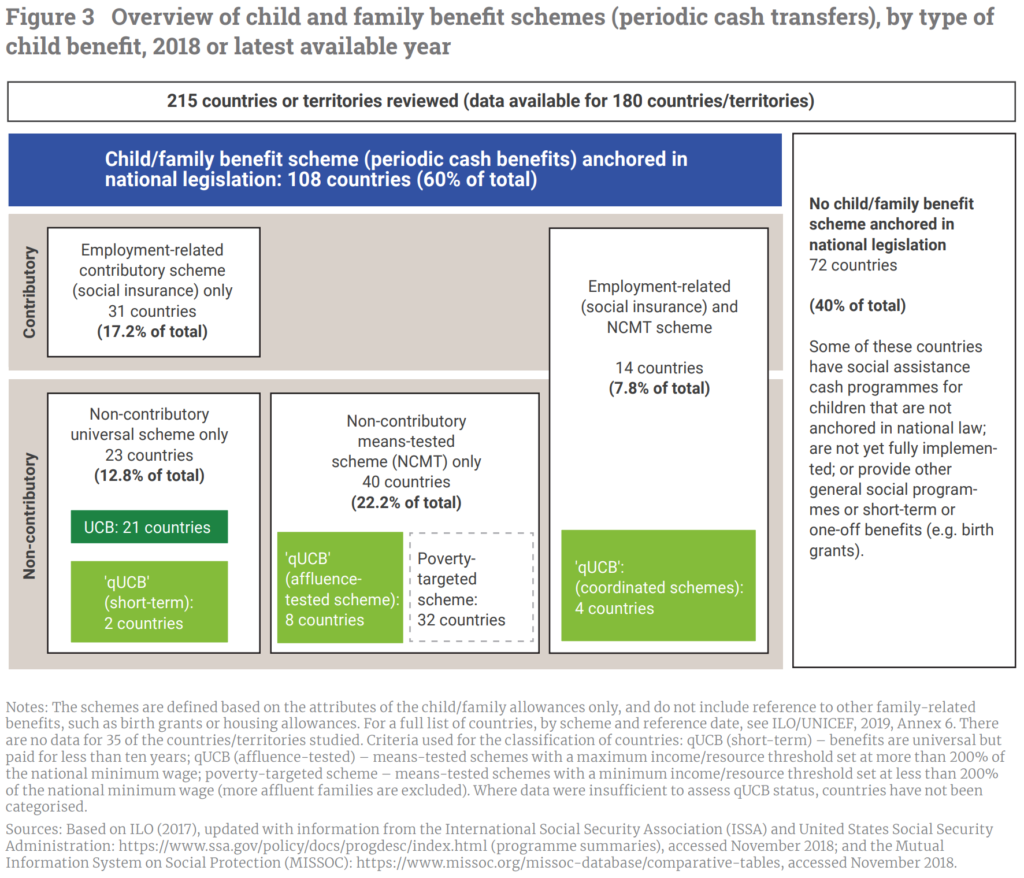

The IRS is one of the most efficient tax administrations in the world and is extremely cost effective at processing tax revenues, boasting one of the lowest costs-to-tax collection ratios. However, as a benefit service the IRS is underprepared to take on the growing social welfare responsibilities that are being delegated to it. As of 2018, the United States spent less than 30 percent of the OECD average for investing in family benefits. As it seeks to catch up to other countries through the recently expanded Child Tax Credit, there is much to learn from how other countries administer similar benefits. While there are numerous countries with child benefits, Canada, the United Kingdom, and Australia provide the best comparison points for the US to draw from toward developing a modern tax-and-transfer service within the IRS.

Social welfare policy isn’t just about deciding how much to give people and in what form. It is also vital to understand the design choices that governments have to make at the level of program administration. A 2020 report published by UNICEF and the Overseas Development Institute (UNICEF-ODI) identified several key factors for ensuring that recipients actually receive the child benefits they are eligible for. These include various elements of policy design such as the universality of the program, and the method by which benefits are transferred. However, when focusing on how to improve the Child Tax Credit’s administration as it is currently designed, administrative simplicity and ease of compliance are crucial for ensuring that the IRS can effectively administer this otherwise transformative child benefit program, and with the foundation necessary to sustain it into the future.

The Family Tax Benefit of Services Australia

Australia used to have child cash benefits delivered outside their tax system, but since 2000 have successfully administered the current Family Tax Benefit that replaced it. To administer the benefit well, Services Australia introduced the capabilities to account for changes in child living arrangements over the course of a year, establish standards for determining who should receive payments, and manage any improper payments at the end of each tax year. They have implemented all of this while making biweekly payments and maintaining administrative simplicity for beneficiaries of the program. [Correction: Australia moved their Family Tax Benefit from the Taxation Office to Services Australia to address administrative issues related to overpayments. While most applicants are still required to lodge a tax return to claim benefits, the move allows for many individuals to become eligible automatically, like those claiming unemployment benefits.]

For tracking mid-year changes in children’s household statuses, Services Australia makes individuals responsible for reporting changes when they happen. Their online portal includes features for adults to update custody arrangements of either a new child or changes to a previously claimed child. Beneficiaries are able to include the share of time in a year that they cared for a child they claimed, which is often important information for children under shared custody arrangements. By reporting the percent of time that the child lives with that parent, they are able to calculate how much of the benefit (and other family-related benefits) that the parent might receive. For instance, if each parent cares for the child 35–65% of the time, they can split the benefit. However, if one parent cares for the child for almost all the time, they receive all of the benefit. These changes in custody can be filed at any point in the year, which help avert any underpayments or overpayments that could be owed following recalculations with each financial year. To accommodate for periods of disputed care, interim periods were established for allocating benefits based on written agreements between caretakers, followed by a transition to allocating benefits based on the actual amount of care each person provides.

This design can be especially useful for the IRS in administering the expanded CTC so that it reaches the proper households throughout the year. While a tax credit is typically filed for and paid to households once annually, enabling families to begin receiving payments or change their status mid-year would help the IRS begin delivering benefits shortly after a child’s delivery. During the year, any new parent or someone who gains custody of a child could apply for the CTC, and be paid any potential remainder of the total annual amount they would be eligible for based on their tax return for that year. This would essentially represent a continuation of how the policy will function this year, with monthly payments from July until December with the remaining balance then paid on people’s 2021 tax returns. While policy changes might be needed to address surprise overpayments at the end of the tax year, this feature of accounting for any imbalance in payments can help simplify administering the program as it’s designed now. Easing the administrative complexity of the program for the IRS as well as the recipient is essential, as refundable tax credits to households with children are otherwise calculated as annual sums even if a child began living with someone mid-year.

The Canada Revenue Agency as a Role Model

Serving as a good model for a country’s benefit administration, the Canada Revenue Agency (CRA) accepts the dual roles of both revenue collection and welfare distribution for the nation. Through its Assessment, Benefit, and Service Branch, it administers the Canada Child Benefit (CCB) program that reaches 90 percent of families. While not designed through the tax code as the US’ child benefit is, there are still ways the CRA can provide a blueprint for improving the IRS’s administration of the expanded Child Tax Credit.

Like the IRS, the CRA still assesses families’ payments for their child benefit based on their tax returns. Tax returns are required to be submitted annually for a parent to keep receiving the CCB, although in Canada a family can get payments for prior years if they file tax returns for those past years. However, the CRA has decoupled filing for the CCB from how the agency determines the total benefits a family will receive. Filing a tax return is only needed to start receiving the benefit if the CRA hasn’t received one yet for that year. As the CRA notes on their website, someone can apply for the benefit immediately after a child’s birth, following a change in a child’s living or custody arrangements, or whenever they become eligible for receiving the benefit.

This ease of access for beneficiaries of the CCB can be applied to the US’s child benefit as well. While the IRS will be launching its own portal for people to apply for CTC outside the normal tax return process, it is important that the agency not add on additional burdens for applicants such requiring duplicate verification for income or household status. The IRS will often already have sufficient information through recent tax returns, such as claimed dependents with the Earned Income Tax Credit or the Child and Dependent Care Credit, to identify potential households that qualify for the child tax credit but haven’t applied for it. Using this information to reduce the barriers for CTC applicants would increase its take-up rate and make it easier for the IRS to process applications and benefit adjustments with limited resources.

A 2019 OECD report on nations’ tax administrations also detailed innovative initiatives that Canada’s agency has executed for reaching more people to claim eligible tax benefits. In 2017, the CRA ran a behavioral experiment to test any increase in take-up rate from including informational inserts on benefits in people’s paper tax returns. Among the group that received the insert, the number of paper-filed claimed for the Working Income Tax Benefit increased by 35 percent compared to their control group; they have since scaled this program up nationally. The CRA has also begun using business intelligence data and analytics to identify people who haven’t generally filed income taxes but might be eligible to receive benefits.

These outreach efforts can also be applied to the IRS’s administration of the child benefit. The Biden administration has already initiated outreach efforts for stimulus payments, but this could be expanded and established as a permanent force within the IRS to work with tax advocates and community groups to better reach non-filers. There is also potential for effective IRS outreach by working with state governments, given the data states’ have on beneficiaries of programs under their jurisdiction. Of the 12 million non-filers who were at risk of not receiving a stimulus check last year, 3.2 million were under the age of 17 and enrolled in Medicaid and SNAP. To reach more potential recipients, the IRS can collaborate with state administrations to target the households within this sizable group. Increased information sharing across agencies would enable the IRS to identify individuals to inform about the CTC and connect with community groups to establish more access points for people to apply for the benefit.

Comparing the CRA’s and IRS’s resources also demonstrates the funding deficit that the IRS has for processing regular child benefits, all the more demonstrating how important it is for the IRS to use its resources effectively. Despite the CRA having 40 percent fewer employees than the IRS as of 2019, they only had to serve 27.5 million tax filers compared to the 170 million returns the IRS processed in 2020. Since 2010, the CRA has added about 1,800 employees, while over this same period the IRS has cut over 22,000 positions. For their 2019 fiscal year, CRA appropriations for tax and benefit responsibilities was 13 percent greater (in US Dollars) than the IRS budget for taxpayer services. To note that these are corresponding areas within each administration, the taxpayer services section of the IRS budget “funds the infrastructure necessary for processing returns and refunds, as well as assistance and education for taxpayers as they prepare to file.” With the Canadian Revenue Agency’s sufficient funding, they have reported delivering 100 percent of monthly child benefit payments on time. With the well documented delays that the IRS had faced with distributing economic relief payments, it would be very helpful for Congress to sufficiently fund the IRS taxpayer services has the resources it needs to administer benefits like the CTC.

Lessons from Her Majesty’s Revenue and Customs

Across the Atlantic, the United Kingdom’s benefit administration illustrates some dos and don’ts which the IRS can adapt when implementing the expanded CTC. The UK’s Universal Child Benefit has a very high take-up rate at around 95 percent, while their means-tested Child Tax Credit (now being phased-out) has a take-up rate closer to only 80 percent each year. The UK’s two programs demonstrate the pitfalls the United States should avoid when implementing a means-tested child benefit. In particular, the universality of the UK’s Child Benefit has helped simplify its administration. As outlined in the UNICEF-UDI report, means-testing can lead to lower take-up rates because of an information gap for potential recipients who lack an understanding about eligibility rules or face obstacles to applying because of a more complicated filing process.

Even though the UK’s means-tested tax credit didn’t perform as well as their universal benefit, their experience reveals mechanisms that U.S. policymakers can learn from. For example, previous research on the UK’s Child Benefit found that their almost full take-up rate could be partly attributed to mothers receiving benefit registration forms at the hospital following the child’s birth. While there has been criticism of the UK benefit administration in the past given the complexity of the claims process and the lack of coordination between different government agencies, the HRMC was able to increase take-up rates by making the application process more accessible through an online portal, which the IRS already plans on implementing for the CTC this year. They also addressed often the neglected effects of form design by making the form language simpler and reducing the amount of information needed for verification. Community intermediaries, such as health providers or libraries, can also reduce the stigma around applying for benefits when they are available.

While the UK Child Benefit is universal rather than part of a means-tested tax-and-transfer system, the IRS can still borrow their administration mechanisms to develop a simpler administrative process that is easier for families to comply with. Learning from the UK’s failure at inter-agency coordination, the Social Security Administration (SSA) could establish a permanent Memorandum of Understanding with the IRS for reimbursements and information sharing.

There is also a lesson for the CTC to draw from child benefits in the UK, through how the UK links their Child Benefit application to birth registration. To do this, the SSA could work with the IRS to tie a CTC application to the SSA’s Enumeration at Birth process, which is when couples registering a child’s birth at a hospital apply for the child’s SSN. This would ease the burden on families when applying for the CTC by reducing the effort needed to claim the benefit and increase awareness of it. Ensuring cooperation might be a task for Congress, either through oversight or legislation; as recently as March 2021, they had to push the SSA into delivering the latest information of Social Security recipients to the IRS for the third round of stimulus checks. Additionally, the IRS could establish a more permanent mission to connect with local groups that have closer ties to communities to reduce stigma around claiming the benefit. As the UNICEF-ODI report detailed, stigma and lack of awareness on eligibility can reduce the take-up rate of benefits, which the UK addressed by partnering with trusted intermediaries.

A New Institutional Mission for the Internal Revenue Service

There are reasons for both optimism and concern about the IRS’s ability to distribute a child benefit. By sizing up the IRS’s current capabilities to other countries’ tax and benefit administrations, a well-administered CTC could slash child poverty by over a third. While there is some worry about the number of eligible families who are non-filers, both Canada and the United Kingdom show how this can overcome, achieving high take-up rates while still requiring recipients to directly apply for and report income levels in some capacity. However, this is still dependent on the IRS having the support to develop the additional filing tools and a well-designed application process for households to easily apply.

Moreover, there might be a need for broader reform of the IRS as an agency. As preeminent tax administration scholar Kristin Hickman describes it, “the IRS is now one of the government’s principal welfare agencies.” If the IRS is to increasingly take up the mantle of Internal Revenue and Benefit Service, there should be serious consideration of what changes as an institution and culture that requires. When the 1998 IRS Reform Act shifted the administration away from enforcing tax collection to “customer service,” it also led to the reshaping of the IRS’s bureaucratic organization itself. As Canada, the United Kingdom, and Australia all administer their child benefits through agencies designed with the mission of benefit administration, policymakers must consider the broader implications of advancing public benefits through the tax code for the IRS itself.

Samuel Hammond is the director of poverty and welfare policy at the Niskanen Center.

David Koggan is a poverty and welfare policy intern at the Niskanen Center and a rising senior at Carnegie Mellon University.