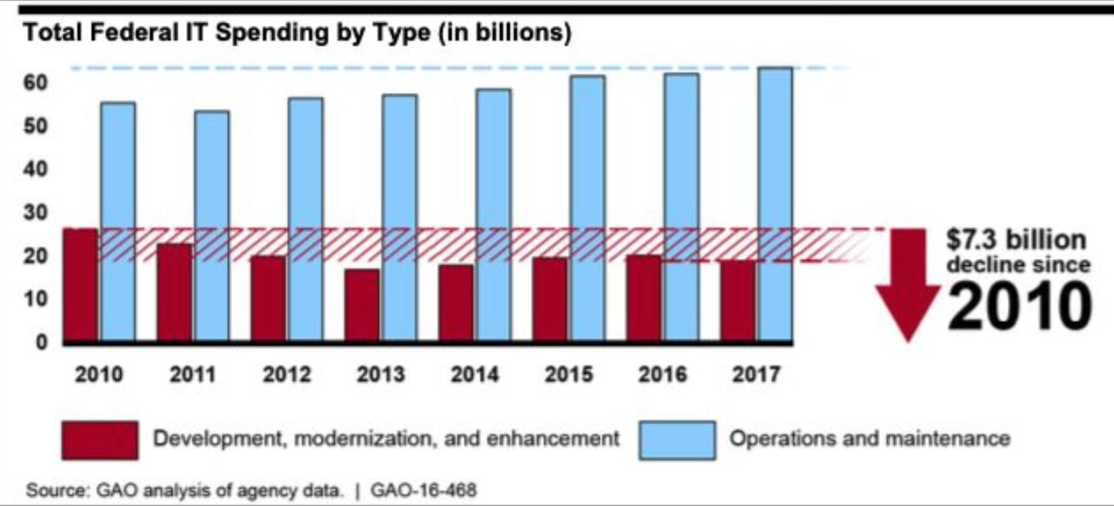

The United States government spends more than $100 billion on technology every year and nearly 80 percent of it goes to sustaining aging systems rather than modernizing them. To be sure, not all older systems are a problem, and some legacy technology, including mainframes, continues to perform important functions well. The concern is technology that has become too brittle, costly, or insecure to keep pace with agencies’ needs. These programs often keep these platforms running because they support essential missions and are difficult to replace. But over time, the “technical debt” from not keeping pace grows, institutional knowledge erodes, and rising maintenance costs crowd out capacity for improvement.

This is the legacy IT trap: a self-reinforcing cycle in which deferred investment makes systems harder to modernize, while making the kind of costly and politically fraught overhaul nobody wants all but inevitable.

As operations and maintenance consume more of the budget, agencies lose the room to modernize systems incrementally and are pushed toward larger, riskier replacements.

The root cause of this cycle is structural: The federal government budgets for technology the way it budgets for bridges and roads, as discrete projects that receive large up-front investment and are expected to operate for years with minimal reinvestment. That approach is a poor fit for software. As Anne Lewis and Jennifer Pahlka argue in “The Product Operating Model: How Government Should Deliver Digital Services,” digital systems are not one-time assets. They require sustained investment, iteration, and dedicated teams to keep pace with changing needs, threats, and emerging technology. Yet, the annual appropriations cycle is a poor fit for this reality. Agencies are often forced to plan long-horizon work inside short-term funding structures. The result is a budgeting system well adapted to annual political cycles, but poorly adapted to the work it is actually funding.

The Technology Modernization Fund is the federal government’s attempt to escape that pattern. Congress created the TMF in 2017 with an initial $175 million to supplement the appropriations process with flexible, multiyear capital for modernization work that does not fit neatly within a single budget cycle. In exchange for this flexibility, Congress imposed transparency, governance, and reporting requirements that most IT spending never receives. I served as TMF’s executive director from 2024 to 2025, and in my view the fund, and programs like it, are necessary for agencies to break the legacy IT trap. But TMF matters for more than what it finances. Its design, and the tensions that have built up around it, reveal the limits of treating modernization as a one-time capital investment rather than a continual process of adapting systems to meet changing needs.

Why TMF is important: Moving at the ‘speed of need’

For some agencies, TMF is the only plausible path forward, especially when modernization must unfold over several years or falls below the threshold for direct appropriations. Larger agencies may have budget flexibility or political weight to pursue modernization in other ways. Smaller agencies often do not. They may be running brittle systems that support critical functions, fully aware of the risk but with no realistic way to address it before something fails. TMF has at times provided one of the few government-wide mechanisms capable of moving flexible, multiyear funding quickly at the speed of need, including supporting the federal government’s response to the SolarWinds breach, one of the most significant cyber breaches in recent years, exactly the kind of urgent, cross-agency need that the standard appropriations process moves too slowly to address.

The fund also improves governance of IT spending. It is led by a multidisciplinary board of senior leaders from across the federal government, chaired by the federal CIO, and supported by a program management office at the General Services Administration that reviews proposals, recommends investments, and tracks performance. That structure brings cross-government judgment to bear on modernization decisions that would otherwise be made in agency silos.

The application process reinforces this discipline. Agencies compete for funding, which forces a sharper articulation of the problem, the approach, and the expected value than standard IT budget requests require. Funding is released in stages against milestones, giving the fund leverage to ask whether a project is progressing and whether course correction is needed. The program is also required to notify Congress of each proposed investment before any award, giving legislators the opportunity to object. That safeguard is often missed in debates about whether TMF operates outside the appropriations process; in practice, Congress has a clear line of sight into every investment and can push back on any of them.

Most importantly, TMF funding is available until expended and can span multiple years. For a CIO, that matters: It creates room to plan modernization as a sequence of deliberate moves rather than a one-year scramble, to stage work, manage dependencies, and reduce transition risk. That is much closer to how successful modernization actually happens.

Where TMF’s mandate and model collide: The repayment requirement

Congress gave TMF a broad mission under the Modernizing Government Technology Act: help government modernize technology, improve cybersecurity, and reduce the risks created by aging systems. The law says the fund exists to “improve information technology” and “enhance cybersecurity across the Federal Government,” and it authorizes investments to “improve, retire, or replace existing Federal information technology systems.” At the same time, it structured TMF as a revolving fund, with agencies required to repay awards over time. The statute says agencies “shall reimburse the Fund,” and those repayments are credited back to it. Those two design choices pull against each other.

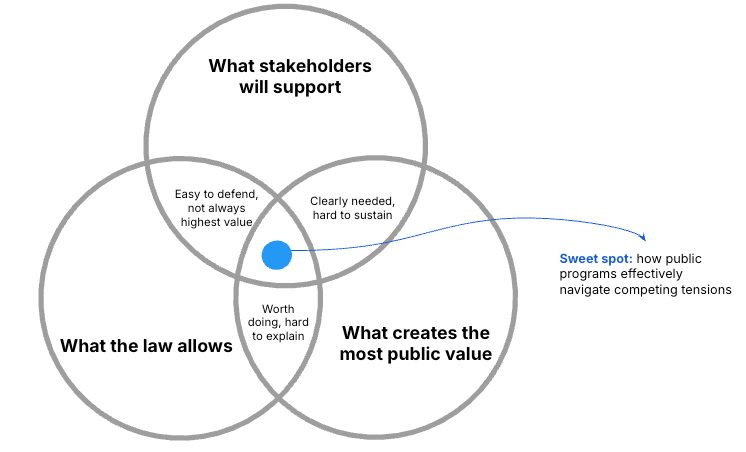

Many public programs optimize for only one or two of these dimensions. The most durable ones are clear about the outcomes they are pursuing, the tradeoffs they are making, and how they will manage all three.

In practice, TMF gets evaluated through three lenses at once:

- what the law authorizes

- what stakeholders including Congress expect

- what is actually highest-value to do

Those lenses can overlap, but they often don’t. The law leaves room for a wide range of important modernization work. Stakeholders often want faster, more visible proof that money is being well spent, or they hold widely different views of “value” depending on their perspective. Some of the highest-value investments also take longer to pay off or generate returns that are more qualitative and harder to express in budget terms.

Beneath these pressures is a more fundamental problem: TMF has never had a fully settled investment thesis. It’s not just that stakeholders disagree about what the fund is for. They also disagree about what kinds of investments belong in its portfolio, what repayment is meant to prove, and what return on investment should mean in a program in which some of the highest-value work may not generate clear financial savings at all. Some see TMF as a mechanism for converting single-year appropriations into stage-gated, no-year capital, with strict repayment as the discipline that keeps the model credible. Others see it as a way to fund important modernization work that agencies cannot move through ordinary appropriations quickly enough. Still others argue that it has drifted toward something closer to delegated spending authority, supporting work that might not otherwise be funded at all.

My own view, based on time inside the program, is that the statute is broad enough to accommodate more than one of these interpretations, and that TMF has in practice served several at once. That’s not necessarily a flaw in the program design. It reflects the fact that the fund is at the intersection of several real needs. But it does mean the program operates without a settled theory of change, and that ambiguity is one reason it remains so vulnerable to criticism.

This tension shows up most clearly in the repayment model. The premise is straightforward: agencies modernize, realize savings, repay the fund, and free up capital for future investments. In practice, that fits a relatively narrow class of projects. Many of the most important modernization decisions don’t produce discrete, near-term savings, even when they’re clearly the right investments to make. Even investments that look like they should generate savings, such as cloud migration, often just shift costs around rather than reduce them, but they’re still important investments to make given the need for modern infrastructure across government.

Why repayment and public value are not always the same thing

When no one agrees on what return on investment means, or over what timeframe, portfolio design gets murky, evaluation becomes inconsistent, and political support weakens. Genuinely important projects can then end up looking misaligned with the program’s stated purpose.

Where reforms could be made

TMF plays an important role, but the model could be stronger on three fronts: a clearer articulation of the types of investments it’s meant to support; an explicit connection to an enduring, government-wide IT modernization strategy; and more regular engagement with Congress on how the fund’s revolving structure is meant to support more sustainable agency modernization practices over time.

The most important step is making the portfolio framework explicit. Flexible funding models such as TMF should be able to support two distinct types of investments: those that generate direct savings and can credibly support repayment; and those justified mainly by risk reduction, service improvement, or mission outcomes that don’t yield a clean financial return. Both belong, and we need to say so plainly. Without that clarity, TMF will keep getting judged as if cost savings and repayment were the default standard even when the highest-value investments don’t meet that test.

A well-defined portfolio also demands evidence and delivery discipline to hold together, and TMF should use funding itself as both carrot and stick to get there. The program’s core design features are built for exactly this kind of work: incremental funding tied to milestones, board oversight, and rigorous PMO review. Used deliberately, they can reinforce practices that are working, prompt course correction when assumptions no longer hold, and end underperforming efforts before they consume further resources. Each investment then becomes a source of learning that the program can carry into the next, so that over time the portfolio teaches agencies, and TMF itself, what effective modernization actually requires. The goal isn’t just to fund good projects. It’s to use the investment process to improve how agencies build and buy technology, and to make better operating models a condition of continued funding rather than a nice thing to have.

TMF should also be used more strategically across government. Since its inception, it has received over $4 billion in funding requests while managing just over $1 billion in active investments, and that gap is one of its most underused assets. The proposal pipeline offers a valuable view into the state of federal IT: which systems are under strain, which needs recur across agencies, what modernization actually costs, and where demand points to shared problems more efficiently solved once than replicated many times over.

In practice, though, that information has been hard to use this way. After TMF received a major infusion of funding through the American Rescue Plan Act, much of the program’s capacity had to go toward scaling quickly and building the core processes needed to handle intake, proposal review, investment management, and oversight at a very different level. That left less room to treat the pipeline and broader portfolio as a strategic, cross-government source of insight. But this data should be used to shape more than individual awards. GSA could use it to identify opportunities for shared services or government-wide products that are more economical at scale. OMB could use it to sharpen budget guidance and prioritize the highest-value interventions. Congress could use it to ground oversight and appropriations discussions in a clearer picture of where federal technology needs are concentrated and what types of interventions are actually working and at what price points.

Used in these ways, TMF, and flexible funding models like it can be more than a source of capital; they can also be a source of business intelligence that few other programs can provide.

The larger lesson

TMF is worth supporting. It gives agencies access to multiyear capital, active governance, and milestone-based accountability. For smaller agencies with brittle systems and no realistic path through regular appropriations, it’s often the only viable option. But it should continue on clearer terms.

The deeper value of TMF isn’t just what it funds. It’s also what it exposes: that government doesn’t merely underinvest in modernization, it approaches software with the wrong assumptions entirely. One-time capital projects have a beginning, a delivery date, and an end. Modern digital services don’t. They have to evolve as policy changes, threats emerge, and user needs shift, and they need new funding and delivery models to match.

The fact that TMF has to exist, and that demand for it has routinely outstripped its capacity by a factor of four, is itself diagnostic. It tells us the broader system isn’t keeping up with what government needs its technology to do, and that TMF is, in important respects, a workaround for a problem the appropriations process has yet to solve.

TMF’s long-term future is still uncertain, but recent congressional action suggests that lawmakers still see value in the underlying model and premise. Congress provided the fund with $5 million in FY2026 appropriations after reauthorizing it through September 30, 2026, and the House has since advanced an FY2027 bill that would provide another $5 million. The more important task now is to be clearer about what TMF is for: not just a financing mechanism, but a tool for helping government change how it builds, buys, and sustains technology over time. Even a well-run TMF is still compensating for a deeper structural problem. The larger challenge is to build a budgeting and delivery system that no longer depends on a workaround like this in the first place. Until that broader system emerges, TMF, clarified and strengthened, remains one of the most direct tools available for making that shift possible, and for making government systems work better for the American people.