“We have no long-run budget policy—no policy for the size of deficits and for the rate of growth of the public debt over a period of years. Annually we make decisions about the size of the deficit that are entirely inconsistent with our professed long-run goals, with the explanation or hope that something will happen or be done before the long-run arises, but not yet.” (Herbert Stein, The AEI Economist, Dec. 1984).

That quote never goes stale. It was true when Stein wrote it nearly 40 years ago, and it remains true today. Once again, we are up against the debt ceiling. Are we going to let the crisis go to waste, yet again? Or will we use it as a spur to establish some real rules for budget policy, once and for all? And just what would a good set of fiscal rules look like?

How alarmed should we be?

Stein wrote about the hope that “something might be done before the long-run arises.” But, oops, the long run is suddenly a lot closer than it was then.

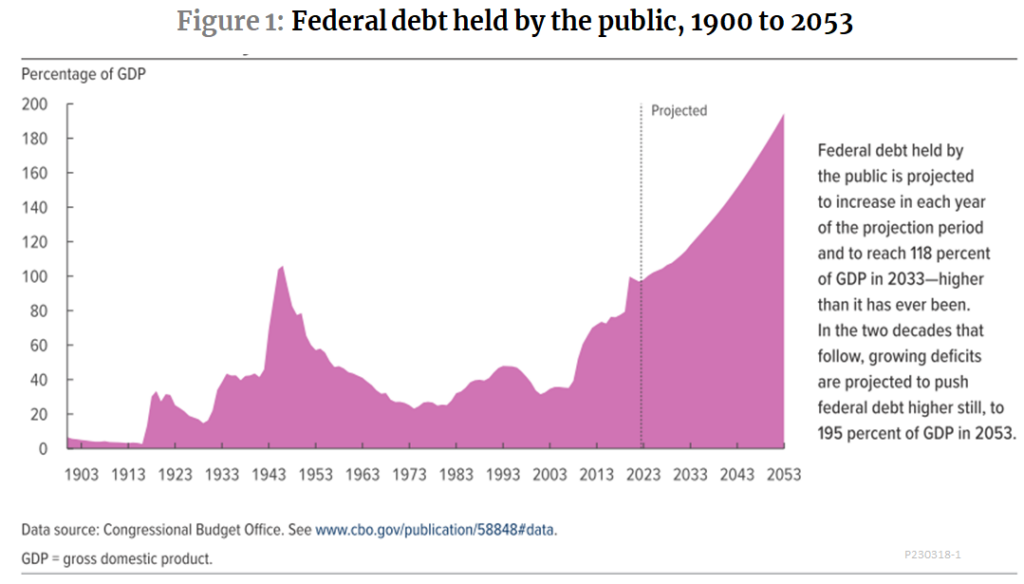

Consider the following chart from the latest Congressional Budget Office Budget and Economic Outlook – one that almost everyone will have seen by now. In Stein’s day, and for quite a few years after that, debt was 35 percent of GDP, plus or minus a bit. But since the 2008 financial crisis, the debt ratio has tripled. The CBO estimates that it will reach 98 percent of GDP in 2023 and go nowhere but up after that.

A quick tour of the enormous literature on the relationship between government debt and the health of the economy suggests that we should be concerned, but not panicked, by the CBO’s numbers.

Pessimists, like Veronique de Rugy and Jack Salmon, authors of a survey published by the Mercatus Center, don’t like what they see in the chart. They warn of threshold effects somewhere in the 70 to 100 percent range. Beyond the threshold, they say, higher debt slows growth due to higher interest rates, distortionary taxes, inflation, and constraints on countercyclical policy.

However, other research, and other interpretations of some of the same sources that de Rugy and Salmon cite, are less alarmist. For example, a 2014 International Monetary Fund study agreed that short-run data suggest a threshold effect around 90 percent of GDP. However, the threshold disappears when longer-term data are used. “There appears to be no clear point above which a nation’s debt dramatically compromises medium-term growth,” concludes that study.

Theoretical analysis helps explain why clear tipping points are hard to find, and why, when they are found, they are found at widely different debt ratios. Olivier Blanchard’s 2019 presidential address to the American Economics Association has been especially influential. Blanchard meticulously examined the underpinnings of supposed thresholds, such as interest rate effects, distortionary taxes, and intergenerational transfers. Although careful not to argue directly for higher debt levels, he concluded that “both the fiscal and welfare costs of debt may then be small, smaller than is generally taken as given in current policy discussions.”

One of the main factors driving Blanchard’s conclusions is that interest rates on government debt have been lower than rates of economic growth in most advanced economies in recent decades. In yet another study, Jason Furman and Lawrence Summers argue that low interest rates are likely to last. As long as they do, the whole idea of using the ratio of debt to GDP as a metric of fiscal policy will be in doubt. The problem is that the debt ratio compares the stock of debt to the flow of GDP. Instead, Furman and Summers say, we should look at stock-to-stock or flow-to-flow comparisons.

A stock-to-stock comparison would look at the current level of debt relative to the present value of future GDP. That is what a business firm would do when comparing the borrowing needed to finance a new factory with the present value of added profits. In making such a calculation, the present value of receipts or outlays is less the farther in the future they occur and the higher the interest rate that is applied. It turns out that if the rate of GDP growth exceeds the interest rate, the discounted present value of future GDP is infinite. In that case, the stock-to-stock debt ratio is always zero.

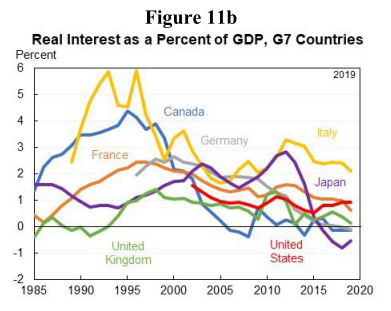

The disappearing stock-to-stock debt is, admittedly, something of a parlor trick. As a guide to policy, Furman and Summers put more emphasis on a flow-to-flow measure, the ratio of real interest payments to real GDP. That is similar to the calculation a potential homebuyer makes when comparing their mortgage payments to their income. Furman and Summers find that the real burden of interest payments is falling in the United States and other wealthy countries. Here is the relevant chart from their paper:

And one more point, made both by Blanchard and by Furman and Summers. The interest on debt is reasonably seen as a net burden when the government borrows to finance current consumption. However, if the borrowing goes to finance public investment, and if the rate of return on public investment is higher than the interest rate on public debt, then borrowing produces net benefits. That is why balanced budget rules at the state level typically apply only to current expenditures and allow borrowing for capital projects.

All these arguments make government borrowing look a lot less scary, but do they overstate the case? Some debt alarmists may not be aware of the relevant research, and others may ignore it as politically inconvenient. But there are still other economists who have read and understood the work of Blanchard, Furman, Summers, and others, yet still harbor serious reservations about high and rising debt ratios.

A short blog post by John H. Cochrane, formerly a professor at the University of Chicago and now a fellow at the Hoover Institution, provides a good summary of the case against what he calls “debt denialism.” His argument invokes the precautionary principle: Even though California hasn’t had a catastrophic earthquake recently, it still rests on a fault. It needs to be ready.

The economic equivalent is that the low interest rates of recent years do not mean rates will always be low. A war with China, another, bigger, banking crisis, or a virus as contagious as Covid and as deadly as Ebola could raise both government expenditures and interest rates in a hurry. It is only prudent to have enough unused borrowing space in reserve to allow a surge in government spending. It is also important to manage the term-structure of debt carefully. Cochrane would be more comfortable if the Treasury did more long-term borrowing to lock in low interest rates. (Determining the term-structure of the debt is complicated, but the weighted average term currently seems to be about five years.)

Besides, says Cochrane, the arguments of Blanchard, Furman, Summers and others do not endorse ever-increasing deficits or limitlessly rising debt ratios. At most, they only establish that a high but stable debt ratio can be sustainable if well managed. A permanent deficit that is a percent or two of GDP is one thing; a debt that edges up year-in and year-out, or a budget that misclassifies current spending as capital investment, is something else again.

The bottom line? Serious economists are not arguing about whether debt is good or bad per se. They are seeking fiscal rules that can hold debt and deficits within reasonable limits. What would such rules look like?

What kind of fiscal rules?

The basic elements from which sound fiscal rules could be built are surprisingly simple and not especially controversial. A good set of rules would consist of four elements: A policy goal, an operating target, an error-correcting mechanism, and a fiscal council. Many governments around the world – Switzerland, Sweden, Chile and more – have had success with rules of that kind.

The policy goal

The first element is a policy goal. In the broadest sense, the goal is sustainability. Despite the limitations of the stock-to-flow debt ratio, most economists would agree that growth of the debt ratio to a point where investors became unwilling to lend to the Treasury at reasonable rates would be unsustainable. That being the case, it could make sense to set a goal of holding the debt ratio within a specified band, with multiyear averaging to allow for cyclical ups and downs.

The operating target

The second element of a fiscal policy rule is an operating target. The operating target needs to be a variable that is within the power of policymakers to control on an annual basis. The debt ratio itself will not do as an operating target. From year to year, it is subject to variations that are beyond the control of policy. Any effort to achieve a target debt ratio that differs much from the initial value would inevitably take many years. The balance of the federal budget – its surplus if revenue exceeds expenditures or deficit if expenditures exceed revenues – is a more reasonable target.

The budget balance itself can be defined in several ways. Some of those are more suitable as an operating target than others. The worst possible target would be to aim for an overall zero balance every year. Annual balance requirements have been proposed in Congress many times, as simple laws or as constitutional amendments. However, an annual balance rule would be highly destabilizing. As explained in this earlier commentary, any such rule would require procyclical spending cuts during recessions while removing fiscal discipline during booms. Fortunately, this time around, we haven’t heard much talk of such a scheme.

A better idea would be to target the structural balance, also known as the cyclically adjusted balance, or, in CBO terminology, the balance without automatic stabilizers. The structural balance is the estimated level of the surplus or deficit that would be observed if GDP were at its potential, the unemployment rate at what we commonly call “full employment,”, and all other factors unchanged (CBO, 2010). A structural balance target takes full advantage of automatic stabilizers – spending items like unemployment benefits that increase during recessions and revenue items like income taxes that increase when the economy expands.

To see how that would work, suppose spending and tax laws were set to in a way that would achieve a zero balance of the budget in years when GDP was at its potential level. Starting from there, if there were a downturn, revenue from income and sales taxes would fall while outlays for unemployment and food assistance would rise. The structural balance would remain on target while the current budget would slip into deficit, providing enough fiscal stimulus to moderate the downturn. Similarly, in a boom year, the current budget would move into surplus, moderating inflationary pressures, while the structural balance remained at zero. Over the course of the business cycle, the resulting surpluses and deficits would, at least roughly, cancel out.

A still better rule would target the structural primary balance (SPB). The SPB is the structural surplus or deficit with interest expenditures removed. An SPB target has two advantages. One is that interest expenditures are not under the immediate control of policymakers, being largely determined by past borrowing and by market interest rates. The other is that an operating target based on the SPB has close relationship to the policy goal of stabilizing the debt ratio. A target based on the current balance is not as closely related to the debt ratio, since the current balance changes from year to year due to variations in interest expenses and automatic stabilizers, neither of which is under the short-run control of policymakers.

Suppose, for example, that the structural primary budget remained indefinitely at a deficit of 2.9 percent of GDP, as the CBO expects for 2023. If economic growth and interest rates were also to stay at their expected 2023 levels, the steady-state debt ratio would eventually stabilize at about 140 percent of GDP. Narrowing the target SPB deficit to 2 percent of GDP would be enough to stabilize the debt ratio close to its actual 2023 value of 98 percent of GDP. Further narrowing it to 1 percent of GDP would stabilize the debt at a bit less than 50 percent of GDP. Setting the SPB target at zero would eventually eliminate the debt altogether.

The error-correction mechanism

By the nature of the budgeting process, planned levels for revenues and outlays have to be set in advance, on the basis of estimated conditions for the coming fiscal year. Obviously, in any given year, the actual outcomes for revenues and outlays are likely to be different from the estimates. If so, the actual amount of borrowing required in any fiscal year could be above or below the target.

To handle that possibility, well-functioning fiscal rules, such as the Swiss “debt brake,” include mandatory error-correction mechanisms. Unplanned excess borrowing in any given year has to be offset with higher taxes or lower spending in the future. Unexpected surpluses go into a “rainy day fund” of some sort that permits extra spending or tax cuts when needed. An error-correction rule that operates over a sufficiently long period, with allowances for emergency situations, can maintain debts and deficits close to their target values on average while still allowing for adequate countercyclical fiscal stimulus or restraint.

The fiscal council

Perhaps the trickiest part of establishing a workable set of fiscal policy rules is their enforcement. If enforcement is left solely to the executive or the legislature, it would be too easy to ignore the rules altogether for reasons of short-run politics. The definition of “emergency” would expand to take in ordinary spending. Current spending would be misclassified as investment. The data themselves on which budgeting was based would be fudged.

Accordingly, countries with successful budget rules have established fiscal councils to oversee the way rules are implemented. Ideally, a fiscal council is well insulated from short-run political pressures. The fiscal councils of specific countries are described in this OECD report.

In the United States, the Federal Open Market Committee, a part of the Federal Reserve, has the necessary combination of decision-making powers and political independence to function as a council for monetary policy. However, there is no comparable body for fiscal policy. The closest thing we have to a fiscal council is the Congressional Budget Office. The CBO does have a respectable degree of political independence in producing projections of economic trends and estimates of the effects of tax and spending measures. That helps, since those are essential inputs to fiscal policymaking. However, the CBO lacks the power to set targets or to undertake mandatory error correction. A fully successful transition to rule-based fiscal policy in the United States should either enhance the powers of the CBO or set up a new, politically independent fiscal council of some kind.

Structure vs. calibration

The preceding discussion emphasizes the upside of fiscal rules and the risks of the unchecked discretion of politicians. However, a fully rules-based system may seem unrealistic in a democracy, where the balance of political forces changes from election to election. It might even seem constitutionally questionable. After all, the Appropriations Clause in Article 1 gives Congress the power of the purse. Could majorities of the Senate and the House really hand that power over to an independent council?

My reply to those concerns is to make a distinction between setting the structure of rules and calibrating them. Rules need to have a sufficiently solid structure to maintain fiscal sustainability, but that does not require political rigidity. The needed flexibility comes from building parameters into the rules that can be calibrated to serve changing political visions as they emerge.

For example, the rules described here call for some mechanism to curb unrestrained growth of the debt, but they do not cast in stone any specific target for the debt ratio. That depends on subjective judgments about what is optimal or sustainable. Whether the goal should be stabilizing the debt at 100 percent of GDP, cutting it in half, or whatever else is inherently political. A similar issue arises with regard to the balance between spending and taxes. Ideally, a budget rule that targets the debt or deficit should be neutral with respect to the total size of government. Such a rule could be calibrated to allow generous expenditures supported by adequately high taxes, or instead, a government that is low on taxes and lean on benefits, if that is what the voters want.

Is there any hope?

Reading the headlines in the spring of 2023, it is hard to find much interest in fiscal rules, either in Congress or the White House. As the dreaded day of default approaches, the debate has largely focused on a “clean” increase in the debt ceiling that would return us to business as usual vs. sweeping cuts to specific spending programs. Still, if we look hard enough, we can find a few hopeful signs of interest in a more rules-based approach.

On the Democratic side, for example, Rep. Jared Golden (D-ME) has outlined his version of a budget deal in a lengthy letter to constituents. As a down payment, he proposes a long-term fiscal goal for Congress that would stabilize the debt-to-GDP ratio. His proposal would cut $500 billion from the deficit over two years. Although he doesn’t get into technicalities, that would be very close to the one-percentage-point reduction in the primary structural balance that would, as explained above, stabilize the debt ratio at something close to its current 98 percent. Any additional moves toward balance in the PSB in the future would further reduce the steady-state debt ratio. To start negotiations off, Golden lists a specific set of deficit-reduction measures that are balanced between spending cuts and revenue enhancements. As a whole, his proposals could easily represent a first step toward rule-based fiscal policy.

On the Republican side, we find the intriguing Responsible Budget Targets Act (RBTA) from Sen. Mike Braun (R-IN) and Rep. Tom Emmer (R-MN). The RBTA is conceptually similar to the Swiss debt brake. It includes a long-term goal of debt reduction, a rule constraining annual primary deficits, and an error-correction mechanism. On a technical level, the RBTA, as written, is perhaps more of sketch than a finished product. Its rules need further development to maintain symmetry in treatment of taxes and expenditures and to avoid procyclicality in the face of exogenous shocks to the economy. But those problems could be fixed by appropriate refinement of its language regarding emergencies, potential GDP, changes in tax laws, and so on.

Whereas Golden’s goal, at least initially, is simply to stabilize the debt at its current ratio, the RBTA, as written, aims for zero debt in the long run. Those goals bracket the current range of debt ratios in most OECD countries. (Japan, with its debt ratio over 200 percent, and Norway, with its massive national wealth fund, are outliers that few propose to emulate.) On the face of it, some political compromise should be possible that aims for a steady-state debt ratio between 100 percent and zero. Such a policy goal would allow the fiscal space to deal with emergencies that the United States now lacks. At the same time, it would take full advantage of the potential of growth-enhancing public investments that are possible in an economy where the cost of debt service is consistently lower than the rate of GDP growth.

Can the two sides get together? Let’s hope so. But I’m only an economist. My job is just to show what could be done with good sense and good will, not to predict what will actually happen.

* The formula for the steady-state debt is D* = SPB*/(R-G), where D*is the eventual steady-state debt ratio, SPB* is the structural primary balance target, and R and G are the assumed rates of interest and growth. If the targeted debt ratio is very far from the current one, it could take many years for the debt to approach its eventual steady-state value. For a full explanation, see Rules for Sustainable Fiscal Policy: Three Perspectives.