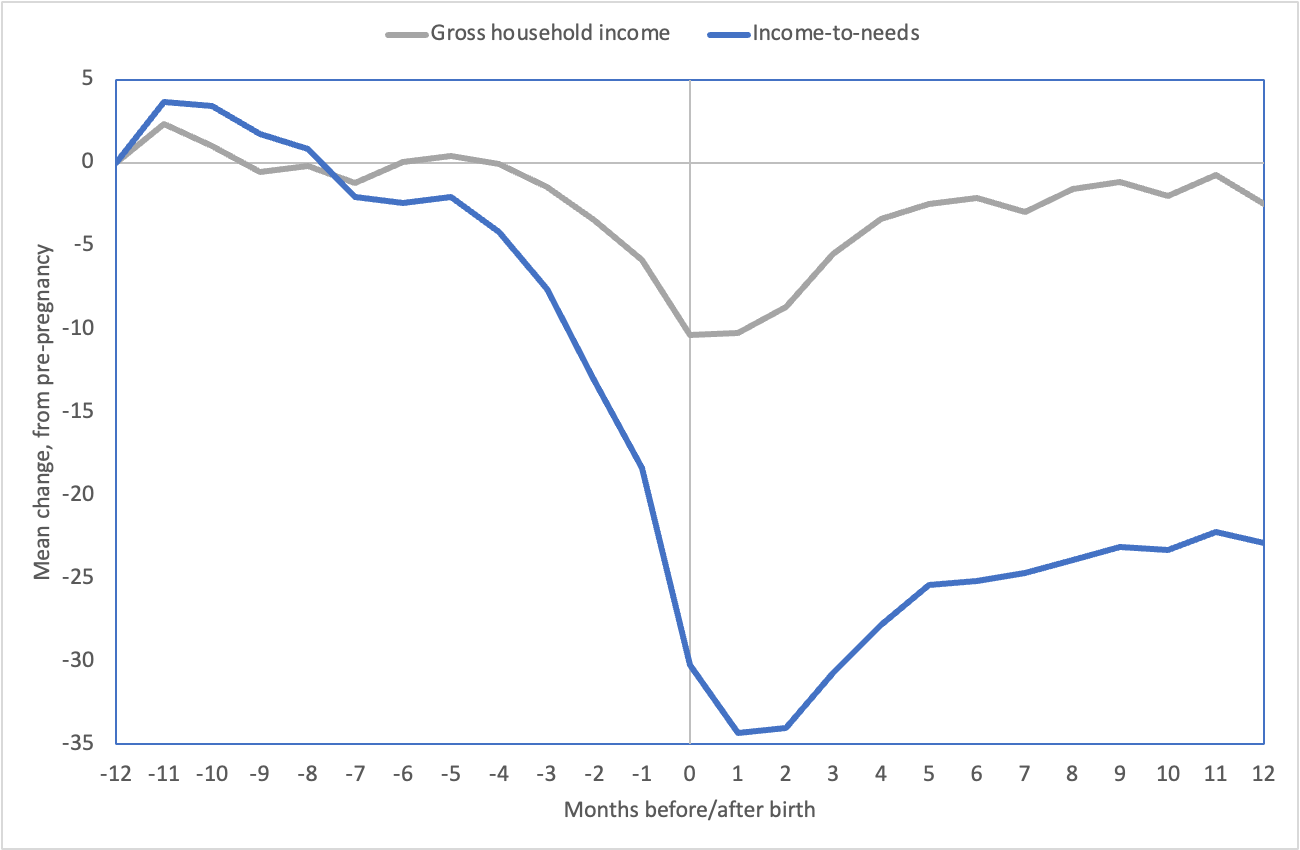

Welcoming a new baby is one of life’s greatest joys, but it can also bring temporary disruptions to household income stability. New parents face a dual burden: a decline in income as they take time off to care for their newborn, and a rise in expenses related to childbirth and preparing for their baby’s arrival. The combination of reduced earnings and increased costs makes it more difficult for families to grow, as shown in Figure 1 illustrates.

Figure 1: Declining income and rising needs around the birth of a child

This issue is not insurmountable. Parents with access to paid parental leave, whether through their employer or one of the thirteen states that have adopted contributory programs, can replace a portion of their lost income with benefits to reduce some or all of their earnings losses. However, data shows that 73% of workers lack access to paid leave through their employer. Even in states with paid leave programs, about 25%of prospective new parents are ineligible due to insufficient work history, leaving a significant gap in coverage for families.

New York introduced a contributory paid leave program in 2016 and phased in benefits over several years. Since 2021, new parents who meet the work history requirements are eligible for up to twelve weeks of benefits, amounting to 67% of their previous average weekly wages, capped at 67% the statewide average weekly wages ($1,151 in 2024). While most eligible parents can take time off without significant financial strain, low-wage workers–particularly those who were working part-time before the birth– may find their paid leave benefit insufficient to cover the full twelve weeks of bonding time. Additionally, parents who do not meet the minimum work requirements receive no benefits to offset lost income or manage the added expenses of a newborn.

Complementing paid leave with a baby bonus

In Left Out: A framework for non-contributory paid parental leave, we highlighted several shortcomings of traditional contributory programs and explored options for designing secondary programs to complement state contributory programs. One such option is a “baby bonus,” which could be administered as a tax credit paid out following the birth of a child.

A new bill (SB 9885A) from New York State Senator Jacob Ashby (R) proposes a $1,000 fully refundable tax credit for families with newborns. According to Ashby, the goal is to provide support for young people as they navigate the rising costs of raising children. Notably, the credit would be universal, meaning all families with a newborn would be eligible, regardless of income level.

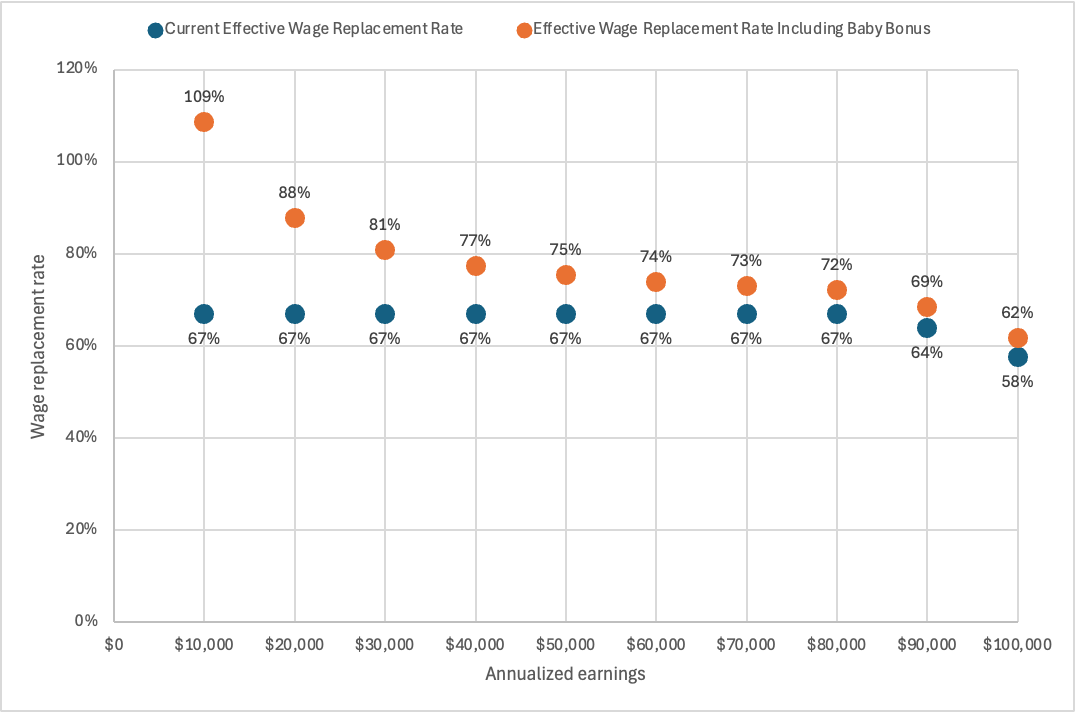

Complementing New York’s existing paid leave program with a baby bonus offers two key advantages in supporting parents with the costs of starting or growing their family. First, it effectively increases benefits for families already eligible for the state program in a progressive manner. Figure 2 demonstrates the potential impact of a $1,000 baby bonus, assuming it could be used to supplement paid leave benefits over a 12-week period.

Figure 2

Under the current system, workers earning less than the statewide average weekly wage receive a 67% wage replacement rate, which decreases as earnings rise above the average. A flat $1,000 income supplement would increase replacement rates for all workers, with the most significant benefit increases going to those with the lowest wages. For example, a new parent earning $250 per week could see their full wages replaced for the entire twelve-week leave period with the help of this supplement.

Additionally, new parents who do not meet the minimum work requirements–whether due to being in school or having left employment for health issues related to pregnancy–would still be eligible for the baby bonus to help with the associated costs of a new child. This advantage is unique and cannot be achieved by simply adjusting wage replacement formulas. Implementing this policy would position New York as a leader in policies supporting newborns and parents.

Administrative reforms can help ensure speedy delivery

Providing new parents with a baby bonus in the form of a refundable tax credit offers numerous advantages, but there are opportunities for policymakers to improve how these benefits are delivered. Typically, households receive tax credits as part of their annual tax refund (usually between February and April of the following year). Under this current system, new parents might face a long wait–potentially months or even up to a year– before receiving the proposed baby bonus. In response, New York is one of several states exploring the option of advanced payment for refundable tax credits, allowing families to access these funds more quickly when they need them most.

The proposed baby bonus presents an ideal opportunity to pilot advanced payment systems. Since the credit is not income-based, there would be no risks of end-of-year clawbacks, which have complicated other advanced payment programs. New York could streamline the process by integrating the baby bonus application with existing forms that parents complete at the hospital, such as for a Social Security number or birth certificate. This documentation would be forwarded to the Department of Taxation and Finance alongside forms sent to the Social Security Administration, allowing the state to verify claims efficiently. As a result, parents could receive the baby bonus via direct deposit shortly after birth.

Whether administrative reforms happen now or in the future, the proposed bill represents a significant advancement for policies supporting families across New York. It offers crucial financial relief to all families with newborns and lays the groundwork for future improvements in how benefits are delivered.