In my previous essay, I argued that the energy transition could occur more quickly than many believe because no reasonable investors will be willing to continue backing oil and gas companies. As financing dries up, supplies will decrease, prices increase, and the shift toward renewable and other energy sources will accelerate. While making that argument, I cited the work of Daniel Yergin, Vaclav Smil, and others who believe that the energy transition will be decidedly more gradual. They think that is the case because our physical infrastructure, built around fossil fuels, will prevent a rapid change.

Smil details this thesis in a January 2014 Scientific American article. His basic argument in it is that the shift to renewables as advocated by proponents such as Amory Lovins of the Rocky Mountain Institute (a clear foil to Smil) would require a “fundamental reshaping of our modern energy infrastructure.” He comments that huge sums have been invested in the existing infrastructure, and thus, change would be impossible:

Even if we were given free renewable energy, it would be economically unthinkable for nations, corporations or municipalities to abandon the enormous investments they have made in the fossil-fuel system, from coal mines, oil wells, gas pipelines and refineries to millions of local filling stations—infrastructure that is worth at least $20 trillion across the world. According to my calculations, China alone spent half a trillion dollars to add almost 300 gigawatts of new coal-fired generating capacity between 2001 and 2010—more than the fossil-fuel generating capacity in Germany, France, the UK, Italy and Spain combined—and it expects those plants to operate for at least 30 years. No country will walk away from such investments.

The facts do not support Smil’s assertion. Businesses often close factories or scrap equipment long before they reach the end of their useful lives. Unlike human beings, capital goods are kept in operation only as long as they can operate profitably.

The term “sunk costs” applies to almost all capital goods. Once a good is built, the money spent to construct it has been spent, and little of it can be recovered. Smil seems to believe owners will continue to use equipment or factories until they wear out. History shows this view is incorrect.

In the 1950s, thousands of steam locomotives were scrapped while still fully functional, much to train buffs’ sadness. The locomotives lost out because they could not compete with the less-expensive, more reliable diesels.

Between 2010 and 2020, more than 200 coal-powered plants have shut in the US or been reconfigured to operate with natural gas because they cannot produce electricity with coal at the low costs achieved with renewables and gas. The New York Times ran a four-page article on October 6, 2020, on the closure of coal-fired power plants in Arizona and Kentucky. The front-page piece explained that the plants were shuttered because they cannot compete.

As economic progress drives down the cost of renewable energy supplies, we will see more coal-fired plants and other types of capital goods such as automobiles scrapped well before their usefulness comes to an end. Harvard economist Joseph Schumpeter described this process as “creative destruction.”

Writing these comments also prompted me to think of the myriad aircraft mothballed in deserts around the world. The website “airplaneboneyards.com” displays acres and acres of aircraft parked in arid locations, some being preserved for future use, others scavenged for parts. As the website emphasizes, many of these vehicles are no longer viable aircraft.

However, many more jets were retired before that point. Take the Airbus A380. Today all but eighteen of the two hundred forty-three A380 jumbo jets built are grounded. Most will never see passenger service again despite being operational aircraft. One Wall Street Journal article shows Air France A380s parked forlornly in Spain, all taken out of use permanently.

Reuters published a timely article on aircraft boneyards on September 13. It seems the firms that dismantle aircraft are seeing a surge in business as airlines seek spare parts from planes prematurely scrapped. Used parts such as engines reduce the need to make costly repairs on planes still in operation. Up to one thousand planes could be dismantled over the next three years compared to the four or five hundred scrapped annually since 2016. Early retirements account for the surge, and more are expected as airlines and leasing companies cut losses by selling planes for scrap.

The Journal article by Scott McCartney, author of the travel commentary “The Middle Seat,” reminds us that consumers and technologies, as well as engineers and managers, determine how fast Smil’s “enormous investments” get abandoned. Aviation provides an excellent example of this.

The Boeing 707 was the first profitable commercial jetliner. It took flight initially in October 1958, traveling from New York to Paris.

Jets such as the 707 proved extraordinarily popular with passengers and airlines. The travelers liked the comfort (this before, of course, airlines began packing people in like sardines) and the speed. Airlines also liked the substantial cost savings provided by jets, which were much less expensive to maintain than piston-powered propeller aircraft.

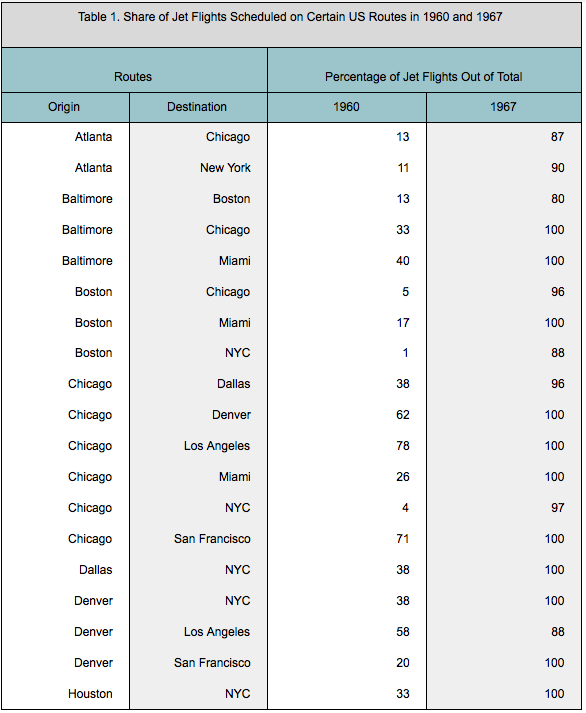

As a consequence, airlines bought and introduced jets on routes as quickly as they could. I collected data on the propeller and commercial jet flights for numerous city pairs by sheer accident when writing my Ph.D. thesis. The data cover 1960 to 1967, the time when jets were coming into use. As Table 1 shows, the percentage of jet flights on various city pairs rose dramatically over those eight years.

During the 1960s, airlines hastened to adopt jet service to remain competitive. They retired their prop-driven planes just as rapidly. Many of these went to airline boneyards and were scrapped long before their useful lives were done.

The telephone industry experienced a similar transition. AT&T’s control over the landline phone business ended in 1984 when the Regional Bell Operating Companies (RBOCs) were broken up. The Bells were left with the local landline phone service, including millions of miles of phone lines, phone exchanges, and other assets. Chaos followed.

Many of the former RBOCs did not survive as going concerns. One reason for this was technical change. In 1984 when the RBOCs were divested, mobile telephony did not exist. The consequences of its appearance and explosive development were grim for most of the ex-Bells.

New York Bell Telephone, one of the survivors, morphed into Verizon Communications. It also acquired many other RBOCs while transforming rapidly into a different type of communications company, selling off its landline business wherever possible. A large number of those buyers later went bankrupt.

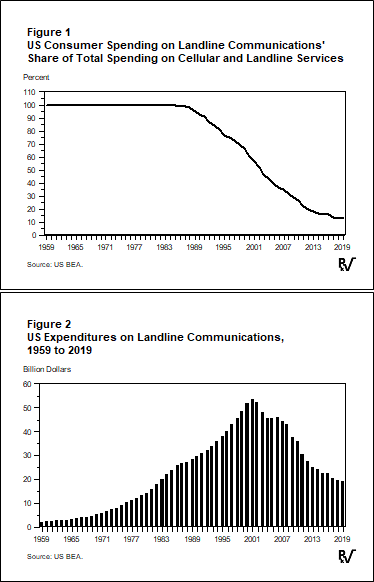

Consumers “cutting the cord” was a primary cause of such bankruptcies. As Figure 1 illustrates, customers were quick to abandon landline phones for cellular ones. The graph shows the percentage of US consumer expenditures on phone services allocated to landlines out of total consumer expenditures on telephone services. These data, compiled by the Bureau of Economic Analysis, are telling. In 1984, traditional phone companies captured all the consumer dollars spent on phone services. In 2019, that share had dropped to 10 percent.

Figure 2 shows the total US expenditures on landlines by year. In 2001, these peaked at $53 billion. They subsequently fell to $20 billion in 2019 as the percentage share of spending plummeted to 10 percent.

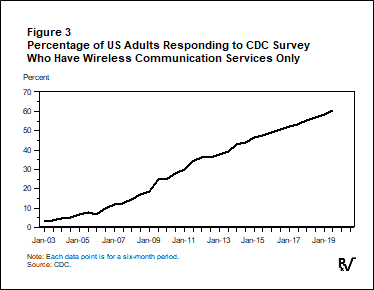

The decline in the landline market share was so large because the cellphone creators, especially Steven Jobs at Apple, had established a brand-new market that grew from nothing in 1984 to $120 billion in 2019.Meanwhile, companies that invested in landline infrastructure must recognize that many assets they built or purchased expecting to earn returns for twenty-plus years must be written off today, even though the equipment and wires have years of useful life remaining. They must do this because, as Centers for Disease Control data show, in 2019 the proportion of adults with no landline phone service, that is, people who used only wireless cellular phones, exceeded sixty percent (see Figure 3). That proportion may be even larger now.

The experience of the airlines and landline local-service phone companies demonstrates the fallacy of Smil’s statement that “it would be economically unthinkable for nations, corporations or municipalities to abandon the enormous investments they have made in the fossil-fuel system.”

Smil and many others writing on the permanency of investments fail to understand the importance of two factors: changes in technology and shifting consumer preferences. Both factors matter.

Technology advances can render long-term capital investments worthless and require assets to be scrapped long before they wear out. The examples of this abound.

- US railroads invested substantially in new “streamliner” passenger equipment immediately after World War II. Railroad executives expected Americans would resume their visits to relatives living great distances away. They did, but they chose to travel by car or air. Passenger rail use died quickly, and passenger railroad cars, new and old, had to be scrapped. Economist Franklin Fisher wrote the passenger trains’ epitaph in his 1960 paper “The Survival of the Passenger Train: The Demand for Railroad Transportation between Boston and New York” [no online version available]. In it, his econometric analysis showed that rising income would doom most rail services.

- In the computing world, the microcomputer’s introduction, followed by the personal computer (PCs) and then handheld devices (PDAs, cellphones, and tablets) with computing capacity that dwarfs that of the then-groundbreaking 1960 mainframes, forced those who invested in large scale computers to scrap or redesign and repurpose units long before they would have stopped functioning. In some cases, the billions they put into plants to manufacture the equipment also vanished. IBM, for example, lost $8 billion in 1993 because it failed to adjust quickly enough to the personal computer revolution.

- In the energy sphere, coal mines are being closed long before their streams are exhausted because customers no longer buy their product. Murray Energy, the fourth-largest coal producer in the US, became the eighth such company in 2019 to file for bankruptcy protection. Others followed as utilities closed coal-fired generating plants.

- Refineries are closing as well, heading for the scrapheap, long before their productive lives would have ended, even though Smil suggests they would keep operating. In 2020 alone, three refining facilities in California, possibly the world’s most important fuels market, have closed or announced shutdowns. They have done so because consumer demand for gasoline in the state is falling and because alternative energy sources have become available.

- As noted above, coal-fired power plants are being closed across Europe and the US. A reporter for Phys.org noted that 289 plants had shuttered in the United States since 2010, comprising 40 percent of the country’s coal-fired generating capacity. A Sierra Club representative explained that the shutdowns occurred “because the economics don’t work out.” A further thirteen plant closures have been announced in 2020. These also happened because the economics did not work. Today, electricity can be provided for less by other technologies.

Shifting consumer preferences can also force the abandonment of investment in viable production facilities. I have already discussed the changeovers from rail travel to air, from piston-powered planes to jets, and from landlines to cell phones. There are numerous other examples.

- Consumers abandoned the use of photographic film and cameras for their cellphones, bankrupting many film and camera firms.

- Consumers have embraced shopping online, mostly from companies such as Amazon, causing thousands of “brick and mortar” retailers to suffer large losses or fail.

- The hundreds of passenger steamships built to take travelers from one continent to another after World War II faced scrappage while still functional as airlines took market share. Today, cruise ships may confront the same fate due to travel shifts brought on by the Covid-19 pandemic.

- Investments in many of “the millions of local filling stations” mentioned by Smil have been written off as larger, better facilities were built, sales shifted to hypermarkets, and new roads were built that bypassed cites.

I could go on, but the point has been made. Financial theorists tell us out that whenever a firm invests in physical capital, one of the implicit costs they incur is giving up the option of waiting for more information. Twenty years ago, instead of building coal-fired plants with a lifespan of 50 years, utilities could have waited to see what would happen to the cost of renewable energy. Given what they knew, they chose rationally in giving up the option of waiting. Still, in doing so, they ran a risk. Now, with renewable prices falling rapidly, they have lost their gamble but, too bad. Sunk costs are sunk, and bygones are bygones.

Investors always confront the risk of a project becoming obsolete long before it earns its expected return. As noted, in many cases investments get scrapped well ahead of when their ability to function productively would end.

The conclusion, then, is that the data refute Smil’s blithe dismissal of a transition away from fossil fuels:

It would be economically unthinkable for nations, corporations or municipalities to abandon the enormous investments they have made in the fossil-fuel system, from coal mines, oil wells, gas pipelines and refineries to millions of local filling stations—infrastructure that is worth at least $20 trillion across the world.

The entire $20 trillion of value he mentioned could end up being written off if technology, circumstances, or consumer preferences continue to change as they have been.

In 2011, an earthquake and tsunami ended the use of nuclear power in Japan almost overnight. While the energy transition off hydrocarbons will not happen that quickly, it will happen much faster than the glacial pace many seem to expect. Those individuals would do well to remember the words of former Saudi oil minister Sheikh Yamani: “The Stone Age did not end for lack of stone, and the Oil Age will end long before the world runs out of oil.”

Photo by Cameron Casey from Pexels