With the introduction of the Supporting Newborn Parents Act, Reps. David Valadao (R-CA), Tom Suozzi (D-NY), Blake Moore (R-UT), and Debbie Dingell (D-MI) have put forward a powerful piece of pro-family legislation. The proposed newborn credit would give nearly all families celebrating the birth of a child another reason to celebrate: a refundable tax credit of $2,000 shortly after their baby is born. This timely payment would help parents navigate the financial shocks that tend to come in baby’s first year.

Working families in America rely on a series of overlapping family benefit programs:

- the Child Tax Credit (CTC) reduces a family’s tax burden while children grow to maturity

- the Child and Dependent Care Tax Credit (CDCTC) cushions the cost of child care

- the Earned Income Tax Credit (EITC) supplements wages for a family working toward stability

- the Trump accounts offer a tax-advantaged way for families to save for their children’s college tuition or retirement

However, these programs leave a gap in the period immediately after birth, when parents face rising expenses and, often, decreasing income. A newborn credit is a cost-effective, well-targeted program to help families during the transition.

The role of a newborn credit

A newborn credit would complement these existing family benefits, helping working parents immediately after the birth of a child. The family benefits noted above operate on a one-year lag. Parents qualify for these credits based on their earnings and/or their child care expenses in one year and then receive a corresponding tax credit the next year when they file their return. In the first year, parents face the increased costs of a new child but may have to wait for more than a year before their new dependent is reflected in their tax return.

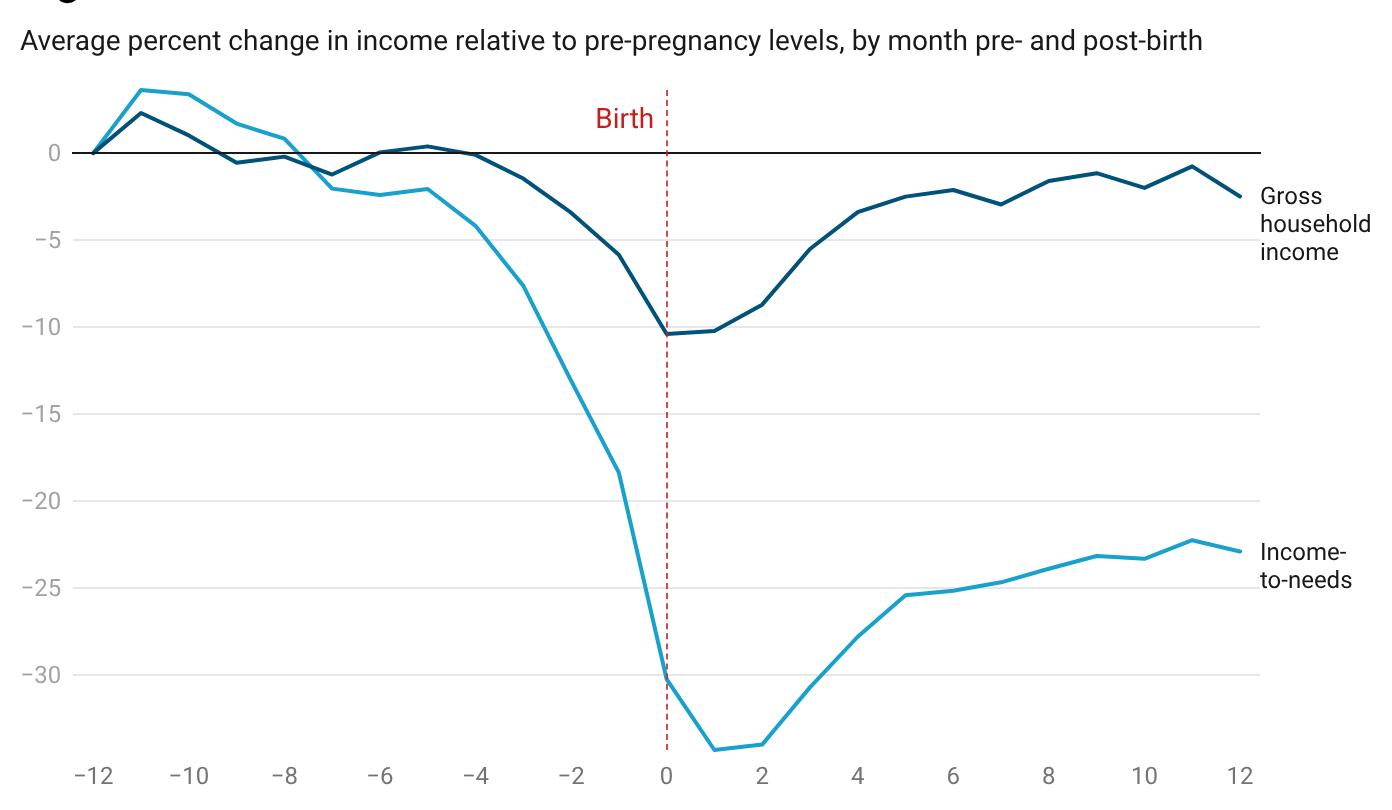

A newborn credit allows parents to receive a timely family benefit just as they hit the financial shock of a baby. In the months following the birth of a child, families see their household income drop by 10 percent on average. At the same time, their expenses surge. Parents need to make a range of expensive, one-time payments (hospital bill, car seat, crib) and budget for continuing costs (diapers, formula, baby clothes). Families’ falling income and rising expenses means that the ratio of their income to their needs drops. A newborn credit helps families weather this shock, just as unemployment insurance helps workers after a disruption to their employment.

Some parents will use the benefit to pay down the hospital bill (an average out of pocket payment of $2,743). For some parents, a newborn credit might let them stop trying to estimate how long they can leave their baby in a wet diaper without causing diaper rash. For other families, a newborn credit would provide the financial flexibility to take unpaid Family and Medical Leave Act (FMLA) time that they have earned but otherwise couldn’t afford to use. Seven percent of workers surveyed for a 2020 report by Abt Associates for the U.S. Department of Labor reported that they could not use FMLA for which they were entitled in a given year; of those, two-thirds said that the problem was that they could not afford unpaid leave.

In a national survey of likely midterm voters, American Policy Ventures, in partnership with the Niskanen Center, found that 65 percent of respondents supported or strongly supported a $2,000 newborn credit for parents. The policy was unpolarized: about equally popular with Republicans (69 percent) and Democrats (65 percent). Similarly, a newborn credit draws strong support from both women (65 percent) and men (64 percent) as well as married (66 percent) and single (63 percent) respondents. The results indicate that voters see a newborn credit as good public policy for the nation as a whole, not as a wedge setting some demographic groups against others.

Another national survey, by the Ethics & Public Policy Center, found that half (54 percent) of parents of children under 6 said that a newborn credit would make them more likely to think about having another baby. These are the parents for whom the financial turbulence that follows a new baby is the most relevant, and who may feel the most pressure to delay a hoped for little sibling.

The structure of the newborn credit

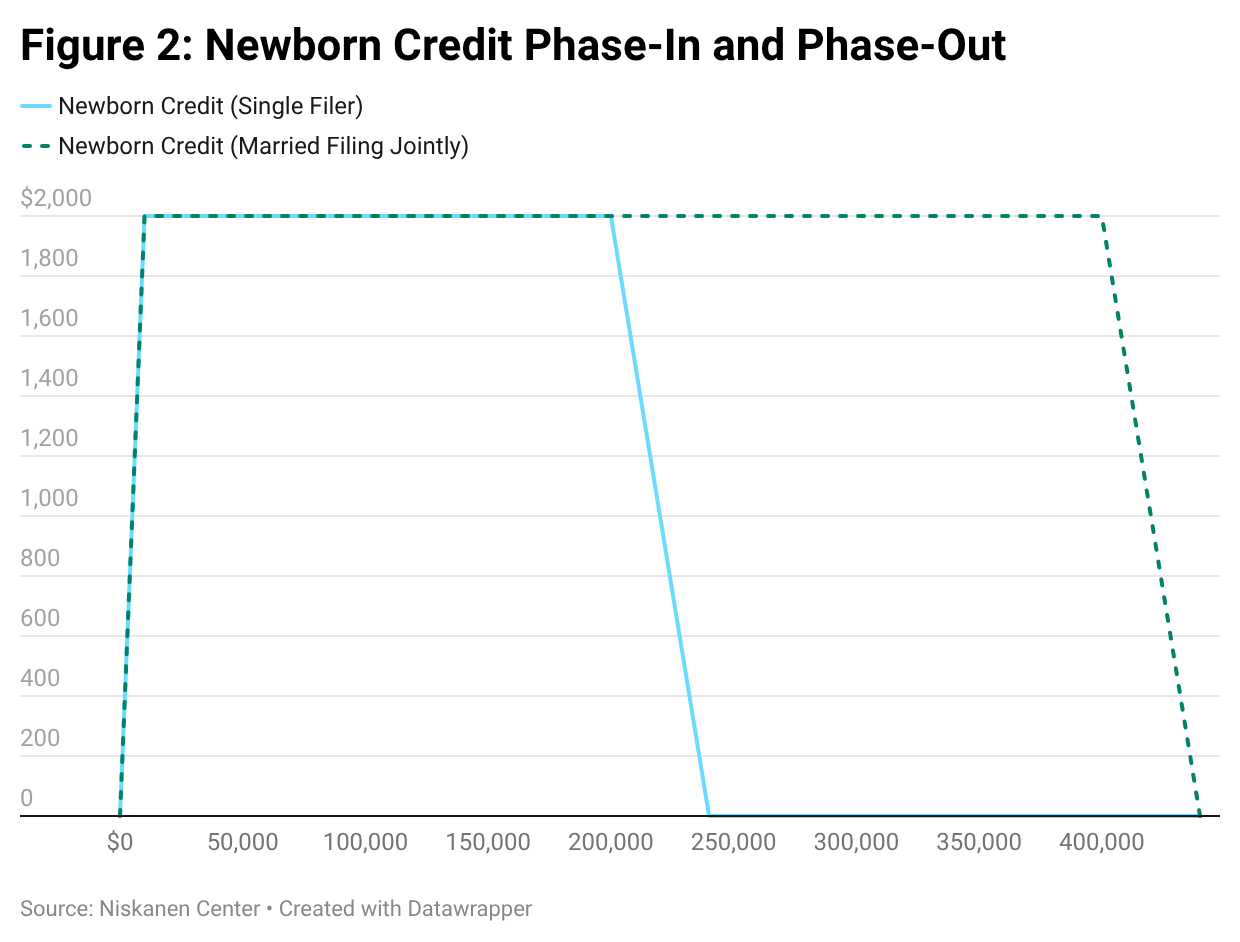

The proposed newborn credit would allow working families to claim a refundable tax credit immediately after the birth of a child rather than at tax time the year after the birth. The newborn credit would offer up to $2,000 per child (thus, $4,000 or more in the case of twins, etc.). The value of the credit would phase in with household earnings and phase out for high-earner households. Policy Engine estimates this proposed credit would cost $6.4 billion per year.

This newborn credit would phase in continuously at 20 percent from the first dollar earned (Figure 2). Families with household earnings of $10,000 or more would receive the full value of the credit. The credit would phase in for all children simultaneously — parents of twins would not need to earn twice as much to claim the credit for both children. The proposed credit phase-out mirrors that of the existing Child Tax Credit, phasing out at 5 percent, starting at a threshold of $200,000 for single parents and at $400,000 for married parents.

This credit mirrors the CTC in several other elements of its structure. The newborn credit would require that at least one parent have a Social Security number in order to claim the benefit. The newborn credit proposal also mirrors the CTC’s criteria for which a parent or guardian is eligible to claim a qualifying child if the parents do not comprise a single tax unit.

Because the newborn credit could be claimed shortly after birth rather than at tax-time the following year, it would incorporate a lookback provision that is not available in other family benefits. Families could qualify for the newborn credit by relying on their household earnings in either the year that their baby was born or their household earnings the prior year. This would allow families with children born early in the year to be certain they would qualify for the credit without worrying that a layoff could put them at risk of a clawback.

Any household that earned at least $10,000 in the year prior to their baby’s birth could confidently accept the full value of the newborn credit. Households not earning at least $10,000 in the year prior to the birth could receive the full value of the credit if they knew they had already passed the threshold, or were confident of being on track. For households not earning at least $10,000 in the prior year and not certain of clearing that threshold in the year of their baby’s birth, there would be two options: They could elect to defer the credit until tax time, when their annual earnings will have been known. Or, they could elect to receive a partial payment of the credit, based on their earnings to that point. In any case, all families receiving the credit would need to file a tax return, even if they otherwise would not owe taxes.

Under the proposal, parents would initiate their claim for the newborn credit as part of the same process allowing their child to be assigned a Social Security number. This bill adds a few additional questions to the paperwork that is already relayed to the Social Security Administration (SSA). In addition to the information that parents already provide, the new form would direct the SSA to relay the child and parent(s) name, SSN, preferred means of payment, and estimated earnings to the IRS in order to allow the IRS to initiate the payment.

Working through the SSA is intended to limit the credit’s susceptibility to fraud since the payment would be triggered by existing processes to generate a new SSN. This would limit the risk that several adults would attempt to claim the same child, a challenge for some other family benefits such as the CTC and EITC. It also would avoid burdening parents with extra administrative processes or asking the IRS or SSA to take on work outside their core functions. The legislation would also direct the IRS to create a registry portal so that expecting parents could submit all relevant information ahead of time and the IRS could quickly process a payment upon receipt of a new, valid SSN.

Conclusion

The proposed newborn credit is good public policy in support of working families and is sufficiently flexible to allow each household celebrating a new birth to make one more good choice for their family.