Last week, hedge fund manager and outspoken libertarian Clifford Asness provided critics of the philosophy of limited government with a “gotcha moment.”

The COVID-19 outbreak is one that demands a strong and swift response from the libertarian’s instinctive enemy: the government. Bloomberg’s Justina Lee covered this “man bites dog” story quite well, accurately representing Asness’ comments and demonstrating his willingness to break from free-market, limited-government orthodoxy to address the greatest public health crisis in a century.

I cannot offer enough praise for Asness’ comments. Elite opinion matters, as Niskanen makes clear in its conspectus, and as an outspoken libertarian it’s good to show that this is not something to be downplayed and that protecting human life, and thus the ability to exercise the liberties we hold dear, means buckling down and giving the government the public health and economic tools it needs to fight a two-front war against a possible depression and COVID-19.

It’s always nice to find another libertarian out in the real world that isn’t drinking the Ron Paul Kool-Aid. But just like in a pandemic, where Asness recognizes the necessity of state intervention, a financial crisis made possible by the current design of financial regulation involves a cascade of poor choices made by individuals or individual firms having spillover effects that can drag an entire economy down. There’s a reason terms like “contagion” are used to describe a financial meltdown. And given the good chance that finance will be lining up for a bailout before this pandemic is over, it’s high time we recognize that what is true of public health is also true of finance: government inevitably plays a major role, and we would do well to set it up for disaster prevention rather than disaster mitigation.

From a libertarian perspective, government’s interventions in the financial sector can be grouped into two broad categories. The first I shall call “necessary evils”: instances where there is simply no feasible way for a strictly natural-rights framework to produce a functional financial system and government must create some rules of the road, or where the financial sector cannot help but benefit from interventions elsewhere in the economy. The second I shall call “unnecessary evils”: policies that go beyond creating the legal and institutional infrastructure necessary for the financial sector to exist and redistribute upwards and to less productive enterprises.

Necessary evils

A natural-rights framework cannot come close to explaining the rules and institutions of the financial sector. Basic liberty of contract fits well within the general model of borrowing and lending, but as things get more complex, man-made laws are required to define both the nature of legal rights and their enforcement. A natural rights “view from nowhere” doesn’t work in a system where institutions must be designed to serve a specific purpose.

To begin with the most obvious example, take the structure of the limited liability corporation itself (which touches virtually every firm, not just those on Wall Street or in Greenwich). If I negligently burn down your house, I could be personally liable to the point where I lose my own. If I am a shareholder in a company that builds homes with faulty wiring, I am only on the hook for the total value of my investment.

This is a strange disconnect from a worldview that centers on liberty of contract and the obligation to fulfill promises made, but it is one that is essential for the capitalist system to thrive. Skin in the game for investors is important, but many would be reluctant to put their savings on the line if it meant they could wind up losing a pound of flesh. As Mass. Gov. Levi Lincoln Jr. put it in 1830, “[t]he business of manufactures requires…the employment of large capital…But men, with the admonitions they have had, will no longer consent, for the chance of profit upon a share in a concern, to put their whole property at the hazard of circumstances, which they can neither foresee, nor over which they can have any control.”

Investment would be impractical and intolerably risky without the guarantees offered by this deviation from strict enforcement of contracts, and the intermediaries in the financial sector would find themselves with little to do without caps on liability for those looking to invest their funds.

Closely related to the structure of the limited liability corporation is bankruptcy law. Squarely in the domain of the federal government, bankruptcy law cannot be produced by translating natural rights into the corporate world. These rules provide predictability; are necessary to resolve issues related to insolvency or bankruptcy; determine who gets what, how much of it, and under what circumstances; and cannot be informed by even the most diligent reading of Anarchy, State, and Utopia.

Liberty of contract exists under a libertarian framework, of course, and the night watchman has a role to play when contracts are broken. But when it becomes impossible for Annie to fulfill the promises she made to Bob, there must be a formal resolution process. This process may approximate the principles of a libertarian conception of property rights and individual liberty, but it is impossible for it to be cleanly derived from them.

Last are the downstream effects of other regressive regulations and government interventions on the financial sector. If you invest in biotech startups or pharmaceutical companies, you’re profiting from the excesses of our current patent system. If you invest in media companies, you benefit from the absurdities of copyright law. Are you a shareholder in Amazon, Google, Foxconn, or countless other corporations that received tens of billions of dollars in subsidies from state and local governments? You can thank the local and state governments that offered them subsidies to set up shop in their jurisdictions. Don’t even get me started on farm subsidies.

This point is summarized well by Dean Baker in his paper “Is Intellectual Property the Root of All Evil?” (Spoiler alert: Yes).

“There are 15 people among this top 100 [richest people in the world] who are listed as getting their fortune from some type of finance. It is possible that much of their wealth stemmed from making a good bet on Apple or Microsoft or some other high-flying tech company whose profits depend on intellectual property.”

You can extend Baker’s logic to any subsidy granted to a firm that can be lent to or invested in. While the industries in question are the ones benefiting the most from these various forms of subsidy, the unique position of the financial sector is that all of these rents and interventions, when they work in a company’s favor, find their way into the hands of investors.

Unnecessary evils

As discussed above, it is necessary for the state to intervene by creating the legal infrastructure without which the financial sector could not survive. Every policy decision comes with tradeoffs, but some regimes are better than others. And the design of our current regime is not only structurally unsound; it also benefits from countless other bad policy decisions.

First and foremost, it is a system built on debt. As Brink Lindsey and Steve Teles point out in this reply to a critic of The Captured Economy, the entire framework of the financial sector is built on leverage by design and must be reoriented so equity reigns supreme.

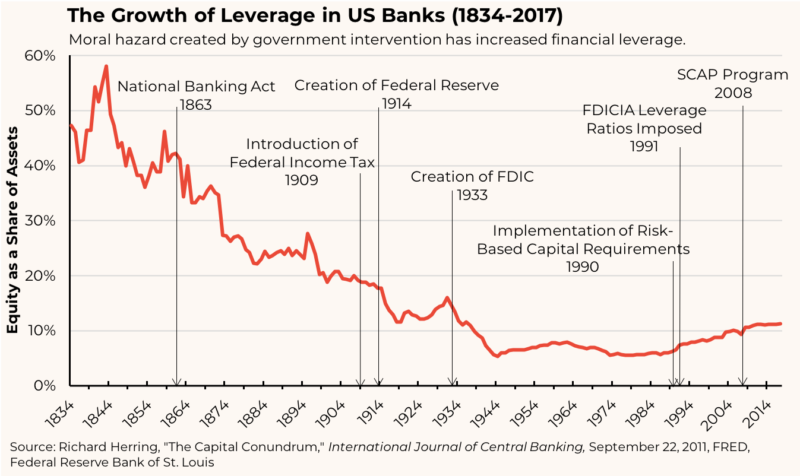

A number of permanent fixtures of public policy buttress our leverage-based system. The Fed’s lender-of-last-resort status is designed to provide emergency liquidity to banks that are leveraged to the hilt. Tax policy also privileges debt by making interest tax-deductible (though the 2017 Tax Cuts and Jobs Act changed some of that). The FDIC insures bank deposits for ordinary depositors (read: lenders). With the exception of the tax privileges, these stopgaps create moral hazard.

Prior to the COVID-19 outbreak, banks were around 11 percent equity-financed, whereas a healthy nonfinancial firm would be at least 25 percent equity-financed. On the eve of the 2008 financial crisis, banks were about 10 percent equity financed, while real non-financial firms were around 40 percent equity-financed. Research shows that banks are willing to forgo about 4-5 cents in profit if it means reducing capital by one dollar. You maximize return on equity the more leveraged you are, but that leads to greater risk.

And when you become too big to fail, that risk is passed on to the government. In this way, one can almost think of debt in the financial sector as a shadow national debt. Yes, the taxpayer technically made money on the Troubled Asset Relief Program bailouts, but such apologetics are just window dressing on a subsidy available to finance but unavailable to John Q. Public. Arguments about the federal government’s capacity to borrow aside, money appropriated to bailing out the financial sector is money that isn’t available for more broad-based stimulus when it’s needed most urgently.

Even aside from the more permanent institutions designed to support leverage, there’s most certainly a general belief that some government body (be it a legislature or central bank) will bail out struggling institutions. In the late ‘90s, private firms in Korea behaved as though they would be bailed out despite public statements from the government to the contrary. Other research found that in the United States, as regulatory capital fell, the value of an implicit government guarantee made up a larger share of the bank’s value. A more highly leveraged bank is more likely to become insolvent and thus rely on government support.

Reasonable people can disagree on whether this or that program measurably subsidized the financial sector in the form of greater support for risk-taking, but the evidence for the overall effect is there. And, as Lindsey and Teles argue, it is the constellation of policies built around leverage that matter most, not the effects of any one program.

Aside from subsidizing leverage, there are other ways the financial sector benefits from bad policy. Prior to joining the Niskanen Center two years ago, I worked at the Reason Foundation’s Pension Integrity Project, which exposed me to a different kind of subsidy to big finance: investing public-sector employees’ retirement funds in so-called “alternatives.”

I’ve been out of the game for a little while, but the single greatest driver of pension underfunding in the U.S. is the failure to set a reasonable assumed rate of return since the year 2000, especially since the 2008 crash. In the ‘90s, you could have a 60/40 split of stocks and bonds and easily meet a 7.5 percent or 8 percent assumed rate of return (ARR). But more recently, pension funds have had to “diversify” and invest in riskier assets to hit that target.

Rather than just accepting a lower ARR and paying more into the system, they’ve instead made investments that are both risky and expensive, because active management firms take a hefty management fee, often with little to no oversight. Pension reformers call this giveaway di-“worse”-ification, and it gives hedge funds a whole lot of money to make more money for themselves. But this happens because legislators refuse to raise the revenue needed to properly fund their pension systems.

You could say the same thing about the 401(k) retirement account structure. The economies of scale for institutional investing are massive, and if the government just set up its own index funds for individuals the fees would be minuscule relative to the size of the portfolio. Instead, many people miss out on significant retirement savings. Though some libertarians may miss this, the 401(k) is, just like Social Security, a subsidy. Subsidizing retirement savings is a good idea in general, but the current system gives managers a significant amount of money to skim off the top, when it could be done more efficiently with less of that money flowing to managers. For a counterfactual, look at John Bogle. He invented the index fund, and his net worth when he died was under $100 million.

This is, of course, not to say that hedge funds and active management do not have a role to play, and if you can make billions by doing your homework, as Asness has, good for you. But this is an industry that has benefited from the bad decisions of public sector employees’ retirement funds and the suboptimal design of key elements of U.S. retirement policy.

Finally, even some of the more progressive forms of redistribution that we rely on are also built around debt where a more straightforward tax-and-transfer scheme of redistribution would be preferable. When you create a system to subsidize lending (and related industries) through mortgage guarantees made by leveraged government-sponsored enterprises, you still leave an ordinary consumer or homeowner with debt that could cripple them if they lose their job. When the job loss is systemic, you get a catastrophe. When you give someone cash (e.g., first-time homebuyer down payment assistance), you’re still providing a subsidy for the desired purchase, but you’ve taken the risk associated with debt out of the equation.

Capital is the cure

Most of the economic literature points to an optimal capital requirement of greater than 20 percent of assets. This clean, blunt instrument has many supporters with strong free-market bona fides. John Cochrane supports a sort of sliding scale of regulatory supervision, with well-capitalized institutions being subject to relatively little regulation, and the most highly leveraged ones strictly scrutinized. Allowing greater relief for better-capitalized financial institutions is similar to the system envisioned by the Financial CHOICE Act, introduced in 2017 and aimed at rolling back portions of the 2010 Dodd-Frank Act, but the bill’s threshold of a 10 percent capital/assets ratio for lighter regulation should be significantly higher. Robert Eisenbeis recommended changing the bill by raising the floor from 10 percent to at least 15 or 18 percent, with even greater relief for better-capitalized banks.

While Alan Greenspan’s support among libertarians has fallen far since his days of being part of Ayn Rand’s “Collective,” he calls for capital requirements of 25 to 30 percent. I would argue that on top of whatever the economically optimal capital requirement is, the political costs of the dysfunction that arises from government bailouts demands an additional buffer. On the other side of the issue, Jamie Dimon may praise capitalism while decrying increased capital requirements, but by making the financial system riskier, he is contributing to a system that, if it fails catastrophically, could lead to unrest that leads to the undoing of the free market.

The most attractive solution to the Too Big to Fail (TBTF) problem is The Minneapolis Plan. The Federal Reserve Bank of Minneapolis, which proposed the plan in 2016, estimated that it would reduce the risk of a financial crisis so severe that it would require a government bailout from 67 percent to 9 percent over the next century. The three main pillars of the plan are:

- a 23.5 percent capital requirement for banks that are not systemically important;

- a 38 percent capital requirement for systemically important banks;

- a leverage tax for “shadow banks” with assets over $50 billion.

Why tax leverage? The negative externalities produced by leverage are a bit different than those produced by, say, pollution. Every ton of carbon I emit imposes a cost on others (however negligible my individual emissions are.) The negative consequences of leverage, however, only appear when there are a series of defaults that set off a chain reaction threatening the financial system.

Higher capital requirements would make the U.S. financial system far more resilient for reasons discussed above and continued below, but the leverage tax is also an important part of the story. The negative externalities posed by default, though technically different than those caused by, say, pollution, nonetheless impose real costs to third parties who become unwilling victims of my investment strategy. Some negative externalities are tolerable, but as shown in financial crises throughout history, these impose serious costs on society at large. Even if one could argue that efficiency demands a financial system as focused on leverage as ours is today (the opposite is true), the principle that you should not harm third parties with no say in your own action demands that these costs to others be taken into consideration. As Jerry Taylor says in his “Conservative Case for a Carbon Tax”:

Perhaps the strongest argument for unilateral action [by the creation of a carbon tax]—even in lieu of a global commitment—is that ethical considerations demand it. Simply put, one should not harm others, one should not damage the property of others, and one should leave enough for others when taking from common resources. It does not matter if others have imposed the same harm and not been held to account, that others will continue to impose identical harms without being held to account, that the one who harms gains more than is lost by the one who is harmed, or that the harmed party has imposed similar harms on others without being held to account.

Much as every person in a pandemic is a “walking negative externalit[y]” according to Asness, so too is every undercapitalized financial institution. Unlike in the cases of a pandemic or carbon emissions, the externalities in a financial crisis are pecuniary (a technical distinction that doesn’t necessarily imply lesser damage). But much as in a pandemic, the risks posed by individual risk-taking simply cannot be isolated to an individual.

Rather than relying on a complicated, opaque, and capture-prone web of agencies and departments, higher capital requirements would dramatically reduce the risk of the financial sector and safeguard the rule of law. I generally agree with Asness’ previous criticisms of restrictions on short selling and the complicated rules of Dodd-Frank which, even if they work on paper, are highly susceptible to capture. These command-and-control style regulations often become popular for no clear reason other than that they sound good and have been branded well. The idea of bringing back the Glass-Steagall separation of commercial and investment banking enjoys bipartisan popularity, but its merits stop there. The now-weakened Volcker Rule also has name recognition, and proprietary trading is a risky business, but it had nothing to do with the 2008 financial crisis. Financial innovation can leave regulators without the tools to address the next source of instability as policymakers play catch-up to the latest goings on in the industry.

Its focus on the beating heart of any financial system, capital, makes the Minneapolis Plan helpful across a wide range of contingencies. Look back on 200 years of banking failures in the United States, and you’ll see that the particulars are quite different. The subprime mortgage crisis was centered on the housing market; the savings and loan crisis came about when rising interest rates made the fixed-rate lending of S&L banks unworkable; the 1929 stock market crash was fueled by investors unable to cover their margins engaging in a massive sell-off; the bursting of the railroad bubble in 1873 led to a panic that year; the list goes on.

Greater regulation and oversight in the sectors which fueled their respective banking crises could have prevented overinvestment from turning into a bubble, and regulations tailored to address problems of a specific industry exposed by the popping of its bubble may be necessary. But that’s fighting the last war. What turns the bursting of a bubble into a full-blown crisis is leveraged investment.

For a counterexample, look at the dot-com bubble at the turn of the millennium. Many of the overvalued internet companies went bankrupt, but there were no bailouts, and certainly not to the financial sector. Why? The dot-com bubble was an equity-fueled bubble, while the subprime mortgage crisis, the 1929 crash, and other crashes associated with bank failures were debt-fueled. As Robert Hall of the Hoover Institution explained:

In 2001, the value of business assets, especially tech-related assets, fell dramatically, but the financial system showed no signs of stress. Financial institutions had little exposure to business assets. The stock market communicated losses directly to investors with no bank-like intermediation. In the Great Recession, banks and other financial institutions became insolvent or nearly so because of direct and indirect exposure to real-estate values. The stock market fell by about the same percentage in both recessions. In the Great Recession, the fall occurred because the adverse forces from the real-estate crash appeared to threaten a collapse of the whole economy.

It wasn’t exactly a fun time to be on Wall Street when the dot-com bubble burst, but imagine how much worse it would have been if, instead of venture capitalists and other investors with money taking the hits, the investments had all been leveraged.

A little leverage is fine, but having a financial system just over 11 percent financed by equity, giving it a leverage ratio just shy of 10:1 (as of the end of 2019), far greater than any of the other industries to be bailed out or that may be bailed out in the future, is courting disaster.

Defensive regulation

In a very technical sense, Niskanen’s preferred design for the financial sector, one based on significantly higher capital requirements, is a regulation. It is the government requiring private firms to do something or face penalties. These are sensible, beneficial rules for reasons discussed above and below, but let’s put ourselves in the position of a hardcore libertarian who opposes almost all forms of regulation. Maybe regulations, almost anywhere they are found, are bad policy or unacceptable limitations on the rights to free exchange.

Even if this is the case, libertarians should support higher capital requirements. Inherent features of the financial system make it crisis-prone, and even if, for whatever reason, it is better to let banks fail, the overwhelming majority of Americans who aren’t libertarians won’t see it that way. We must protect the capitalist system from political unrest that would undermine it, a strategy I call “defensive regulation.” There are realistically only two basic forms of regulatory regime available. Even if both are worse than the ideal, zero-regulation worldview, we must choose the one that provides the best defense.

Due to the leverage ratchet effect, the history of TBTF, and the fact that you’re about as likely to find a true homo economicus on Wall Street as you are a Yeti on the moon, bailouts are going to happen when the financial sector runs into trouble (and it will). And, for all the reasons I listed above, governments simply cannot credibly promise to not bail out failing banks, policy merits aside. Add in bailout apologetics (“but the taxpayers made money!”), and I think the evidence is compelling that while major financial institutions don’t necessarily want to be bailed out, government can’t credibly guarantee it won’t turn to bailouts when the going gets tough.

Even if capital requirements are, technically speaking, a form of government intervention, large-scale bailouts are an intervention far more offensive to libertarian sensibilities, as they combine a reward for excessive risk-taking with massive amounts of government money. There are only two politically viable alternatives, and higher capital requirements are the more market-friendly one. Better-designed “necessary evils” make it so we never need to use the unnecessary ones.

Conclusion: No neutral design

One can be a libertarian and still work in the financial sector, the same way one can work in arms manufacturing, or for the police, or any other government body. There is a whole universe of policies relevant to the libertarian project separate from those industries. And, as Asness points out, most libertarians aren’t anarchists. Nevertheless, the entire financial sector is a creature of the state. Expanding the set of available actions to financial institutions isn’t a question of more versus less government; it’s a question of one set of policy choices versus the other.

Virtually every other facet of life is also shaped directly or indirectly by policy, but what makes finance different from a libertarian perspective is that cannot function like an industry in the “real economy.” If our government were like a Nozickian state backed into without really trying, which respected liberty of contract and property rights but did little else, the day-to-day functioning of the butcher, baker, and candlestick maker wouldn’t look too different from a legal regime with LLCs, bankruptcy laws, and all the other legal institutions common to today’s corporate world. As explained above, the financial sector is different, and its basic design is to work within the legal infrastructure created by government.

In finance as in the current pandemic, restrictions on what could be fairly described as liberty of contract and association are necessary when individuals simply cannot internalize their risk-taking to the extent necessary to avoid serious harm to others. And in both cases, straightforward rules are necessary to prevent catastrophes that will lead to even more aggressive and unjust interventions in the future. For the sake of preventing the “contagion” of default and massive upward redistribution in the form of bailouts, our financial sector must be made both leaner and more robust by recognizing the inherent risks posed by the industry, and the fact that it relies on the state to exist.