Tax season is a useful reminder that how we organize financial information matters just as much as the numbers themselves. Taxpayers file returns, but the underlying numbers come from employers, who report wages directly to the government. Without that upstream reporting, the total simply would be error-prone.

That’s true, too, of carbon accounting: There are several ways to measure emissions, each targeting a different node in the supply chain. You can calculate emissions upstream, measuring the carbon content stored in raw fuels, or downstream, monitoring the gases as they exit a smokestack. Ideally, they should provide the same information, much like estimating the weight of an ice cube by either weighing the tray or measuring the water poured into it.

The real questions are these: Which approach provides the most useful information for curbing the pollution without imposing unnecessary burdens? Is there a situation in which we would insist on collecting every possible data point, regardless of the cost of doing so? The answers shape what we consider ideal carbon management policy and determine which policies complement one another.

Compliance carbon policy — mandatory regulatory systems that aim to cap greenhouse gas emissions — frame the decision-making by offering a variety of approaches for the government to choose from. There are three primary compliance carbon policy frameworks, each applying carbon accounting at a different stage of production:

- carbon taxes

- cap-and-invest

- border carbon adjustments (BCA)

While these approaches can overlap in practice, the differences in how they are implemented, such as the point of regulation and the number of entities covered, have important implications for both their implementation complexity and their real-world outcomes. More importantly, they are not all mutually exclusive, but in fact can complement and reinforce one another.

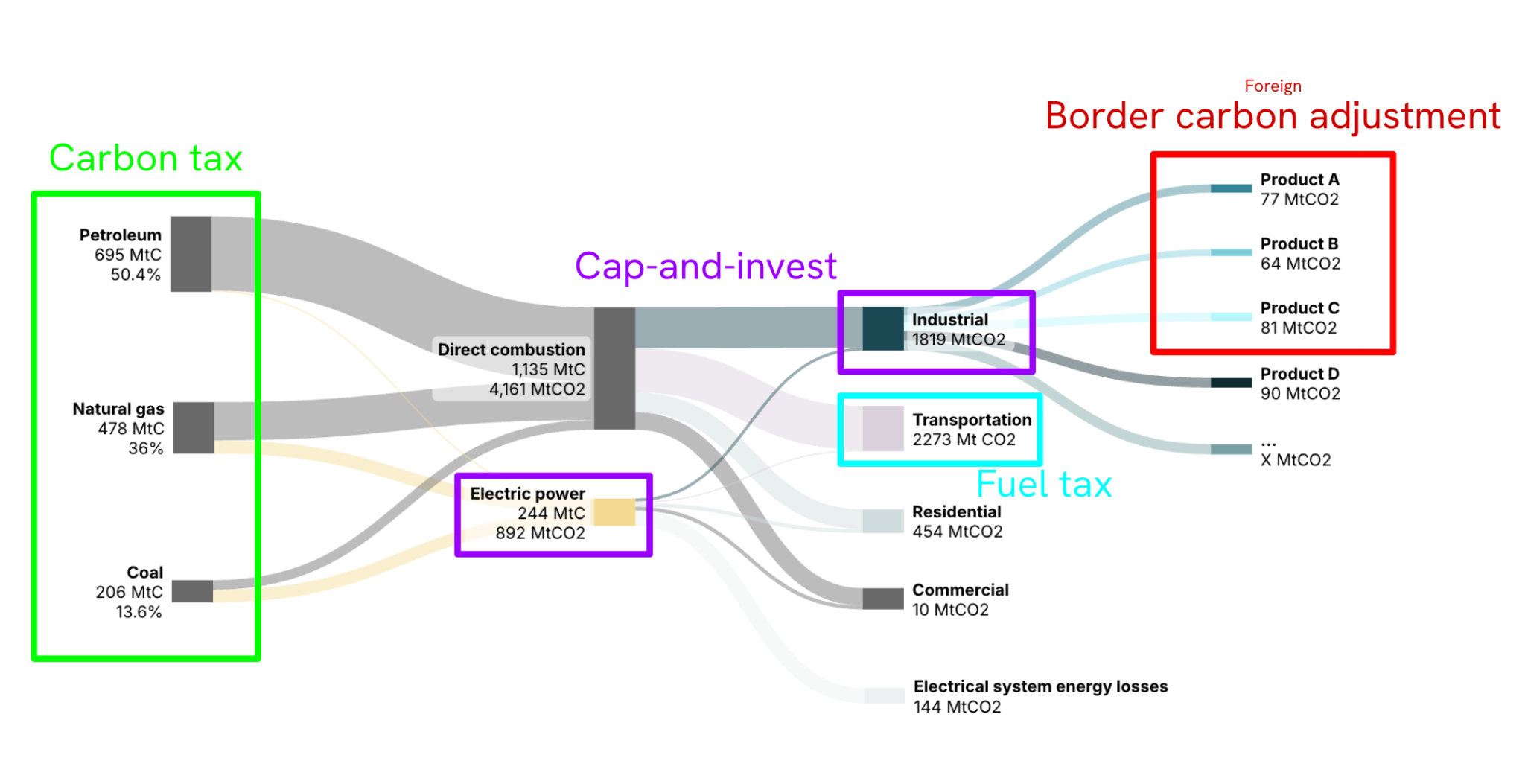

Figure 1. Carbon flow in the value chain and the regulation point for carbon pricing

Different carbon pricing instruments regulate at different points in the value chain, but all rely on the same underlying fuel-based carbon flows.

Source: Data are derived primarily from the U.S. Greenhouse Gas Inventory (EPA 2023) and U.S. energy facts explained (EIA 2024) and have been simplified for illustrative purposes. Created with Sankeyart.com.

Point of regulation in the carbon flow and efficiency implications

Carbon tax (Upstream, green box in Figure 1)

Over 3,600 economists have endorsed a carbon tax as the most efficient tool for emissions management. By pricing carbon at the refinery gate or mine entrance, the U.S. government can tax the vast majority of carbon entering the economy by monitoring roughly 1,200 upstream sites, including 132 oil refineries, 524 coal mines, and approximately 510 natural gas processing plants. Downstream actors such as farmers, factory owners, and restaurant owners, do not need to know how much carbon they buy with the fertilizers, materials, and gas. Nor do they need to track the carbon content of their purchases since the price is already reflected in the cost of the energy and materials they use

Cap-and-invest (Midstream, purple boxes in Figure 1)

Under cap-and-invest, which is the only existing carbon pricing policy in the U.S., firms report emissions at the facility level, where combustion occurs: at the power plant or factory floor, for instance. Regulators set caps on the maximum level of emissions that a company is allowed to pump into the atmosphere and establish markets that allow companies exceeding their abatement expectation to sell excess capacity to those who do not. Unlike sulfur dioxide, or SO₂, which is typically monitored continuously at the smokestack, carbon emissions are generally estimated based on fuel consumption for simplicity.

Estimating emissions from fuel, a proxy calculation, has the added benefit of capturing emissions that might otherwise go undetected through leakage. However, because cap-and-invest programs regulate emissions at the facility level, they typically involve a much larger number (on the order of at least 8,000 in the U.S.) of regulated entities than upstream approaches simply because there are far more energy users than energy producers, and require additional administrative infrastructure to operate the allowance trading markets.

Border Carbon Adjustment (BCA) (Downstream, red box in figure 1)

BCA functions essentially as a tariff on the carbon contained in imported goods, with the importing company charged for embedded emissions above a set level. The BCA has become one of the most discussed topics in compliance carbon markets since the European Union began the operational phase of its carbon border adjustment mechanism (CBAM) in January 2026.

The administrative infrastructure becomes evident in the BCA approach. That’s because companies exporting to a BCA jurisdiction must take facility-level emissions data, allocate those emissions across their products, and report those product-level values to the importing country. This creates additional burdens not only for firms, but also for governments, which must ensure the accuracy of data generated outside their own borders. As a result, the system relies heavily on third-party verification, which may include on-site facility visits to confirm the credibility of reported emissions.

Emissions coverage

Fig. 1 can be read as a series of stages in the energy and production system, each representing total emissions at that point. Viewed this way, the differences in policy coverage become clear. Using the United States as an example, taxing carbon dioxide by fuel usage at the exit of fuel production sites, would cover roughly 76 percent of total greenhouse gas emissions (See Fig. 2). A federal cap-and-invest program with a facility threshold of 25,000 tons of greenhouse gases — if we use GHG Reporting Program as the reference — would cover about 75 percent of industrial emissions and nearly all emissions from the electricity sector, which together account for roughly 41 percent of total national emissions. By contrast, even if every other country implemented BCA while the United States lacked a federal carbon price, the share of U.S. emission covered would be comparatively modest because exports account for only about 11 percent of U.S. GDP.

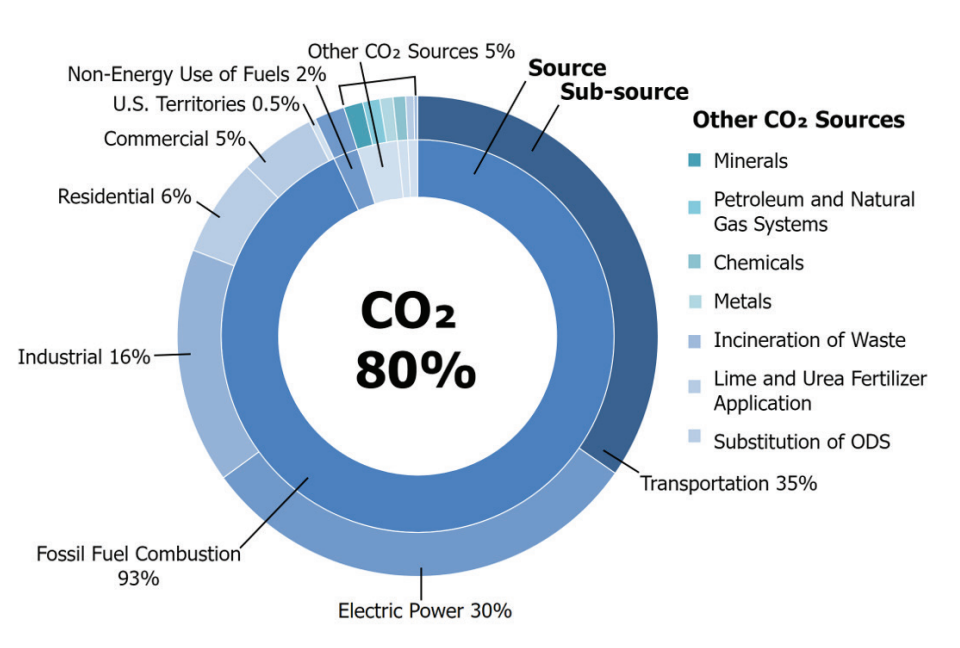

Figure 2. Carbon dioxide emissions sources in the U.S. in 2022

Source: U.S. Greenhouse Gas Inventory (EPA 2023). Carbon dioxide accounts for about 80% of U.S. territorial greenhouse gas emissions. Of these CO₂ emissions, roughly 93% come from fossil fuel combustion and about 2% from the non-energy use of fuels. Taken together, this implies that pricing the carbon content of fossil fuels upstream could cover approximately 76% of total U.S. greenhouse gas emissions.

This is one reason why most economists view a carbon tax as the most economically efficient carbon management policy. Yet this advantage may also be its weakness. Because its impact is so broad, a carbon tax can turn otherwise neutral parties into opponents. Even when policy design includes measures to offset potential increases in electricity prices, voters are less enthusiastic about taxes.

On the other hand, cap-and-invest programs have often proven more politically palatable, in part because they offer flexibility through market mechanisms (e.g., companies have the chance to pay less than a blanket tax) and can obscure costs relative to explicit taxation. While CBAM policies in other countries are beyond U.S. control, their practical impact on the U.S. economy is likely to be limited — affecting only a small share of emissions, albeit while imposing compliance burdens on the firms involved.

Counting carbon content earlier in the supply chain is administratively simpler than monitoring emissions and allocating them across individual products, especially when those products are manufactured abroad. This does not mean BCA is unnecessary. Rather, it can serve as a complementary policy that helps reduce the impact on domestic energy-intensive industries. Nonetheless, a BCA, or a scattered carbon accounting practice to comply with foreign BCA, without a domestic carbon price is the least efficient way to price the carbon.

After all, income taxes are more accurate and less costly when employers report compensation directly, rather than leaving every taxpayer to calculate their own earnings from scratch.