In December 2025, the U.S. government did two anomalous things in the span of a week: it launched a new citizenship by investment (CBI) program — the Trump Gold Card, Corporate Gold Card, and Platinum Card — selling U.S. residency or citizenship for between $1 million and $5 million dollars. Then, it banned the citizens of Antigua & Barbuda and Dominica from entering the country as immigrants, students, tourists, or on business, citing those nations’ CBI programs as a national security threat.

The administration’s objection to the Caribbean programs is based on the fact that the two countries issue passports with no residency requirement, meaning investors obtain citizenship without ever setting foot in the country. This, the White House argues, creates openings for financial crime, evasion of international sanctions, and terrorism financing. The concern is legitimate: the global anti-money laundering watchdog Financial Action Task Force (FATF) has documented exactly these risks in detail.

A close analysis of the Trump Card application materials reveals meaningful gaps against FATF’s anti-money laundering and counter-terrorism financing (AML/CFT) framework — gaps that mirror, in several respects, the very deficiencies used to justify banning Caribbean nationals. The U.S. has every right to pressure Antigua & Barbuda and Dominica to reform programs that pose genuine national security risks. However, it does not have the credibility to do so while launching a program that contains design-level gaps that, if left unaddressed, create conditions for similar misuse.

What citizenship by investment is, and why it matters

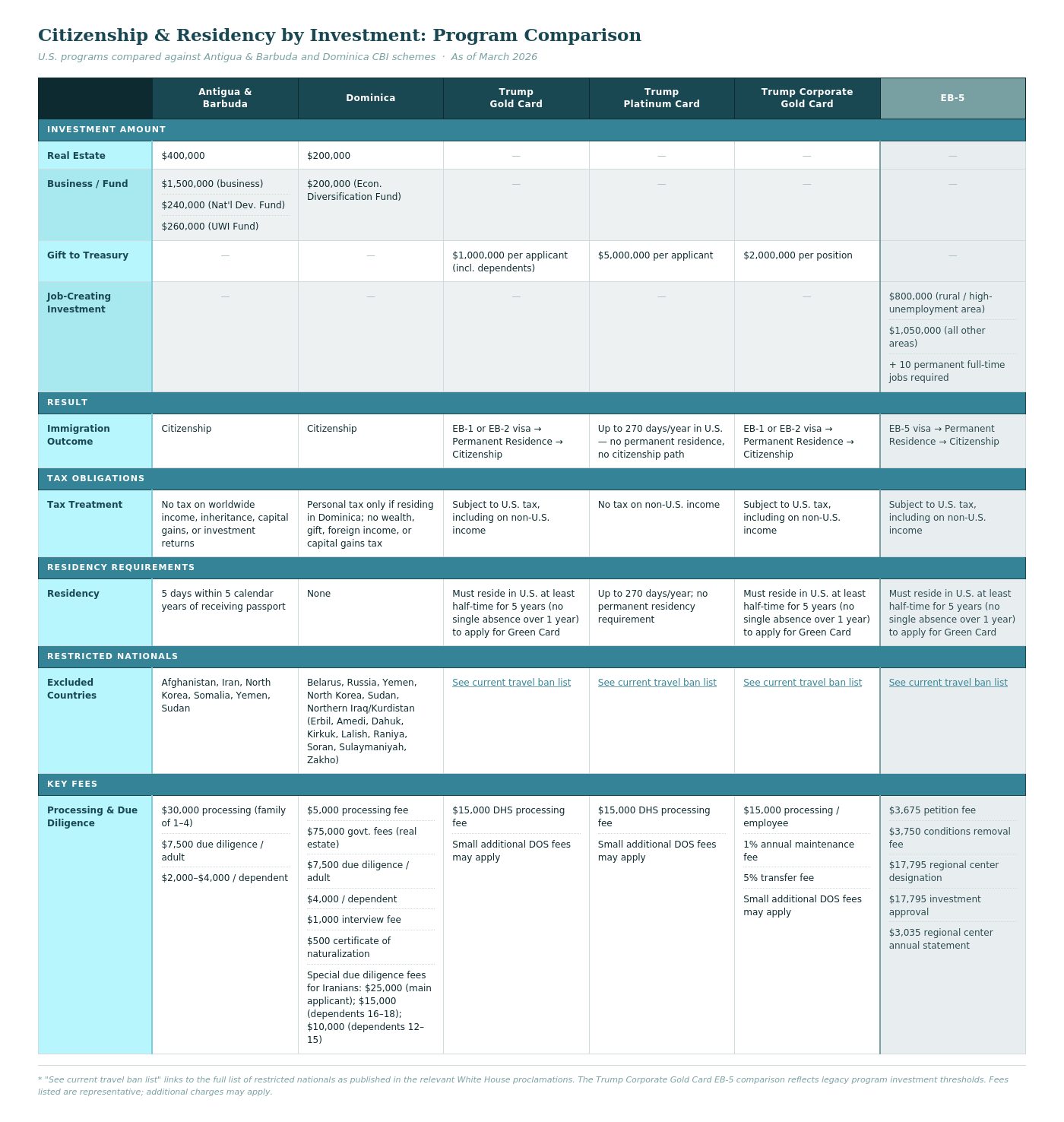

CBI — colloquially known as “golden passport” programs — refers to programs that sell citizenship or permanent residency to individuals in exchange for a qualifying investment in the country. The concept is neither new nor inherently illegitimate. The United States has offered its own investor visa, the EB-5, since 1990. Dozens of countries, including high-income nations such as Spain, Luxembourg, and the United Arab Emirates, operate similar programs. For small, low-income, developing economies, CBI can make a significant fiscal impact: In 2023, Antigua & Barbuda derived 60 percent of its nontax revenue from its program; in Dominica, CBI represented 37 percent of GDP.

But CBI programs have also been extensively documented as vectors for financial crime. FATF’s November 2023 report on the misuse of CBI around the world found that criminals have exploited program vulnerabilities to commit massive frauds and launder proceeds of crime and corruption reaching into the billions of dollars.

Programs without residency requirements are the most problematic. Because they allow applicants to obtain a passport without developing a financial footprint in the issuing country, they limit local authorities’ ability to monitor passport holders’ activities. Weak due diligence, political interference in vetting, and lack of transparency compound the risk. These are not theoretical concerns; they are the documented operational reality of programs such as those in Antigua & Barbuda and Dominica, and they are also the stated basis for the U.S. ban on travel from Antigua & Barbuda and Dominica. In several critical respects, they are characteristics of the Trump Card program.

Why Antigua & Barbuda and Dominica?

The White House proclamation imposing the travel restrictions states plainly that Antigua & Barbuda and Dominica were targeted specifically because their CBI programs have no residency requirements. While they are the only two countries whose citizens have been banned from entering the U.S. explicitly because of their CBI schemes, it’s worth noting another eight countries on the administration’s January 2026 immigrant visa pause list also have CBI programs: Grenada, Saint Kitts & Nevis, Saint Lucia, Saint Vincent & the Grenadines, Egypt, Jordan, North Macedonia, and Cambodia.

The programs in both countries are problematic. In Antigua & Barbuda, applicants can invest as little as $240,000 in real estate, a business, the National Development Fund, or the University of the West Indies Fund and receive a passport in return. The sole residency-adjacent requirement is a minimum five-day visit to the country at any point within the five years before passport renewal. CBI recipients owe no tax on worldwide income, inheritance, capital gains, or investment returns. In Dominica, $200,000 in real estate or the Economic Diversification Fund buys a passport with zero obligation to ever enter the country; recipients pay personal tax only if they reside there.

Both programs suffer from structural weaknesses that exacerbate these concerns. Their governance structures lack independence, making them vulnerable to corruption and political interference and the temptation to prioritize revenue over rigorous vetting. Due diligence for the programs is also inadequate. Dominica’s 2023 Mutual Evaluation — based on an on-site assessment conducted in 2022 — found the country falling short on several of FATF’s 40 Recommendations across several areas, with remaining deficiencies concentrated in targeted financial sanctions for terrorist financing, nonprofit organization oversight, and beneficial ownership transparency. Antigua and Barbuda’s most recent full evaluation, based on a 2017 on-site visit, found that targeted financial sanctions had not been addressed or implemented at all; as of the 2021 follow-up report, Antigua remained only partially compliant on this requirement. Both programs rely primarily on private due diligence firms for applicant vetting; while the multinational Joint Regional Communications Centre and its INTERPOL database access are available tools, their use has been inconsistent across programs and countries. Oversight of financial institutions and real estate developers is weak, public accountability through transparent reporting is absent, and investigative capacity is thin.

The consequences have been substantial. The widely publicized case of fugitive Indian billionaire Mehul Choksi, the main suspect in India’s largest bank fraud who obtained Antiguan citizenship and used it to resist extradition, illustrates the reputational and security risks in sharp relief. The European Union has treated the mere existence of CBI programs in the Eastern Caribbean as grounds to suspend Schengen visa-free access for the region. These are real costs, paid by the islands’ legitimate citizens.

The Trump Card programs

Since 1990, the U.S. has offered the EB-5 investor visa under the employment-based immigration umbrella. The program allows up to 9,940 investors annually to apply for lawful permanent residence if they invest a minimum of $800,000 in a business that creates 10 permanent full-time jobs for U.S. workers, or if they participate in the Regional Center Program, which pools investments to fund a qualified project. It is an investment program explicitly tied to economic output and job creation.

The Trump Card programs are a marked departure. Rather than requiring investment in a job-creating business, applicants make a “gift” to the U.S. Treasury: $1 million for the Gold Card, $2 million for the Corporate Gold Card, or $5 million for the Platinum Card. The administration has claimed the Trump Gold Card will replace the EB-5, but upon launch, it was announced that successful applicants would receive either an EB-1 or EB-2 visa. EB-1 and EB-2 visa categories are reserved, respectively, for workers with “extraordinary ability in the sciences, arts, education, business, or athletics” and for professionals with advanced degrees. Combined, EB-1 and EB-2 visas represent 57.2 percent of all employment-based green cards, roughly 80,080 visas annually. Routing wealthy donors through the EB-1 and EB-2 categories risks crowding out scientists, doctors, and business leaders selected on merit.

The Platinum Card warrants particular scrutiny. For $5 million, holders can spend up to 270 days per year in the U.S. without being subject to U.S. taxes on foreign income. Permanent U.S. residents are typically subject to worldwide income taxation; for a wealthy individual with significant foreign holdings, that exemption could amount to millions of dollars in foregone federal revenue annually. Research from the Yale Budget Lab suggests the Platinum Card will likely “pay for itself quickly” for individuals with high levels of foreign-source income, meaning the net fiscal contribution to the United States, after the $5 million gift, could be negative over the lifetime of the arrangement for some holders.

This is the feature that most directly mirrors the administration’s objection to the Eastern Caribbean programs. The White House cited the absence of residency requirements in Dominica and Antigua & Barbuda as a mechanism that insulates participants from financial oversight. The Platinum Card does something structurally similar: It allows high-net-worth individuals to maintain a substantial U.S. presence while keeping their foreign financial activity outside the reach of U.S. tax authorities. The security and oversight concern does not disappear because the price tag is higher.

Do the Trump cards meet the standard the U.S. demands of others?

A review of Form I-140G, the Trump Card application form, against FATF’s core AML/CFT framework reveals several meaningful gaps. While the form requires extensive upfront documentation including a 20-year employment history, source-of-funds verification, and sanctions screening, it appears to fall short of FATF best practices in ways that could matter.

FATF Recommendation 12 requires “appropriate risk management systems” and enhanced monitoring for Politically Exposed Persons (PEPs), foreign government officials and their associates who present elevated corruption risks. The form asks about government positions but does not indicate enhanced due diligence procedures for PEPs beyond that disclosure. FATF Recommendation 10 requires ongoing due diligence on the business relationship after approval; the form contains no provisions for postapproval monitoring. FATF Recommendation 24 requires that countries maintain adequate, accurate, and up-to-date information on the beneficial ownership of legal entities; the form does not require verification of beneficial ownership through independent registries.The program also contains no stated application cap (though EB-1 and EB-2 visa caps exist) and provides no public transparency regarding approved applications or revenues generated.

This last point is more than administrative. Transparency and public accountability are among the core safeguards that distinguish well-governed CBI programs from poorly governed ones. Their absence from the Trump Card framework is the same absence that has drawn sustained criticism of the Antiguan and Dominican programs.

None of this is to suggest that the Trump Card program poses the same level of risk as the Caribbean programs. The U.S. has substantially greater institutional capacity for financial oversight, law enforcement, and due diligence than Antigua & Barbuda or Dominica — which makes the design gaps in the Trump Card harder to explain, not easier. USCIS conducts the vetting of immigrants via the Immigration and Nationality Act (INA), and the Department of Treasury coordinates policy on AML/CFT as well as the country’s compliance with FATF’s international standards. Treasury does not influence the INA, and therefore USCIS uses its own standards built around national security, terrorism, and criminal admissibility. There is no statutory or regulatory requirement for USCIS to reference FATF standards when vetting immigrants — not because the U.S. lacks the ability to do so, but because it has not chosen to. FATF’s framework exists precisely because institutional capacity alone is not sufficient; program design matters. The gaps identified above are the same categories of gaps that FATF has documented as exploitable in other jurisdictions. A country with the resources and reach of the United States has less excuse for replicating them, not more.

Conclusion

The critical question is not whether the U.S. should offer residency or citizenship by investment — it has done so since 1990. It is whether the programs it administers will be held to the same standards it demands of others, and whether those standards will be enforced consistently or selectively.

The AML/CFT concerns about Antigua & Barbuda’s and Dominica’s CBI programs are real, documented, and consequential for those countries, their legitimate citizens, and the broader Caribbean region. The travel ban may prove to be an effective policy lever to compel rapid reform, or it may be collective punishment of ordinary citizens for structural deficiencies in programs they have no control over, deployed in service of unrelated immigration goals. That question deserves serious scrutiny.

But the near-simultaneous launch of the Trump Card programs with their own due diligence gaps, displacement of merit-based immigration, and the Platinum Card tax exemption that structurally mirrors the very feature used to justify the Caribbean bans raises a harder question. If the standard for a CBI program is FATF compliance, transparency, and genuine government oversight of participants’ finances, then shouldn’t the standard apply in Washington as readily as it does in Roseau or Saint John’s? The administration has not yet shown that it will.