- New York State’s newly enacted FY 2027 budget includes major new mass transit projects for New York City, among them the Interborough Express (IBX), which would be the city’s first new end-to-end rapid transit line in almost a century.

- The near-term federal transit funding outlook is rocky, but the budget includes a powerful funding and financing tool that will allow the state transit authority to “capture” the added value that the IBX and future projects will create.

- The project will need a market-grade underwriting, but we find that the lower-bound estimate of funding available for the IBX through this state tool is in the billions of dollars.

In her 2026 State of the State address in January, New York Gov. Kathy Hochul outlined an ambitious transit infrastructure agenda. Not only would the Metropolitan Transportation Authority (MTA) move ahead with the Interborough Express (IBX), the city’s first new end-to-end rapid transit line since 1937, but, Hochul said, it would also extend the Second Avenue Subway to 125th Street in Upper Manhattan as long envisioned.

But big ambitions come with big price tags. The next phase of the Second Avenue Subway extension is projected to cost over $7 billion; the IBX is projected to cost $5.5 billion. While the MTA is looking into potential cost savings, the question of how New York will foot the bill remains. Federal transit funding is uncertain given the Trump administration’s hostility to transit investments, and even in less politically volatile times, the procedural requirements for federal grants can delay projects and inflate costs.

New York State’s long-overdue FY 2027 state budget, adopted late Tuesday, includes a powerful alternative to fund those projects: land value capture. Widely used in Japan, Hong Kong, and elsewhere and known as the “Rail plus Property model,” land value capture encompasses policy tools that connect the private real estate value created by local public investments with the funding needed for those investments to trigger a virtuous cycle of cost-effective growth.

When the MTA expands the transit network, residents near new stations can access more jobs and services in a fixed amount of time, and businesses can access a larger labor pool and customer base. These benefits substantially increase the value of nearby properties. Land value capture allows the public to recoup a share of that windfall — on the principle that public investments shouldn’t exclusively enrich private landowners — and reinvest it for public benefit.

New York City and the MTA should recognize this principle and use land value capture to fund the IBX, finally resuming the continuous expansion of the subway system that stalled before World War II.

Value capture under Section 119-R

New York City’s ability to recapture the value of its transit investments is embedded in Section 119-R of the New York General Municipal Laws, enacted in 2016 and recently extended to April t, 2027.

The provision enables value capture for transit investments, both directly and indirectly, through three mechanisms. The first two are new taxes that a city can impose on property owners in conjunction with transit projects: special transit assessments and land value taxes. A special assessment is a tax on nearby properties, both the parcels of land and their improvements. A land value tax is a more targeted levy on land alone, rather than on the property as a whole.

The third mechanism is known as tax increment financing (TIF), in which public agencies such as the MTA can borrow against the property taxes that their projects will generate. Unlike the other two provisions, TIFs are financing mechanisms and do not entail additional value capture.

The land value taxes that this provision enables may be the most important. The value of underlying land, not physical structures, increases in response to nearby improvements, so this tax would fall more directly on the value generated by the state’s investments — without penalizing construction.

This matters because it’s been more than a decade since New York last used any kind of value capture to fund a subway extension. That project entailed the sale, in 2015, of air rights and a TIF-like redirection of payments in lieu of property taxes to help fund the extension of the MTA’s No. 7 train from Times Square to the redeveloped Hudson Yards on Manhattan’s West Side waterfront. In that alternative model of value capture, a fee is collected if a developer builds, but not if they leave the land undeveloped. In effect, it taxes the decision to build.

But the Hudson Yards approach is no longer viable for the IBX: New York has since layered on new programs that already capture much of the value from upzoning. Between inclusionary zoning, prevailing wage rules under Section 485-x of New York State Real Property Tax Law, and other exactions, there is little left for the city’s Planning Department to claim through District Improvement Bonuses (the fees developers pay for additional floor area) near proposed IBX stations. Besides, the incremental property taxes from upzoning are already exempted to offset the costs of inclusionary zoning and prevailing wage mandates: property taxes that have already been forgiven can’t fund transit.

A land value tax avoids this problem by capturing the added value — the value uplift — in both the build and no-build scenarios. It will capture the land value created by transit access without relying on the meager leftover value unlocked by residential upzoning alone.

The Second Avenue Subway precedent

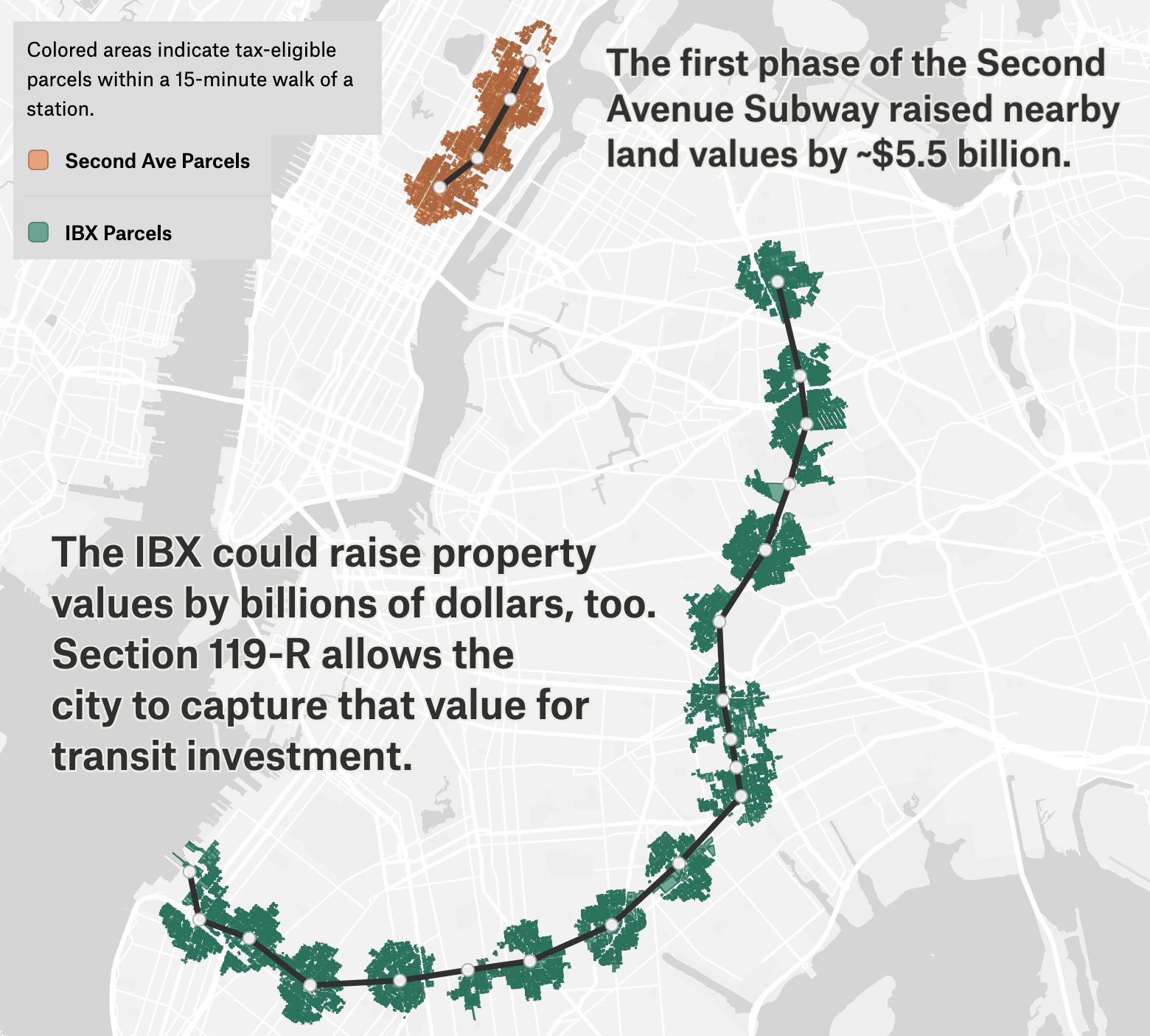

At a cost of $4.5 billion, the 2017 Second Avenue Subway extension was the most expensive two miles of transit ever built. The project involved an extraordinary amount of waste and delay that must be shaved off future projects. Yet even with its bloat, it was well worth the cost. In their 2022 paper “Take the Q Train,” economists Arpit Gupta, Stijn Van Nieuwerburgh, and Constantine Kontokosta found that the extension boosted property values in the Second Avenue corridor by 8 percent, generating $5.5 billion in uplift — enough to pay for the entire line with over $1 billion left over. Despite the excess expense, a centrally located subway line in the densest neighborhood in North America still generated enough social value to pay for itself.

But existing property taxes only capture some of that windfall — the authors estimate that only ~30 percent of the private uplift value will ultimately flow back to the city’s general fund. The remaining uplift generated by public investment will stay in private hands. The more substantial levy that Section 119-R authorizes would ensure that the landowners who stand to benefit the most from public investments pay a commensurate share.

Value capture along the IBX

The value generated by the first phase of the Second Avenue Subway is not obviously replicable with other projects, given the exceptional land values of Manhattan’s Upper East Side. But if the IBX extension generates even a fraction of the $5.5 billion value that the Second Avenue Subway created, the case for value capture is strong.

To estimate the IBX’s potential, we took the value uplift percentages that Gupta, Nieuwerburgh, and Kontokosta found, and then applied them to notably undervalued city property assessments near the planned IBX route. Using a 0.3-mile (as the crow flies) buffer around proposed stations and the 5.6 percent uplift rate Gupta et al. found for properties nearest the new Second Avenue Subway stations yields approximately $1.5 billion in added value. Expanding to the properties accessible on a .5-mile (approximately 15-minute) walk raises that to $2.1 billion. At the higher 8 percent rate that the authors found along the Second Avenue corridor itself, these projections rise to $2.3 billion and $3.3 billion, respectively.

And there are sound reasons to believe that, on a percentage basis, IBX could exceed the returns to the Second Avenue project. This potential depends on two competing considerations.

On one hand, the Second Avenue Subway serves some of the densest, most valuable real estate on the planet. Paring even small amounts of time off commutes in the area could create outsized gains for the millions of residents who live in and commute to the area. On the other hand, the Upper East Side was generally well served before the expansion; though the expansion was highly productive, it was a marginal improvement for an area that already had high transit access. In contrast, many of the IBX stations are sited in transit deserts. Providing residents of the outer reaches of Brooklyn and Queens with access to jobs in Manhattan could be even more transformative, even if the expansion is located on the periphery rather than in the city’s center.

In addition, zoning restrictions constrain land values in Brooklyn and Queens. If the IBX expansion is paired with transit-oriented upzoning to lift those constraints, new transit access would unlock more housing capacity, higher land values, and greater fiscal returns. Even though the maximum allowed density in the IBX corridor is far below that on the Upper East Side of Manhattan, the corridor still has more unused existing “zoned capacity” than the Manhattan areas that the Second Avenue Subway extension served at the time it was completed. Even if much of the incremental upzoning value is captured by inclusionary zoning and 485-x wage rules, the IBX’s potential to catalyze development could result in both short-term value uplift and long-term revenue expansion.

As calculated, the IBX’s uplift may not offset its full $5.5 billion price tag. But it could substantially offset capital costs and, if paired with upzoning, generate a steady, growing return on public investment, funding further infrastructure expansion at a pace New York hasn’t seen in decades.

Putting transit funding on solid ground

Beyond the IBX and Second Avenue extensions, establishing value capture as a permanent funding feature would significantly improve current mechanisms for transit planning and development.

First, the MTA’s use of broader-based taxes does not distinguish between those who benefit most from capital improvements and those who do not; value capture would allocate the funding burden directly onto the greatest beneficiaries.

Second, it enables local autonomy over capital decisions. The total federal funding pool for transit is limited; even when New York wins grants, the delays caused by application and compliance work can add years (and huge costs) to projects. Even in more stable environments, autonomy for local decision-makers is extremely valuable. In a previous value capture success, the Hudson Yards tax increment financing enabled then-Mayor Michael Bloomberg to extend the No. 7 train without federal help.

Third, using 119-R value capture to support new projects would create a virtuous cycle of investment and recaptured returns. By building institutional knowledge in the relevant agencies, a development pipeline supported by value capture might even mitigate many of the cost issues that plagued inexperienced planners during the Second Avenue Subway extension.

Conclusion

By enacting the 119-R extension, the governor and the legislature have equipped New York City with the ability to capture the value that investment in public transportation creates. As a project both sufficiently transformative to deliver the required value and large enough to demonstrate how value capture can work at scale, the IBX is the right place to start.