In response to the economic crisis caused by the COVID-19 pandemic, Congress has just passed a $2 trillion spending package, the Coronavirus Aid, Relief, and Economic Security Act (CARES). Although it was put together very quickly, the macroeconomic impacts of this fiscally enormous piece of legislation will be felt for years. The following commentary highlights some of its important macroeconomic implications.

Stimulus or lifeline?

Not surprisingly, CARES has been widely compared to stimulus measures enacted at the onset of the Great Recession — the Economic Stimulus Act of February 2008, the Troubled Asset Relief Program (TARP) of October 2008, and the American Recovery and Reinvestment Act of February 2009. Although the total cost of those three laws was comparable to that of CARES, the new law is differently targeted and will affect the economy differently.

One important difference is that the 2007-09 recession was largely the result of a massive shock to aggregate demand triggered by the contraction of lending and the collapse of housing prices. In this case, the initial shocks have come from the supply side, first in the form of interrupted supply chains, then as sick and frightened workers became unable to report to their jobs, and finally, the policy-induced shock of shelter-in-place orders. (See here for a detailed discussion of the difference between supply shocks and demand shocks.)

As a result, restoration of aggregate demand will not be enough to restart the economy. At least in the short run, the checks being sent out to individuals under CARES will be more important as social policy than as macroeconomic stimulus. In fact, if we go by the results of similar payments in 2008, it is likely that a substantial part of this round will go into precautionary savings, as a hedge against worsening of the crisis, or into debt repayment, which, in economic terms, is another form of saving. For many people, these payments will make the difference between moderate and extreme hardship, but they will do relatively little to induce an immediate rebound of GDP.

A further difference is that the 2008 crisis was triggered primarily by a meltdown of the financial sector. On the whole, banks have come into this crisis with much better capitalization than they had in 2007. Consequently, there is nothing in the CARES Act that is comparable to TARP, which was aimed at recapitalizing banks and other financial institutions. If trouble does again develop in the banking system (which we cannot rule out if the present crisis goes on long enough), then resolving it will require new legislation.

Effects on the deficit and debt

Although worries about the federal deficit and debt have not been central to the debate over CARES, it is still the case that a trillion here and a trillion there will eventually add up to real money. It is worth giving a little thought to how this new legislation will affect the federal debt and deficit.

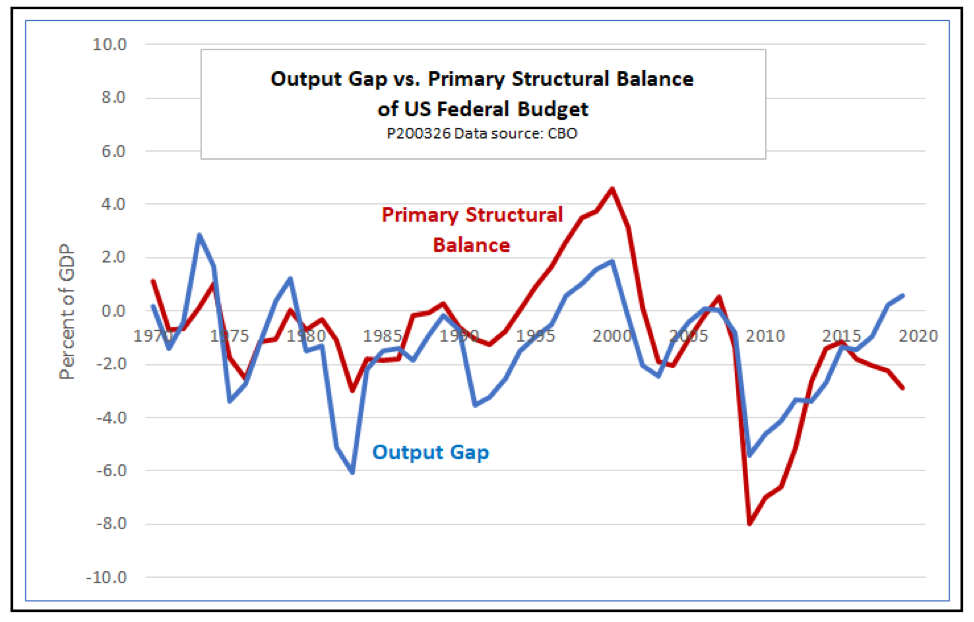

The first thing to note is the highly unusual stance of fiscal policy going into the coronavirus crisis. As the president never fails to remind us, the economy, through 2019 and into the beginning of this year, was exceptionally strong. One standard measure of that strength is the output gap. The output gap is the difference between current GDP and potential GDP, which is an estimate of the level of output that can be produced in the long run without overheating the economy. According to the Congressional Budget Office, the output gap for 2019 was +0.6 percent, the strongest since the peak gap of +1.9 percent achieved at the end of the dot-com boom of the 1990s.

According to orthodox rules for fiscal policy, the government should apply fiscal stimulus when the economy is in a slump, as indicated by a negative output gap, and fiscal restraint during a boom, when the output gap is positive. Fiscal stimulus or restraint can be measured by the primary structural balance (PSB) of the federal budget, that is, the surplus or deficit, excluding interest payments and adjusted to reflect the state of the business cycle. (See this slideshow for an overview of the mathematics of debts, deficits, and the PSB.)

The following chart plots the stance of fiscal policy, as measured by the PSB, against the business cycle, as measured by the output gap, over the past 50 years. The chart shows that as orthodox rules would prescribe, the PSB moved into surplus at the business-cycle peaks of 2000 and 2007, and then into deficit during the subsequent recessions and recoveries. However, from 2017 to 2019, as the output gap closed and then turned positive, the PSB reversed course. Rather than moving into surplus, it dove further into deficit, reaching a value of -2.9 percent in 2019. An inspection of the entire chart reveals that the movement of fiscal policy toward increased stimulus as the business cycle approached a peak is unprecedented in the last half-century.

The stance of fiscal policy, in turn, has implications for the dynamics of government debt. At any given time, there is a value of the PSB that is just sufficient to hold the ratio of debt to GDP constant over time. At present, federal debt held by the public is about 80 percent of GDP, the nominal rate of interest on the debt (measured as net interest per dollar of net debt) is about 2.3 percent, and the expected long-run growth rate of nominal GDP is about 4 percent, including an allowance for 2 percent inflation. Given those numbers, a primary structural balance of -1.36 percent of GDP would be needed to hold the debt ratio constant at 80 percent in the long run.

As of 2019, the PSB, at -2.9 percent, was already farther in deficit than its steady-state value. As a result, the debt was already on a path toward growth even before the coronavirus crisis began. If 2019 conditions had continued indefinitely, the debt would have grown toward a steady-state value of about 170 percent of GDP.

Now, of course, the debt will grow much more rapidly, at least in the short run. Partly that is because CARES will increase the PSB as a percentage of potential GDP by several percentage points. Partly also it is because GDP itself will decrease by an unknown amount for an unknown period of time, thereby severely eroding federal revenues. However, if the economy returns to its initial long-run path of 4 percent nominal growth and if interest rates remain at recent levels, the long-run steady-state level of the debt ratio will remain unchanged at about 170 percent of GDP. We will just get there several years sooner.

The good news is that as long as the interest rate on the national debt remains lower than the growth rate of GDP, the ratio of debt to GDP will always have a finite ceiling. The theoretically possible “exploding debt” scenario, in which the debt ratio grows without limit until wiped out by default or hyperinflation, looks unlikely, based on trends of interest rates and growth that seem well-anchored.

Keep in mind that in comparing interest rates to inflation, both must be stated in nominal terms or both in real terms. Do not panic at the thought that the 2.3 percent figure given above for nominal interest payments as a percentage of GDP is higher than the widely reported real GDP growth of 2.1 percent for 2019. Nominal GDP grew by a full 4 percent last year, when inflation is figured in. Furthermore, looking forward, a case can be made that we should be looking not at total interest payments as a percentage of outstanding debt, but instead, at the cost of financing newly issued debt. As of March 25, those rates ranged from 0.19 percent on the 1-year T-bill to 1.45 percent on the 30-year bond. Those ultra-low rates in part reflect the renewed program of quantitative easing undertaken by the Fed in mid-March, but even before that action, at the beginning of March, borrowing rates were just 0.89 percent for the 1-year T-bill and 1.66 percent for the 30-year bond.

The restart

From a macroeconomic point of view, the most difficult and least certain phase of the coronavirus crisis will be restarting the economy once the public-health aspects of the pandemic are tamed. CARES has some provisions that will help the restart:

- Loans to small businesses will be forgiven if they are used to maintain payroll during the crisis. That will maintain a connection between small-business employers and their workers.

- The Treasury is empowered to channel aid to corporations not just in the form of loans, but also “through the use of such instruments as warrants, stock options, common or preferred stock, or other appropriate equity instruments.” A lower debt burden should make it easier for companies to restart operations while still allowing the government to recoup sums advanced during the crisis.

- Numerous changes to regulations regarding student loans, Pell Grants, work-study programs, and related forms of student aid should make it easier for students to weather the crisis and for educational institutions to resume operations once the pandemic has died down.

These provisions and others will mitigate supply-side constraints that might otherwise prevent firms from resuming their operations. However, even after those constraints are lifted, production will not be able to get back to normal without adequate demand. CARES is strictly a short-term measure. It is entirely possible that additional demand-side measures will be needed well into the recovery.

One of the dangers ahead is that unwarranted alarm over the increase in the federal deficit and debt will bring renewed calls for budget austerity. To succumb to the temptation to tighten fiscal policy before the recovery is complete would be to repeat a mistake made during the recovery from the Great Recession. That premature tightening of fiscal policy can be seen in the above chart at the point where the red PSB line moves above the blue output-gap line after 2013.

In a prescient 2017 paper, economists Alan J. Auerbach and Yuriy Gorodnichenko warned against a repetition of premature tightening during the inevitable next recession. Studying the experience of several countries during the recovery from the Great Recession, they concluded that fiscal policy “was not used to full potential, given the depth of the recession.” While cautioning that governments should not recklessly finance “bridges to nowhere,” they concluded that concerns over debts and deficits should not block appropriate fiscal stimulus. In fact, they found that “fiscal stimulus in a weak economy may help improve fiscal sustainability” rather than undermining it.

We should heed their warnings as we enter, and eventually emerge from, the onrushing coronavirus recession.