In frequent posts on Universal Catastrophic Coverage [1] [2] [3], I have treated details regarding income thresholds, deductibles, and co-pays as open to negotiation. For simplicity, I often use a formula under which each person is automatically enrolled in a catastrophic plan that has a deductible equal to 10 percent of the amount by which their income exceeds the Medicaid threshold and pays 100 percent of expenses once the deductible is met, but those particular numbers are not sacred.

A helpful reader recently sent me a link to an alternative formula proposed by blogger Ben Paine. He modestly calls his plan “Ben’s Care,” as a placeholder for a better name to come. His specific formula for deductibles and co-pays differs from the simpler version I have used in two main ways.

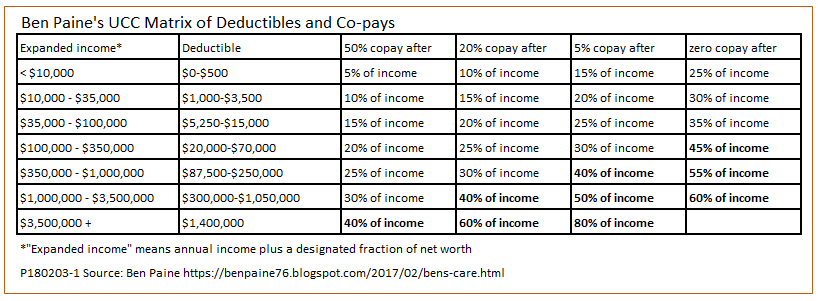

First, Paine uses an expanded concept of “income” that includes a component based on total wealth—say, 100 percent of this year’s total income plus 10 percent of net worth. It is not entirely clear what assets would be included or how they would be valued, but the idea is that a person with no savings and $50,000 in wage income should not be expected to contribute as much toward medical expenses as someone with $50,000 of interest income from several million dollars’ worth of government bonds.

Second, Ben’s UCC formula uses a sliding scale of co-pays. For example, a person with $50,000 of expanded income would pay 100 percent of medical expenses up to 15 percent of income, or $7,500. After that, UCC would kick in with a co-pay of 50 percent, falling to 20 percent, then 5 percent, and finally to zero as expenses rise. His entire suggested matrix of deductibles and co-pays looks like this:

Paine emphasizes, as I do, that the exact parameters of the formula would be subject to negotiation. To him, as to many market-oriented healthcare reformers, the important thing is to make sure that healthcare consumers have “skin in the game” for as much of their health care as possible, while still having a safety net against financial catastrophe.

{kind=link}