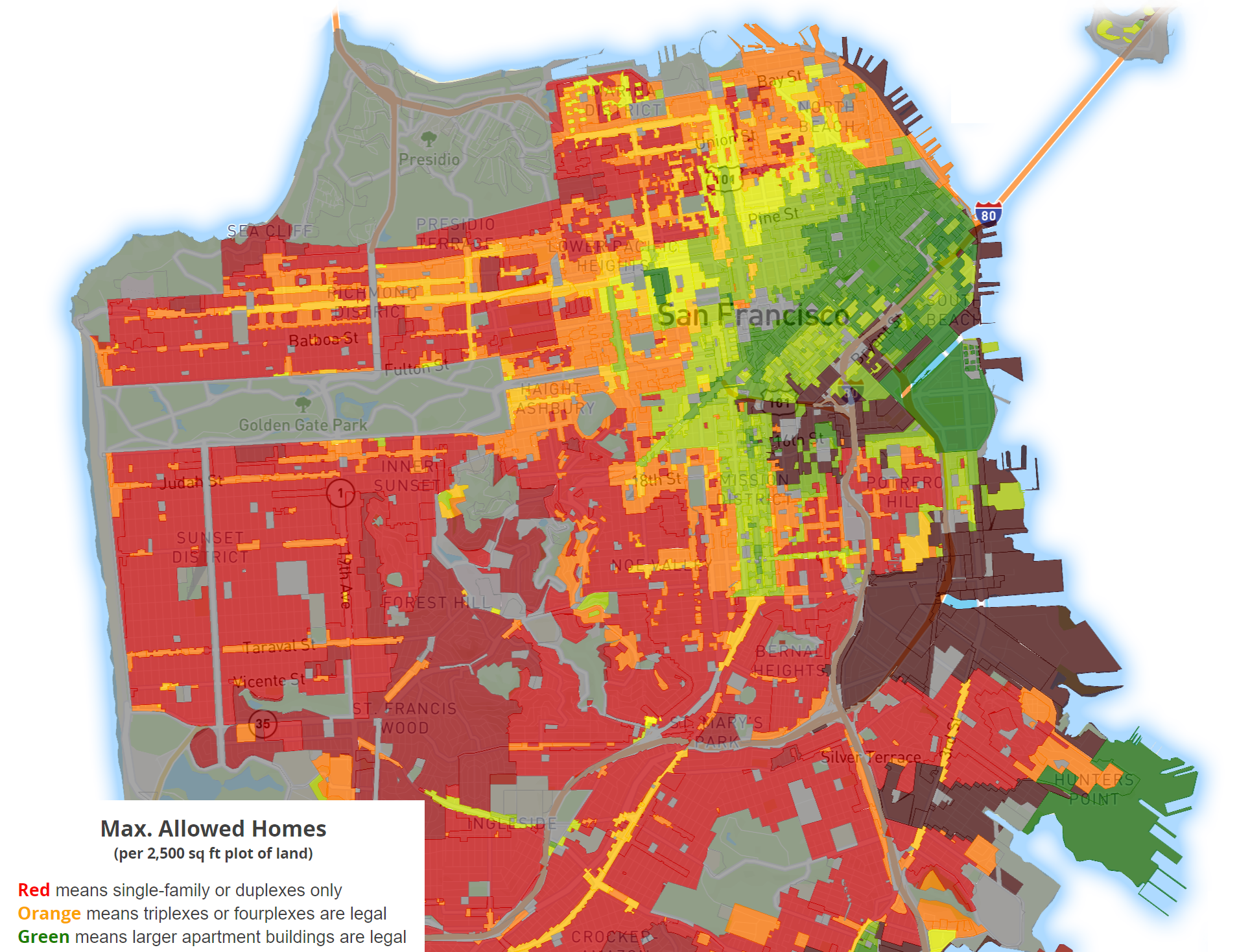

SFzoning.deapthoughts.com

It is tempting to moralize the land use issue by blaming everything on existing homeowners and their narrow-minded "NIMBY" ("not in my back yard") attitudes. After all, the strong bias of homeowners against new construction nearby – because of concerns over the disruptions of construction, increased congestion, and effects on neighborhood amenities and property values – is the primary political force in opposition to new housing, and its formidable muscle all too often carries the day. But although homeowners’ attitudes may sometimes be tainted by unsavory preferences for racial and socioeconomic exclusivity, by and large their anti-construction bias is completely understandable. For most homeowning households, their residence is their largest single asset and comprises the vast bulk of their net worth; and for all of them, it’s home, a place freighted with personal meaning and family significance. It is to be expected, therefore, for homeowners to take a skeptical view of any changes that could negatively impact their financial position and broader well-being.

The problem isn’t the narrowness of homeowners’ interests. The problem, rather, is that the current structure of land use decision-making gives massively disproportionate influence to those narrow interests. Local control over land use, combined with the hyperlocal (i.e., plot by plot) basis on which decisions to permit or prohibit new construction are typically made, ensures that NIMBY concerns are greatly overweighted relative to all the other interests that are affected. The solution, therefore, is to shift the locus of decision-making upward – from hyperlocal to metro-wide, from city to state, and even from the state level to the federal level.

This general principle suggests reform possibilities at all levels of government. At the municipal level, Minneapolis has led the way with pathbreaking reform. With its "Minneapolis 2040" plan, initially approved in December 2018, the city has taken the bold step of eliminating single-family zoning throughout the city. Of course, this does not mean that single-family homes are no longer allowed – far from it. Rather, it means there are no longer lots on which only single-family homes can be built; duplexes and triplexes are now permitted citywide. In addition, the plan opens the way for greater density by allowing three- to six-floor apartment buildings near transit stops while also eliminating off-street minimum parking requirements that work to jack up housing costs. [57]

At the state level, Oregon followed Minneapolis’s lead in July 2019 with legislation to end exclusive single-family zoning throughout the state. In cities with more than 25,000 people, the law allows duplexes, triplexes, fourplexes, and "cottage clusters" to be built on lots previously reserved for single-family homes; duplexes are now allowed in cities between 10,000 and 25,000 people. [58] Similar bills have also been introduced recently in Virginia and Maryland. [59] Under the leadership of state Sen. Scott Wiener, a major bill in California to allow greater density near transit and in affluent areas has thus far failed to make it through the legislature but has attracted significant support and made increasing headway over time. [60] Meanwhile, more modest reforms – to allow auxiliary dwelling units (otherwise known as "ADUs" or "mother-in-law flats") and to speed up permitting of new construction – have passed in California. [61]

Although Washington has traditionally deferred to states and localities on issues of municipal land use, that deference is now being actively reconsidered – to which we say, the sooner the better. It has become clear in recent years that local land use policy has important ramifications at the national level for GDP growth, wealth inequality, and prospects for upward mobility – and at the global level for carbon emissions and climate change. Accordingly, the federal government can no longer afford to sit idly by as unchecked NIMBYism undermines the national interest on multiple fronts.

The most straightforward way for federal policy to encourage more liberal rules for new housing is through leveraging funding for urban development. This is the approach taken in the bipartisan Yes In My Back Yard (YIMBY) Act introduced in both houses of Congress in 2019. This bill would condition eligibility for federal Community Development Block Grant funding on local governments’ identifying and eliminating zoning and permitting policies that hinder new construction. This basic approach could be followed in various permutations to incentivize needed reforms at the local level.

Endnotes

[1] Robin Greenwood and David Scharfstein, " The Growth of Finance ," Journal of Economic Perspectives, Vol. 2, no. 2, pp. 3-28, Spring 2013.

[2] Jordan Weissmann, " How Wall Street Devoured Corporate America ," The Atlantic, March 5, 2013.

[3] David Luttrell et al., " Assessing the Costs and Consequences of the 2007-09 Financial Crisis and Its Aftermath ," Federal Reserve Bank of Dallas Economic Letter, Vol. 8 no. 7, September 2013.

[4] Stephen G. Cecchetti and Enisse Kharroubi, " Reassessing the Impact of Finance on Growth ," Bank of International Settlements Working Paper no. 381, July 2012.

[5] Thomas Philippon and Ariell Reshef, " Wages and Human Capital in the U.S. Financial Industry: 1909-2006 ," Quarterly Journal of Economics, Vol. 127, no. 4, pp. 1551-1609, November 2012.

[6] Jon Bakija et al., " Jobs and Income Growth of Top Earners and the Causes of Changing Income Inequality: Evidence from U.S. Tax Return Data ," April 2012.

[7] See Brink Lindsey and Steven Teles, The Captured Economy: How the Powerful Enrich Themselves, Slow Down Growth, and Increase Inequalit y (New York: Oxford University Press, 2017), pp. 35-63; Brink Lindsey and Steven Teles, " The Regulatory Subsidy for Extreme Leverage: A Reply to Mike Konczal ," Niskanen Center, January 23, 2018.

[8] William Shrank et al., " Waste in the US Health Care System: Estimated Costs and Potential for Savings ," JAMA, Vol. 322, no. 15, pp. 1501-1509, October 15, 2019.

[9] See Donald Berwick and Andrew Hackbarth, " Eliminating Waste in US Health Care ," JAMA Vol. 307, no. 14, pp. 1513-1516, April 11, 2012 (waste estimated at 35 percent of total spending); The Healthcare Imperative: Lowering Costs and Improving Outcomes: Workshop Series Summary (Washington, DC: Institute of Medicine of the National Academies, 2010) (waste estimated at 31 percent of total spending).

[10] Bakija et al., " Jobs and Income Growth of Top Earners ."

[11] See Jonathan Rockwell, A Republic of Equals: A Manifesto for a Just Society (Princeton, N.J.: Princeton University Press, 2019), pp. 244-245..

[12] See Lindsey and Teles, The Captured Economy , pp. 100-105; Robert Orr, " U.S. Health Care Licensing: Pervasive, Expensive, and Restrictive ," Niskanen Center, May 12, 2020.

[13] See Rockwell, A Republic of Equals , pp. 251-253.

[14] See ibid., p. 254.

[15] " Overpatented, Overpriced: How Excessive Pharmaceutical Patenting Is Extending Monopolies and Driving Up Drug Prices ," I-MAK, August 2018.

[16] U.S. Government Accountability Office, " Drug Industry Profits, Research and Development Spending, and Merger and Acquisition Deals ," November 2017.

[17] See Lindsey and Teles, The Captured Economy , pp. 109-123; Edward Glaeser et al., " Why Is Manhattan So Expensive? Regulation and the Rise of Housing Prices ," Journal of Law and Economics Vol. 48, no. 2, pp. 331-69, October 2005.

[18] See Edward Glaeser and Joseph Gyourko, " The Economic Implications of Housing Supply ," Journal of Economic Perspectives Vol. 32, no.1, pp. 3-30, Winter 2018; Kyle Herkenhoff et al., " Tarnishing the Golden and Empire States: Land-Use Restrictions and the U.S. Economic Slowdown ," National Bureau of Economic Research Working Paper no. 23790, September 2017; Enrico Moretti and Chiang-Tai Hsieh, " Housing Constraints and Spatial Misallocation ," National Bureau of Economic Research Working Paper no. 21154, May 2017.

[19] See David Abouy and Mike Zabek, "Housing Inequality," National Bureau of Economic Research Working Paper no. 21916, January 2016.

[20] Matthew Rognlie, " Deciphering the Fall and Rise of the Net Capital Share ," Brookings Papers on Economic Activity, Spring 2015; Peter Ganong and Daniel Shoag, " Why Has Regional Income Covergence in the U.S. Declined? ," Journal of Urban Economics, Vol. 102, pp. 76-90, November 2017.

[21] See, e.g., Ross Levine, " Financial Development and Economic Growth: Views and Agenda ," Journal of Economic Literature, Vol. 35, pp. 688-726, June 1997.

[22] Cecchetti and Kharroubi, " Reassessing the Impact of Finance on Growth ."

[23] " Domestic credit to private sector (% of GDP) – United States ," The World Bank.

[24] Greenwood and Scharfstein, " The Growth of Finance ."

[25] Atif Mian et al., " Household Debt and Business Cycles Worldwide ," National Bureau of Economic Research Working Paper No. 21581, July 2016.

[26] " Home ownership is the West’s biggest economic-policy mistake ," The Economist, January 16, 2020.

[27] Lindsey and Teles, " The Regulatory Subsidy for Extreme Leverage ."; Anat Admati and Martin Hellweg, The Bankers’ New Clothes: What’s Wrong with Banking and What to Do about It , (Princeton, NJ: Princeton University Press, 2014).

[28] Admati and Hellweg, The Bankers’ New Clothes , pp. 176-191; " Federal Reserve announces plan to develop a new round-the-clock real-time payment and settlement service to support faster payments ," Board of Governors of the Federal Reserve System, August 5, 2019; John Cochrane, " Toward a run-free financial system ," SSRN, April 16, 2014.

[29] Morgan Ricks et al., " FedAccounts: Digital Dollars ," SSRN, July 16, 2020.

[30] " 2017 FDIC National Survey of Unbanked and Underbanked Households ," Federal Deposit Insurance Corporation.

[32] James Bessen and Michael Meurer, " The Direct Costs from NPE Disputes ," Cornell Law Review, Vol. 99, Issue 2, Article 3, January 2014.

[33] Rebecca Rosen, " The Missing 20 th Century: How Copyright Protection Makes Books Vanish ," The Atlantic, March 30, 2012.

[34] Jason Koebler, " Why American Farmers Are Hacking Their Tractors With Ukranian Firmware ," Vice, March 21, 2017; Elle Ekman, " Here’s One Reason the U.S. Military Can’t Fix Its Own Equipment ," New York Times, November 20, 2019.

[35] Miriam Laugesen and Sherry Glied, " Higher Fees Paid to US Physicians Drive Higher Spending For Physician Services Compared To Other Countries ," Health Affairs, Vol. 30, no. 9, September 2011.

[36] " Physicians (per 1,000 people) ," World Health Organization’s Global Health Workforce Statistics, The World Bank. It should be noted that Canada and the United Kingdom are comparable to the United States.

[37] Robert Orr, " The Planning of U.S. Physician Shortages ," Niskanen Center, September 8, 2020.

[38] Tim Dall et al., " The Complexities of Physician Supply and Demand: Projections from 2017 to 2032 ," Association of American Medical Colleges, April 2019.

[39] Joanne Finnegan, " More medical students than ever, but more residency slots needed to solve physician shortage, AAMC says ," Fierce Healthcare, July 26, 2019.

[40] Ruth Campbell-Page et al., " Foreign-trained medical professionals: Wanted or not? A case study of Canada ," Journal of Global Health, Vol. 3, no. 2, December 2013.

[41] Avik Roy, " Affordable Hospital Care Through Competition and Price Transparency ," FREOPP, January 31, 2020.

[42] Lusine Poghosyan, " Here’s an easy way to increase access to high-quality, affordable health care ," Washington Post, January 2, 2020; Morris Kleiner and Kyoung Park, " Battles Among Licensed Occupations: Analyzing Government Regulations on Labor Market Outcomes for Dentists and Hygienists ," National Bureau of Economic Research Working Paper No. 16560, November 2010; Bill Kekevian, " Expanding Scope of Practice: Lessons and Leverage ," Review of Optometry, October 15, 2018; Brittany Ranchoff and Eugene Declercq, " The Scope of Midwifery Practice Regulations and the Availability of the Certified Nurse-Midwifery and Certified Midwifery Workforce, 2012-2016 ," Journal of Midwifery & Women’s Health, Vol. 65, Issue 1, pp. 119-130, January 2020.

[43] " National Health Expenditures 2017 Highlights ," Centers for Medicare & Medicaid Services.

[44] Roy, " Affordable Hospital Care ."

[45] Ibid .

[46] Ibid .

[47] Avik Roy, " The Competition Prescription: A Market-Based Plan for Affordable Drugs ," FREOPP, May 16, 2017.

[48] Greg Ip, " A Cure for Swelling Drug Prices: Competition ," Wall Street Journal, August 31, 2016.

[49] Conor Dougherty, " California’s Housing Crisis: How a Bureaucrat Pushed to Build ," New York Times, February 13, 2020.

[50] " Locked Out? Are Rising Housing Costs Barring Young Adults from Buying their First Homes ?", Freddie Mac, June 28, 2018.

[51] " America’s Rental Housing 2020 ," Joint Center for Housing Studies of Harvard University, 2020.

[52] Hannah Knowles, " Homelessness in the U.S. rose for a third year, driven by a surge in California, HUD says ," Washington Post, December 21, 2019.

[53] See Glaeser and Gyourko, " Economic Implications of Housing Supply "; Herkenhoff et al., " Tarnishing the Golden and Empire States "; Hsieh and Moretti, " Housing Constraints and Spatial Misallocation ."

[54] Jessica Trounstine, " The Geography of Inequality: How Land Use Regulation Produces Segregation ," American Political Science Review, Vol. 114, Issue 2, pp. 443-455, May 2020; Michael Lens and Paavo Monkkonen, " Do Strict Land Use Regulations Make Metropolitan Areas More Segregated by Income ?" Journal of the American Planning Association, Volume 82, Issue 1, pp. 6-21, December 28, 2015.

[55] " Zoned Out: How School and Residential Zoning Limit Educational Opportunity ," United States Congress Joint Economic Committee, November 12, 2019.

[56] Patrick Sisson, " As cities confront climate change, is density the answer? ", Curbed, December 11, 2018.

[57] Richard Kahlenberg, " How Minneapolis Ended Single-Family Zoning ," The Century Foundation, October 24, 2019.

[58] Laura Bliss, " Oregon’s Single-Family Zoning Ban Was a ‘Long Time Coming’ ," Bloomberg CityLab, July 2, 2019.

[59] Kriston Capps, " With New Democratic Majority, Virginia Sees a Push for Denser Housing ," Bloomberg CityLab, December 20, 2019; Kriston Capps, " Denser Housing Is Gaining Traction on America’s East Coast ," Bloomberg CityLab, January 3, 2020.

[60] Elijah Chiland, " SB 50 didn’t pass. But California is still considering these housing bills .", Curbed Los Angeles, February 6, 2020.

[61] Patrick Sisson, " Will California’s new ADU laws create a backyard building boom ?", Curbed, October 11, 2019; Marisa Kendall, " Is California’s most controversial new housing production law working ?", Orange County Register, November 26, 2019.