My colleague Will Wilkinson wonders whether the Federal Reserve under Gary Cohn will be willing to run the economy hot.

Fun question: would a Gary Cohn/Goldman Fed agree to run hot? @karlbykarlsmith

— Will Wilkinson ? (@willwilkinson) July 16, 2017

Cohn is currently Trump’s Chief Economic Advisor and Director of the National Economic Council. Trump is rumored to favor Cohn as a replacement for Federal Reserve Chairperson Janet Yellen, whose term is up in 2018. Traditionally, the Federal Reserve’s Open Market Committee, which is responsible for setting interest rates, has deferred heavily to the Fed. Chairman Alan Greenspan had nearly dictatorial powers over the Committee. That softened under his successor Ben Bernanke. Nonetheless, the committee members rarely voted against the Chair, and Bernanke was never overruled.

Bernanke’s successor, current Chairwoman Janet Yellen, continued his policy of seeking wide input from the committee. However, she also has rarely been voted against and never overruled. Thus, her successor can be presumed to carry a lot of power. So the question is: should Cohn become Chairman, what kind of Fed can we expect?

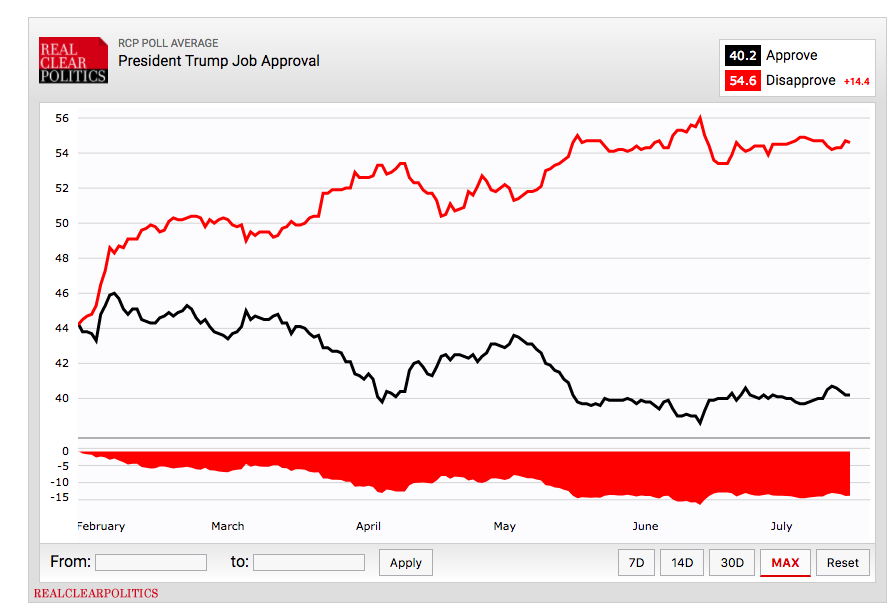

Arguably the most prominent factor in this determination is that the President’s approval ratings are deeply underwater. According to Real Clear Politics, the President’s disapproval rating is 14 percentage points higher than his approval rating.

Yet the economy is running well. Unemployment is low. Job creation is high. The stock market is near record highs. Typically, we’d expect a President to have numbers the inverse of Trump’s. If the economy tanks we could see Trump’s approval drop into the 20s, around the level of George W. Bush late in his second term.

So far, Trump has had a solid 40 percentage point floor, despite his array of outrageous scandals and seemingly incompetent administration. One might think he is impervious even to horrible economic news. I doubt it. I strongly suspect that a healthy fraction of the folks who are still with Trump are with him because they perceive him as someone who can deliver results, despite his bad behavior. The strong economy, which Trump came into office with, only helps support that view. If the economy goes, however, so does the fundamental justification for putting up with Trump.

This all puts Cohn in a difficult position. On the one hand, both he and Trump have berated the Fed for having too loose of policy. That is, they have accused the Fed of keeping interest rates too low, which has the positive effect of increasing economic activity and driving down employment, but risks rising inflation and potentially fueling asset price bubbles.

The Federal Reserve is supposed to be independent of politics, and the Chair is expected to steer the committee without concern for the political fallout of his actions. That means that Cohn, if appointed as Chairman, should stick to his guns and raise interest rates to rein in inflation and the risk of asset price bubbles. Yet nothing about Trump or his administration suggests that he will adhere to these norms.

If appointed, I fully expect Cohn to reverse himself and push to keep interest rates low in an effort to keep his former boss in power. The big question mark is whether or not the rest of the Open Market Committee will fall in line. The Fed has not been tested this way since the 1970s when Fed Chairman Arthur Burns was accused of driving down interest rates to keep Nixon in power. Privately, the Open Market Committee was livid, but they trudged along with Burns, and the result was stagflation. My sense is that the groundwork laid by Bernanke and Yellen is extensive, and that today the committee would feel empowered to fight back against brazen politicization by the Chair. Still, it’s a test we should all hope the Fed is not forced to face.

{kind=link}