The Opportunity Zone (OZ) program was created as part of the Tax Cuts and Jobs Act of 2017 (TCJA) to help spur investment in low-income communities. Eligible investments made within an OZ can reduce or even eliminate the taxes owed on capital gains if they are held in a qualified OZ fund for a sufficient amount of time. But whether a particular tract can be selected as an OZ crucially depends on it first being designated as a Low-Income Community (LIC) by the Treasury Department—a process which appears to have been corrupted.

A recent investigation by ProPublica reveals a case in which a wealthy area of Detroit was designated as an LIC despite not meeting any of the eligibility criteria. Uncovered documents point to a lobbying effort by the billionaire founder of Quicken Loans, Dan Gilbert, who (not coincidentally) owns a significant amount of property in the area. The mis-designation potentially allows Gilbert to capture enormous tax advantages intended by Congress to support struggling regions, not a wealthy CEO.

Unfortunately, ProPublica’s finding is not the end of the story. According to an original analysis by the Niskanen Center, similar misclassifications appear to have occurred in at least 2 additional census tracts.

Not-So-Low Income Communities

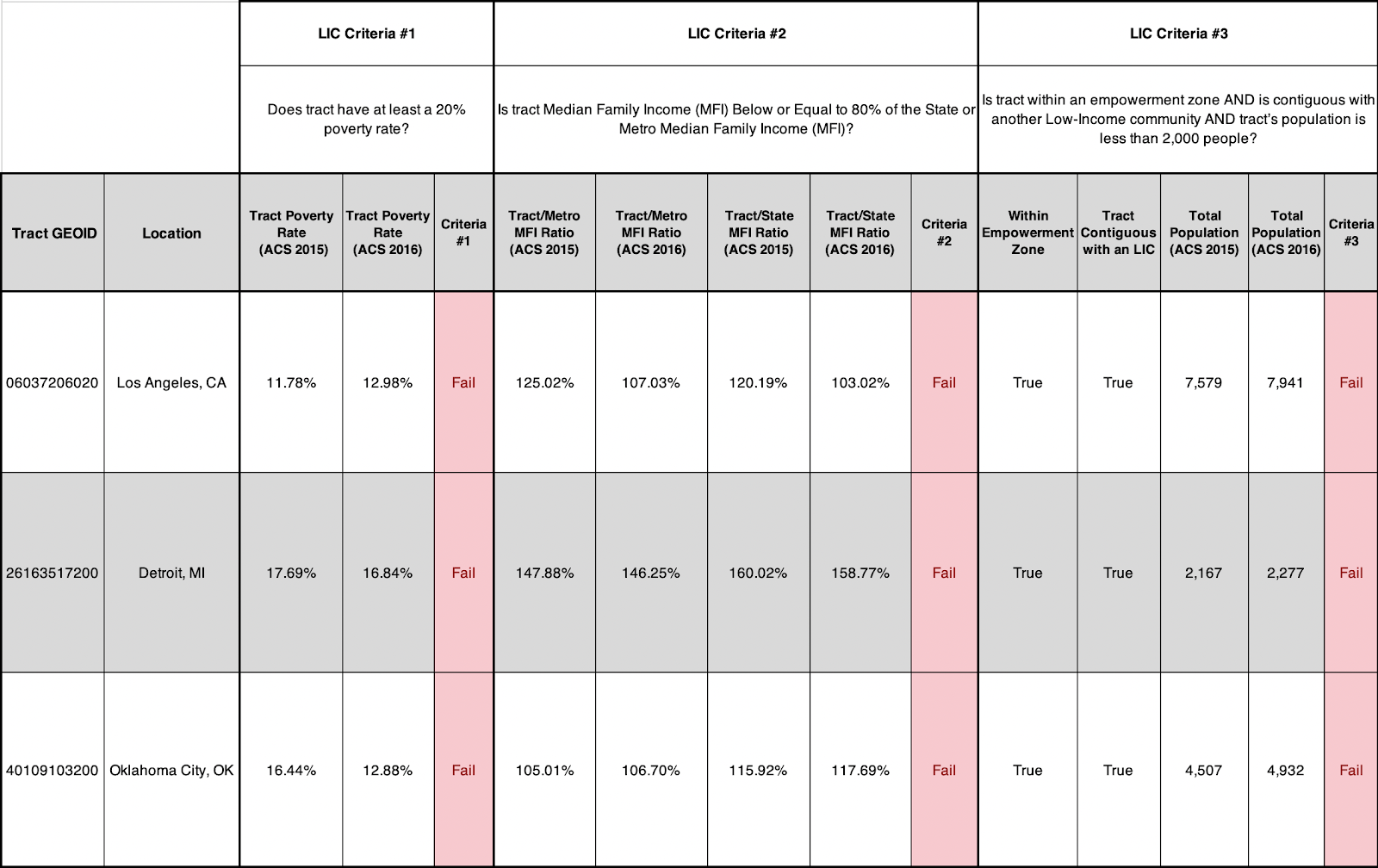

Apart from the improperly classified LIC tract in Detroit (tract ID 26163517200), misclassifications also appear to have occurred in Los Angeles, CA (06037206020) and Oklahoma City, OK (40109103200). Furthermore, these misclassifications were instrumental to the improper designation of two additional OZs through the Contiguous Tract Criteria (tracts 26163517000 & 06037206031 respectively). In total, five OZ tracts were misclassified. While two of these can retain their OZ status under a reclassification as contiguous tracts with legitimate LICs, the other three OZs are entirely improper—that is, they should not have qualified under the requirements stipulated by the TCJA.

All three of the improperly labeled LIC tracts do not meet the income or poverty requirements to be designated a LIC, but are situated in Empowerment Zones or contiguous with other LICs, which are sub-criteria for another eligibility avenue. However, all three ultimately do not qualify as LICs as a result of having a population of over 2,000 persons in both the 2015 and 2016 editions of the American Community Survey (the two years of data admissible for the Low Income Community criteria).

Below is a table demonstrating the lack of eligibility for the aforementioned tracts under Section 45D(e) of the Internal Revenue Code. The eligibility criteria regarding rural tracts, areas not within census tracts, and targeted populations (typically Native American tribes) aren’t explored in detail in this table. Yet as far as can be discerned, the improper tracts would not meet these criteria either.

In addition to the improper LIC classification of these tracts, two of these misclassifications resulted in further improper OZ designations by creating branches through which the contiguous tract criteria were applied. In what follows, I walk through the details behind each of the apparent misclassifications, and consider whether they should retain their OZ designations.

Detroit:

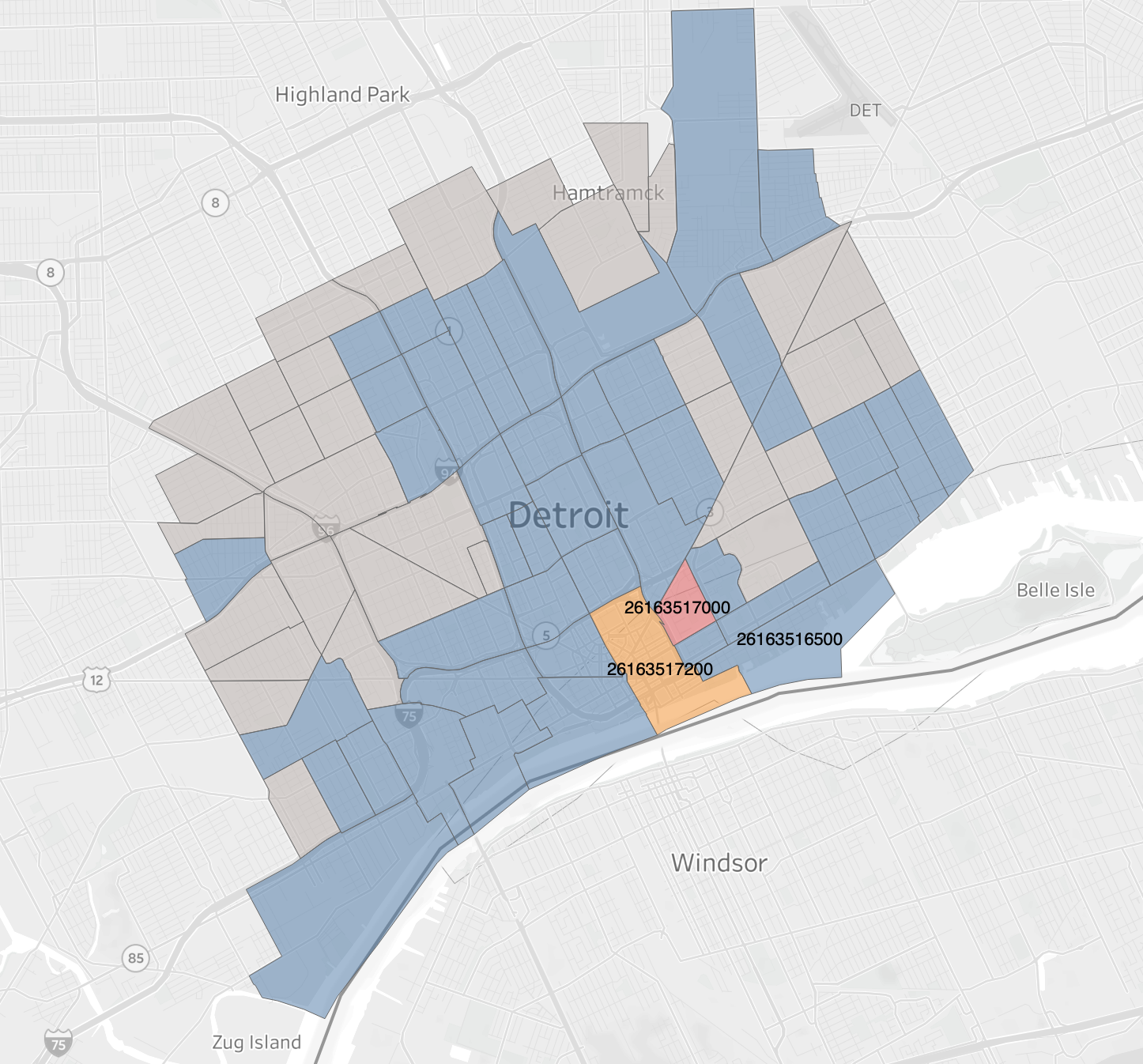

Tracts 26163517200 & 26163517000

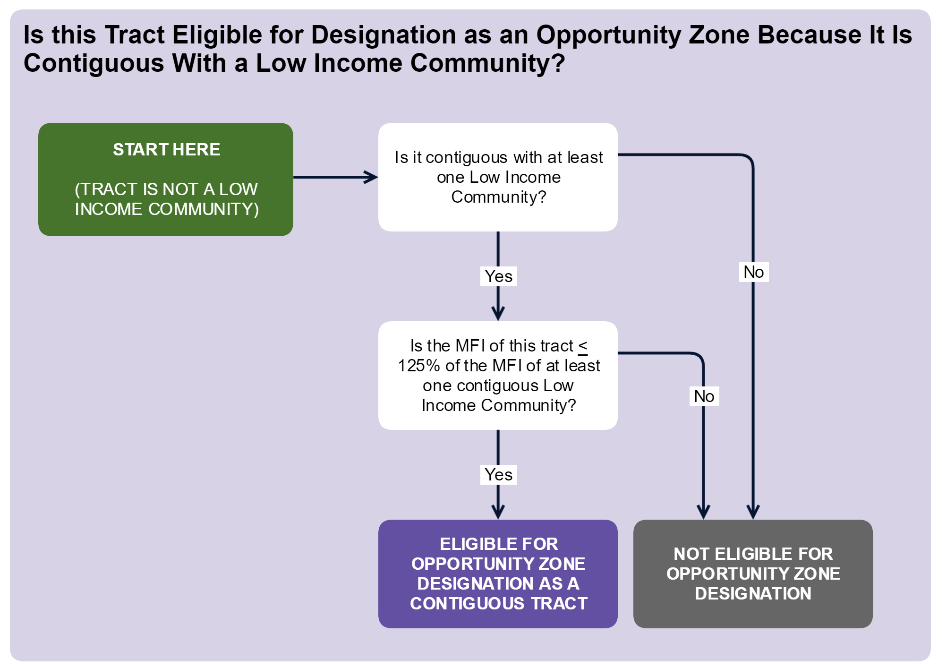

As the ProPublica report points out, tract 26163517200 does not meet the eligibility criteria for OZ designation through the LIC criteria. What the article doesn’t mention is that this tract was requisite for the designation of another OZ through the Contiguous Tract criteria. Under this criteria, any tract contiguous with a LIC and with a median income no greater than 125 percent of the LIC tract can also be designated as an OZ.

According to the 2015 American Community Survey, which is the only year relevant for Contiguous Tract designations, the improperly designated tract in Detroit had a median family income of $99,609. This allowed the contiguous tract 26163517000, with a median family income of $60,957, to receive an LIC designation as well. Its median income would have been too high to qualify based on any of its other LIC neighbors.

Strangely, however, another neighboring low-population LIC tract (26163516500) recorded a median family income of $82,917. This means that the improperly designated LIC Detroit tract could have been eligible as an OZ under the contiguous tract criteria after all. Indeed, Michigan could have designated this tract as a contiguous tract while remaining under the 5 percent limit on contiguous tract designations. Consequently, despite being suspicious, only the branching contiguous tract 26163517000 was truly ineligible for its OZ status according to the statute.

Los Angeles:

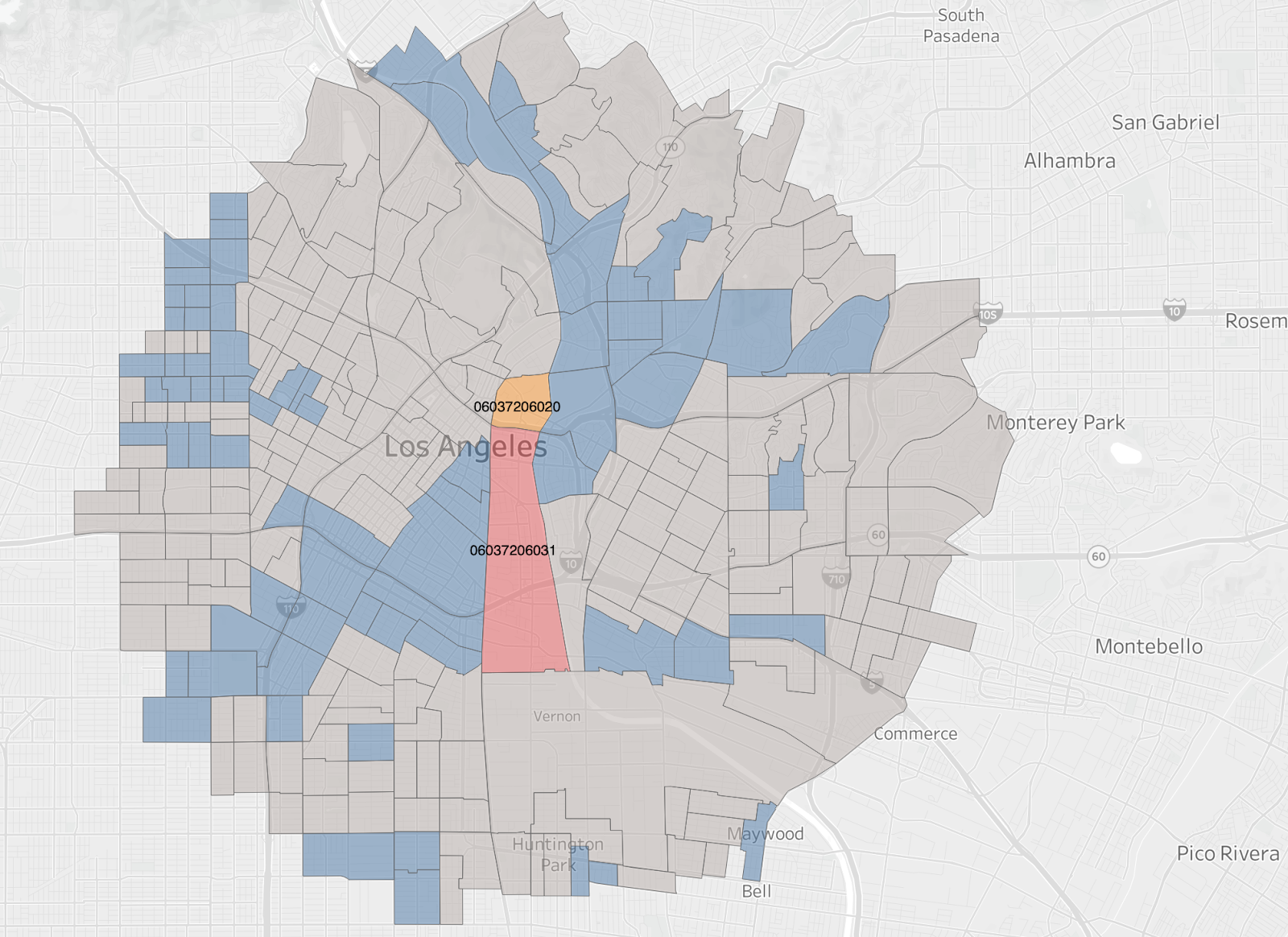

Tracts 06037206020 & 06037206031

A tract situated in Los Angeles, 06037206020, also appears to have also been improperly designated as a LIC. Much like in Detroit, this tract led to a secondary improper OZ by creating a bridge through the contiguous tract criteria.

Tract 06037206020 has a median family income of $85,000, which is just barely high enough for neighboring 06037206031 to qualify with a median family income of $103,750 — 122 percent of $85,000. Since other neighboring Low Income Community tracts have median family incomes roughly between $25,000 and $40,000, it would not have been possible for this tract to be designated through the contiguous tract criteria without branching off of 06037206020, which itself was improperly designated.

Covering most of Los Angeles’s affluent Arts district, this tract has no business being an Opportunity Zone, and there is no way to salvage the OZ status of either tract through alternative eligibility criteria. If Detroit’s improper designations were the result of lobbying, investigative journalists should consider looking into whether something similar occurred in Los Angeles.

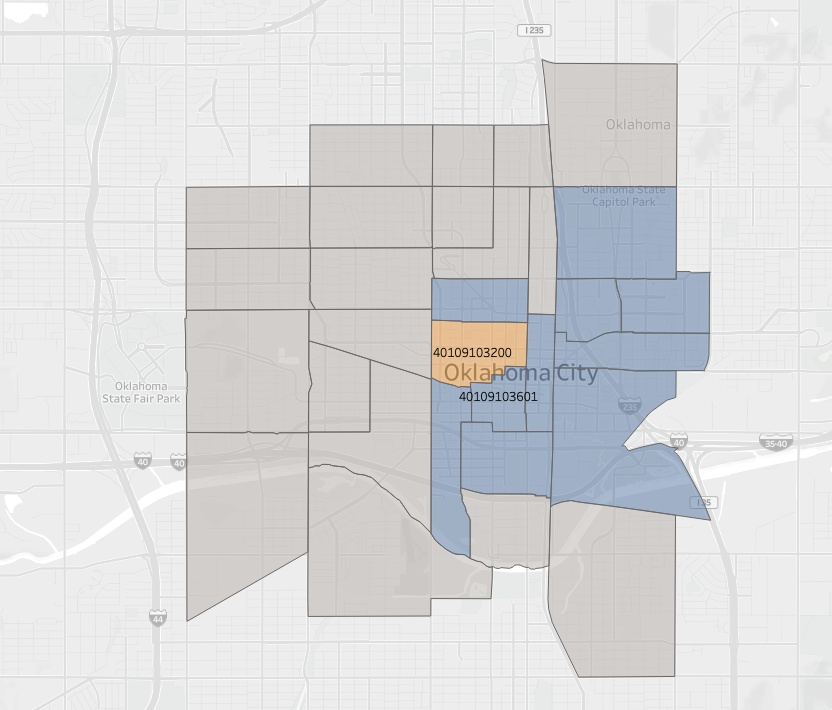

Oklahoma City:

Tract 40109103200

Finally, a census tract in Oklahoma City was mislabeled as a LIC, but in a way that appears to be inconsequential. Despite not being eligible as a LIC, the tract could have been designated as an OZ through the Contiguous Tract criteria given that tract 40109103200 meets the income requirements via neighboring LIC tract 40109103601, and Oklahoma did not hit its limit on tracts designated through the contiguous method. If this improper designation is evidence of a scandal, it is an incompetent one. Under the TCJA, the tract could have achieved OZ status through a legitimate application of Contiguous Tract criteria.

Conclusion

ProPublica’s investigation into the improperly designated Low-Income Community tract in Detroit opened the possibility that more tracts were erroneously designated in a similar manner. My own investigation indicates that this is indeed the case for two additional tracts located in Los Angeles and Oklahoma City. While the mislabeling of the tract in Oklahoma City is of little consequence, the improperly designated LICs both in Los Angeles and Detroit have far more serious ramifications. The tracts in Los Angeles and Detroit each enabled additional improper designations to occur thanks to the Contiguous Tract criteria. While the improperly labeled Detroit tract could have itself been designated through the contiguous tract criteria, the branching contiguous tract it created is illegitimate.

If a legitimate rationale for the apparent misclassifications is not uncovered, the following census tracts should have their Opportunity Zone status rescinded under current law:

- 06037206020

- 06037206031

- 26163517000

Ensuring that the benefits of Opportunity Zones flow to struggling regions as intended will be essential to preserving the legislation’s integrity.

Update: You can find the follow-up to this analysis here.

This research is part of the Niskanen Center’s Struggling Regions Initiative.