State policymakers interested in tackling child poverty, particularly for working families, have several policy levers at their disposal. Two of the most popular are refundable earned income tax credits (EITCs) and minimum wage laws. Building on the success of the federal EITC, twenty-five states also administered refundable EITCs in 2023. Thirty states also had minimum wages above the federal standard of $7.25 per hour.

Given how much progress states could make in reducing child poverty, many advocates continue to push for further expansion of these policies. Colorado saw a successful push to double the state’s EITC from 25% to 50% of the federal EITC this year. Massachusetts advocates, fresh off a successful campaign to raise the commonwealth’s minimum wage to $15/hour are now pushing for a $20/hour minimum wage. Advocates and policymakers often take the idea that “bigger is better” in both cases for granted. But is this always the case?

Evidence suggests that many states–particularly those where support for future expansions is gaining traction–are seeing diminishing marginal returns to expanding these policies regarding reducing child poverty. The case for shifting away from minimum wage and EITC increases – and toward refundable CTC expansions – is strongest in these states.

The EITC, minimum wage, and poverty

Congress introduced the federal EITC in 1974 to shield lower-income workers with children from payroll tax increases at the time. The EITC has grown into an income-tested tax benefit that phases in with earnings until reaching a maximum benefit based on the number of children in a family. It plateaus briefly before phasing out again for single parents earning more than $22,720 and married parents earning more than $29,640.

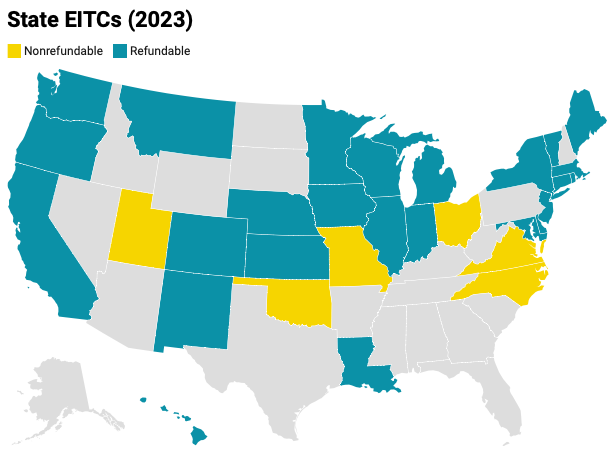

Recognizing the credit’s anti-poverty impact, states began enacting their own EITCs in the 1980s. As of 2023, 32 states and the District of Columbia had EITCs (26 refundable; 6 nonrefundable). State EITCs are typically set as a percentage of the federal EITC. Refundable EITCs ranged from 4.5% (DE) to 45% (CA) of the federal credit in 2023.

Figure 1: State EITCs, 2023

The introduction and expansion of state EITCs was a productive strategy for states looking to further reduce poverty given political and fiscal constraints during this period. EITCs are politically popular, relatively inexpensive, and effective tools for poverty reduction. The academic literature consensus is that the EITC reduces poverty, particularly for children.

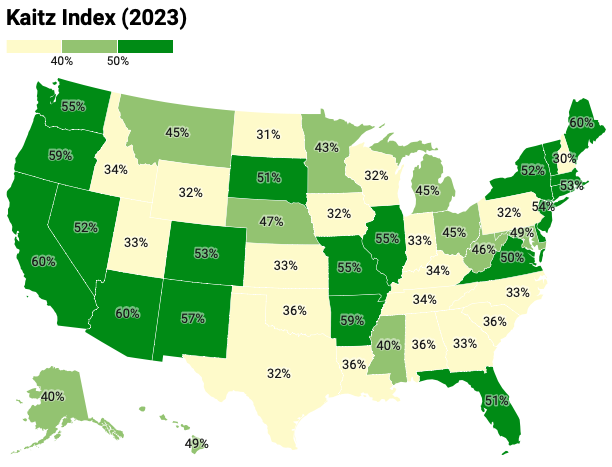

Similarly, states have pushed for minimum wage increases as part of this same effort to reduce poverty. In contrast to the EITC, the evidence of the minimum wage’s impact on poverty is mixed for two reasons. First, there are concerns about its impact on employment. In contrast to the EITC, which increases labor force participation, there have long been concerns that higher minimum wages drive up the cost of labor and thus reduce demand for it. The debate is ongoing, but recent evidence suggests that minimum wages set between 40-60% median wages have little impact on employment. When we examine state minimum wages in this context, we find that most states are in this range. Figure 2 shows the Kaitz index – each state’s hourly minimum wage as a proportion of their hourly median wage. No state exceeds the 60% upper bound. Twenty-one are greater than 50% and ten are greater than 40%. Nineteen states fall below 40% – but none fall below 30%.

Figure 2: State minimum wage as a percentage of state median hourly wage, 2023

The second issue stems from our ability to examine the impact of the minimum wage as it interacts with other anti-poverty programs. Early studies found that higher minimum wages were associated with a reduction in poverty but those findings have come into question. The key issue was that they often relied on the Official Poverty Measure (OPM), which excludes tax credits and SNAP benefits from its calculations. Studies using broader measures have found smaller impacts on poverty. This is because the loss of income-tested programs like EITC and SNAP often offsets increases in earnings. One study found this reduced the impact of a higher minimum by about one-third. Other studies have found no association between minimum wage laws and poverty.

These mixed findings complicate a decades-old strategy for pairing minimum wage increases with EITC increases to “make work pay” for low-income families. This strategy, popularized by the Clinton administration, seeks to reduce poverty through higher earnings and income supplements for low-wage workers. But that strategy only works if the relevant minimum wage is accurately aligned with the relevant income supplements.

Raising the minimum wage and expanding the EITC have received far more attention from advocates than assuring that they are properly aligned so that a parent working full-time at the minimum wage is also eligible for the maximum EITC benefit (and, ideally, other income supplements). Table 1 categorizes the 25 states with refundable EITCs by whether working full-time at that state’s minimum wage would put a single parent in the EITC’s phase-in range, plateau, or phaseout range.

Table 1. Where does a state’s minimum range put EITC-eligible workers?

| Working full-time at state minimum put family in state EITC phase-in range | Working full-time at state minimum put family in state EITC plateau range | Working full-time at state minimum put family in state EITC phase-out range |

| Indiana Iowa Kansas Louisiana Wisconsin | Montana Michigan Nebraska Minnesota | California Colorado Connecticut Delaware Hawaii Illinois Maine Maryland Massachusetts New Jersey New Mexico New York Oregon Rhode Island Vermont Washington |

The five states (IN, IA, KS, LA, WI) with minimum wages that put workers in their state EITC phase-in range are all bound by the federal minimum wage, which puts them below 40% on the Kaitz index. In these cases, increasing the minimum wage to align it with the EITC and “make work pay” for single parents makes sense. In four other states (MT, MI, NE, MN), their minimum wage (about $10-10.50/hour or about 43-47% of median wages) puts workers at the end of their state EITC’s plateau range. In these cases, it makes some sense to increase the EITC. Still, this approach risks further penalizing workers as they begin to move up the ladder and earn wages higher than the state minimum.

In the remaining sixteen states, however, single parents working full-time at the minimum wage find themselves in the EITC’s phaseout range. In these cases, raising the minimum wage above $11 per hour results in full-time workers receiving less than the maximum EITC benefit as each additional $1 is offset by a 16-21¢ reduction in their federal EITC and smaller reductions in their state EITC. Increasing the size of the state EITC (which is typically done as a percentage of the federal EITC) would increase the size of these reductions. These are the states where we see diminishing marginal returns to expanding the minimum wage and the EITC for poverty reduction. Some studies suggest the problem is even bigger when you account for other income-test benefits, with workers losing between 60¢ and 95¢ for each additional dollar they earn depending on the scope of benefits (EITC, SNAP, housing, childcare, etc.).

The limits of the maximalist approach

One takeaway is that there is some room left for increasing the minimum wage in states subject to the federal minimum wage, which was last increased in 2009 to $7.25/hour but left indexed. One option is to raise the federal minimum wage to $10/hour and index it for inflation. This would bring the nineteen states currently subject to the federal minimum wage up into the Kaitz index “sweet spot”, align them with the EITC “sweet spot” for single parents, and keep them there through automatic adjustments of both policies.

But that is not the case for the majority of states where the majority of working-class parents reside. Policymakers in these states cannot raise the minimum wage without pushing families into the EITC phaseout range. And, because state EITCs are set as a percentage of the federal EITC, they also do not have the proper levers to reform their state EITCs without totally decoupling them from the federal EITC. This is the limit of the traditional maximalist approach that relies on expanding both.

A more fruitful approach for advocates and policymakers in those states listed in Table 1’s last column, such as Connecticut, Hawaii, and Rhode Island, would be to shift focus away from efforts to increase state minimum wages and EITCs altogether and instead consider ways to introduce or expand fully refundable state child tax credits (CTCs) as the primary policy tool for reducing child poverty. The universal nature of fully refundable CTCs makes them particularly effective at reducing deep poverty while avoiding the pitfalls associated with traditional income-tested benefits. Recent reforms illustrate two potential avenues for this new approach.

The first, more straightforward approach is to convert existing state dependent exemptions and nonrefundable CTCs into fully refundable and more generous CTCs. Massachusetts and Maine offer the best models for this approach. While creating a new CTC wholesale rather than modifying existing tax benefits, Vermont offers a similarly good model. The universal or nearly universal design of these CTCs ensures that workers with children are not penalized when their earnings increase, whether because of minimum wage increases, pay raises, or working more hours.

Policymakers considering this approach must be careful to avoid the temptation to add onerous income tests that recreate the same issues with negative interactions between the minimum wage and state EITCs. For example, California, Maryland, and Oregon all created fully refundable state CTCs that begin phasing out at very low earnings threshold so that full-time minimum wage workers receive little or no credit at all. This only exacerbates the problem. Ideally, states would stick to universalism in design.

The second and more comprehensive approach is to completely decouple state EITCs from the federal EITC by converting them into fully refundable CTCs and restructuring them to better align with the needs of working-class families. New York’s proposed Working Families Tax Credit (WFTC) offers a good case study. The WFTC would consolidate the state’s EITC, CTC, and dependent exemption into a single, more generous, and fully refundable tax credit worth $1,600 per child. It would increase the phaseout threshold for single parents to $25,000, which is below what that parent would earn working full time at the state’s $15/hour minimum wage, but it would also reduce the phaseout rate from 5-6% to a flat 2%. This effectively reduces the penalty for parents earning minimum wage relative to the status quo. Minnesota, which has long decoupled its state EITC from the federal EITC, enacted similar reforms last year. The Minnesota CTC’s phaseout threshold is much higher than what a single parent would earn working full time at the state’s $10.59/hour minimum wage, but the phaseout rate is higher when families earn enough to put them over that threshold. Ideally, states would combine higher thresholds with lower phaseout rates when fiscally feasible.

Fully refundable state CTCs are the way of the future

For several decades, changes in the minimum wage and EITC were the two primary levers state policymakers had at their disposal for tackling child poverty. As we have highlighted elsewhere, the recent proliferation of fully refundable state CTCs offers a new policy lever and a new opportunity to rethink our approach to reducing child poverty.

Given the limits of the old approach, it is time for advocates in many states to drop it altogether and refocus their attention on properly designing fully refundable state CTCs and building support for them as the best way forward in the fight against child poverty.