In a recent commentary, Kevin Corinth and Scott Winship of the American Enterprise Institute’s Center for Opportunity and Social Mobility raised concerns that the expanded Child Tax Credit (CTC) proposed in the Smith-Wyden tax package could result in a marriage penalty for some low-and middle-income families.

While eliminating marriage penalties is indeed a critical public policy goal, the marriage penalties Winship and Corinth identify can be traced to the Earned Income Tax Credit (EITC) and Supplemental Nutrition Assistance Program (SNAP)—not CTC. These marriage penalties should be removed, but blocking a CTC expansion won’t solve them.

Fix marriage penalties at the source, not indirectly through the CTC

To determine whether it imposes any marriage penalties now or under the proposed changes, it’s necessary to look at the CTC in isolation. When Congress passed the Tax Cuts and Jobs Act of 2017, it addressed existing marriage penalties by raising the phaseout thresholds from $75,000 to $200,000 for single parents and $120,000 to $400,000 for married parents. The Smith-Wyden proposal would leave these CTC phaseout thresholds unchanged.

When we look at the impact of the proposed changes to the CTC’s phase-in, we find that it actually reduces a small marriage penalty for single parents with one child under current law (See figure 1). By increasing the refundable portion of the CTC, the proposed changes reduce the impact of filing status on the nonrefundable portion of the credit, which penalizes married couples filing jointly relative to single parents filing as head of household in some cases.

FIGURE 1

So how do Corinth and Winship find a marriage penalty when they examine the CTC in concert with the EITC, SNAP, payroll tax, and income tax? Although the CTC is usually marriage neutral or even offers a marriage bonus, that bonus doesn’t always align with the steepest marriage penalties imposed by the EITC and SNAP.

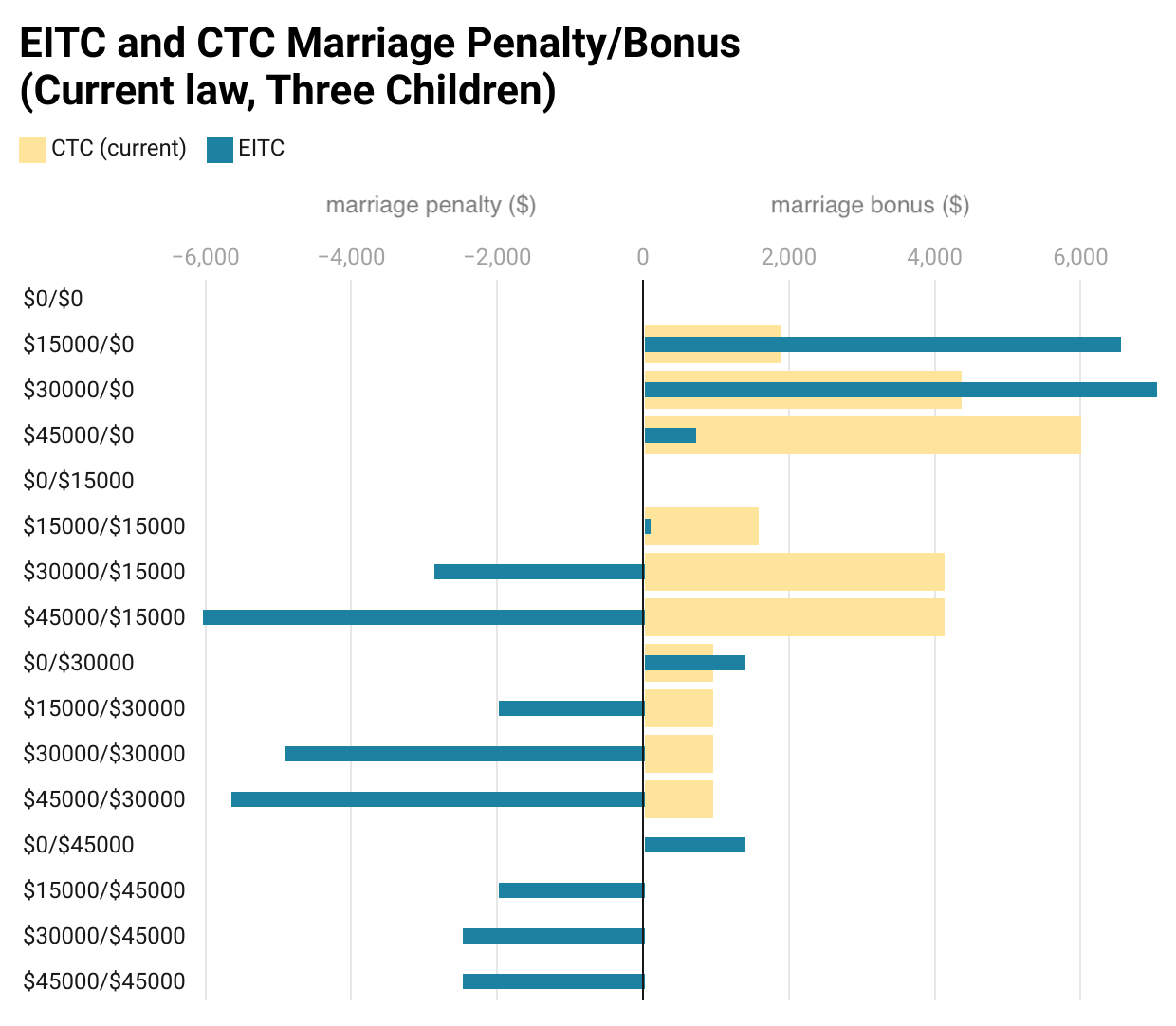

Smith-Wyden allows families with more children to phase in their CTC credits faster—a family with three children no longer needs to earn almost three times as much as a family with one child to receive their full credit. Lower-income families with more than one child see a larger marriage bonus. The marriage penalty that Corinth and Winship identify only emerges due to the interaction of the CTC with existing marriage penalties in the EITC and SNAP. Figure 2 breaks down the marriage penalties/bonuses by CTC and EITC for those hypothetical families.

FIGURE 2

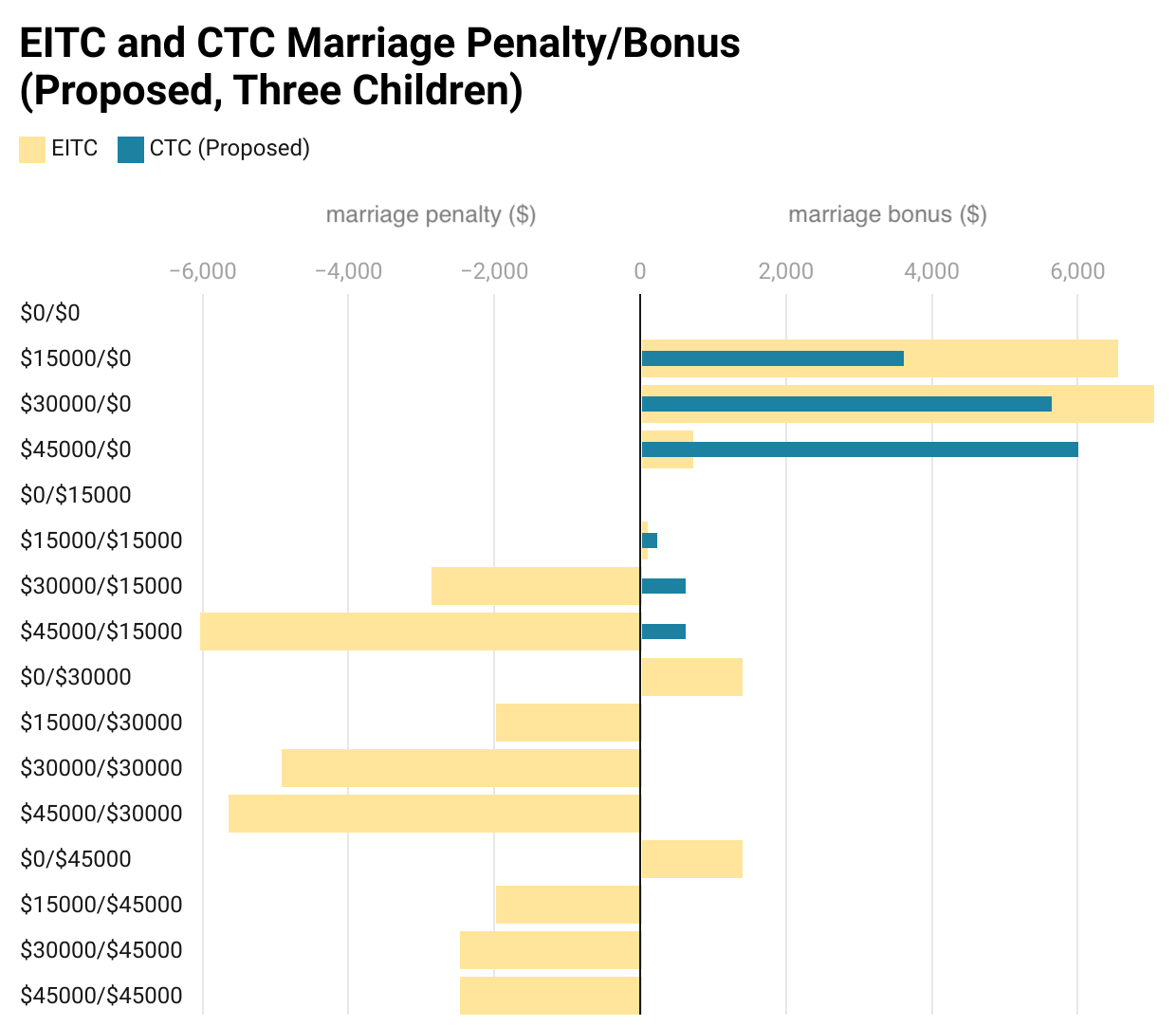

Figure 3 similarly breaks down the marriage penalties/bonuses by CTC and EITC for the same hypothetical families under the Smith-Wyden proposal. By phasing the credit in faster for larger families, the Smith-Wyden changes boost marriage bonuses for lower-income parents but decrease them for parents in the EITC phaseout range, exposing families to the full extent of the EITC’s marriage penalties.

FIGURE 3

We see these identical issues with SNAP. The EITC and SNAP marriage penalties are well-known, so they should be solved at the source. Corinth and Winship are essentially arguing that the CTC cannot undergo any reform that isn’t tailored to the bad design of the existing EITC and SNAP marriage penalties.

When we look at the specific CTC changes on their own, we find the Smith-Wyden proposal supports family formation. The structure of the CTC itself does not impose any marriage or work penalties, and for many low-income working families, it even offers a marriage bonus. Sound policy shouldn’t be penalized for failing to solve unrelated marriage penalties elsewhere in the tax-transfer system.