The unprecedented federal interventions and social-insurance expansions intended to protect households during the pandemic are almost all scheduled to be terminated by the end of this summer or fall. Although helpful, these policies formed a piecemeal, administratively complicated emergency safety net. Even if they are extended, it will likely be only at the last minute (as with the eviction moratorium and student loan freeze) or on a local or case-by-case basis only. Also, in many cases, the enrollment process for these programs is unnecessarily confusing and time-consuming. The people who need program resources the most are often the least able to acquire them, because they cannot afford the nonmonetary costs of navigating welfare bureaucracy. These costs create kludgeocracy, a word coined by Steve Teles of Niskanen to describe the complexities and incoherence common in government initiatives.

America lacks state capacity

The ability of the government to effectively provide a service is its state capacity, which often gets overlooked in the debate about the size or scope of government. As Sam Hammond wrote for the Niskanen Center, “At the most basic level … state capacity simply refers to a government’s ability to adopt a policy and have it faithfully enacted through some combination of competence, credibility, and political will.” Without that capacity, the government will not achieve the fundamental goal of social insurance, which is to give people the tools they need to achieve their own goals.

Creating an efficient social insurance program requires a system that capably redistributes, but does not over-regulate or impose high administrative burdens. The pandemic emergency assistance programs are a good case study for how social insurance programs are all too often rolled out, and they offer valuable lessons in how to do better.

Emergency housing assistance is failing

The web of emergency programs hurriedly propped up in the beginning of 2020 to save Americans from catastrophe, however well intentioned, amounted to a government bureaucracy that was extremely difficult for eligible Americans to navigate. This was especially the case for programs meant to assist families in their housing needs.

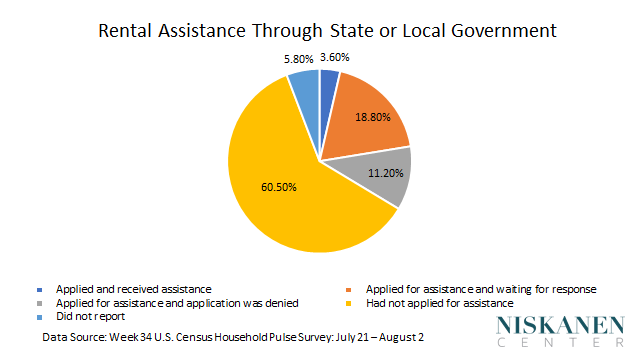

Renters must go through a time-consuming process to search and apply for federal pandemic rental assistance. Federal rental assistance programs are administered by state and local entities, each of which has different, complicated paperwork requirements. An application might require renters to submit bank statements, payroll stubs, and a letter from their landlord. Capturing this paperwork and uploading it for submission to a government website can be a long and fraught process. In fact, as David Dayen notes, “a fully funded Congressional program spent only 6 percent of its allocation in five months, leaving six million renters behind.” The most recent wave of the U.S. Census Bureau Household Pulse Survey found that around only 4 percent of households have received rental assistance, while around 19 percent have applied and have not yet received a reply. For renters who cannot make rent and aren’t covered by the eviction moratorium, there exists nonprofit legal assistance to fight evictions, but finding it and managing the eviction process also requires an exhaustive amount of time and effort.

The CDC just extended the moratorium on evictions in counties with substantial COVID transmission rates (which constitutes most of the country) to October 3, but this would not need to exist if federal rental assistance were effective. Renters would instead be able to make rent, and landlords would not be forced to shoulder the cost of missed rental payments. That alternative would be better because a moratorium has all sorts of negative downstream effects. It creates perverse incentives, where renters who can afford rent don’t pay because they won’t get evicted. It puts serious strain on small, individual landlords, the largest category of landlords, who do not have the savings to make their own payments for mortgages, taxes, maintenance, and other expenses. Public assistance for landlords is available, but it comes with many of the administrative burdens rental assistance does; landlords usually need personal information from tenants to apply for assistance and their tenants often refuse to supply that information. Many of these individual landlords may be forced to eventually sell their properties to corporate real estate firms, and some landlords are concerned about affording housing themselves.

A robust social insurance system means less regulation

It does not have to be this way. The Biden administration has had to extend the eviction moratorium — itself a politically fraught and legally dubious process — because of the lack of state capacity in our current system. The government has not been able to help renters and small landlords through cash transfers because we do not have the mechanisms in place to get money to the renters that need it.

If the government had invested more in social insurance programs earlier, the United States would not be in this position. Building information systems that allow us to quickly determine who needs assistance and how they can be reached would allow us to better manage situations like this going forward. For example, Vox’s Jerusalem Demsas has suggested that a rental registry would have forestalled the need for the eviction moratorium. A rental registry would simply be a federal database of rental units across the country, including the address, contact information for the landlord, and (potentially) current rent. If this information were already systematically collected by federal agencies, it would be much easier to determine which individuals need rental assistance and how much they need, instead of burdening applicants with paperwork and forcing them to become their own case workers.

How the Child Tax Credit addresses this kludge

The newly expanded and refundable Child Tax Credit provides an example of how a more robust framework for issuing payments can help. The system to administer CTC payments will assemble information on people’s bank accounts for disbursing checks in general. That also gives the IRS, which is currently distributing the CTC monthly payments, an opportunity to build out its ability to effectively administer public insurance. That would lay the groundwork for the government infrastructure necessary to handle future cash transfer programs, even if not through the vehicle of the IRS.

These CTC direct deposit payments should assist families who are concerned about housing interventions coming to an end, or who didn’t receive help because of bureaucratic hurdles. A report from the Cowen Washington Research Group notes that “the refundable child care tax credit may be a material offset to potential trouble for housing.” The U.S. Census Bureau Household Pulse Survey found that at least 7 million households are spending at least part of the CTC benefit on rent, and at least 5.7 million households are spending part of the CTC benefit on their mortgage payments. The CTC is also well-timed to help those who will be hurt by the rest of the pandemic safety net coming apart; enhanced unemployment insurance, the SNAP (or food stamp) expansion, and family leave provisions are coming to an end. The CTC is a major stimulus payment overall, not just within housing. Niskanen has recently estimated that its effects will “boost consumer spending by $27 billion, generate $1.9 billion in revenues from state and local sales taxes, and support the equivalent of over 500,000 full-time jobs at the median wage.”

The flexibility and no-frills approach of the CTC has come at the right time. It represents a better approach to government assistance that does not burden its recipients with unnecessary red tape. The pandemic safety net has made clear that overly regulated welfare programs hinder the government’s ability to achieve its goal of successfully helping people during a crisis. In order to build up state capacity, the government must also build up social insurance programs such as the CTC and government infrastructure such as a rental registry or the IRS benefit-distribution system. These would be substantive steps towards a future where those in need aren’t forced to navigate labyrinthian systems of welfare, and public assistance doesn’t present unnecessary barriers but helps all.

Matt Darling is the Employment Policy Fellow at the Niskanen Center.

Audrey Xu is a poverty and welfare policy intern at the Niskanen Center and a rising senior at Rutgers University.