Introduction

Economists generally agree that a well-designed carbon tax is an effective and promising way to reduce greenhouse gas (GHG) emissions that cause climate change, and U.S. policymakers and advocates have offered a number of carbon tax bills and proposals over the last few years.

An important component of a carbon tax is a border adjustment. A border adjustment would apply the carbon tax to the carbon content of imported goods and exclude exports from the carbon tax via a rebate. There is a consensus among most experts that border adjustments should be part of a carbon tax, but little agreement on how such a border adjustment should be designed. Legislators will need to consider a wide range of complex design issues. Developing a consensus about the goals of a border adjustment mechanism will help focus the design of border adjustments.

This paper reviews the principal design choices policymakers would face when establishing a border adjustment for a carbon tax, and the implications of different design choices. It also provides a high-level overview of carbon tax bills pending in the U.S. Congress.

Overview of a Border Adjustment

Border adjustments are widely used throughout the world in several taxes, most commonly value-added taxes (VATs). Although border adjustments apply a tax to imports and rebate tax on exports, they are, in principle, trade-neutral. As long as the export rebate and import tax are at equal rates to the domestic tax, the border adjustment does not encourage or discourage trade. A border-adjusted carbon tax would eliminate the incentive for companies to shift carbon-intensive production from a jurisdiction with a carbon tax to a jurisdiction without a carbon tax. In common parlance, a border adjustment protects the competitiveness of exporters seeking to sell in foreign markets and levels the playing field for domestic producers competing with foreign imports that otherwise face no carbon tax.

What is border adjustment?

A border adjustment is a mechanism that ensures that consumers of a good or service pay the same tax regardless of whether the good or service is imported or produced locally. A border adjustment works by applying a tax on imports and a rebate on exports. Imported goods are for domestic consumption, so they are taxed. Exported goods are for foreign consumption, so they are not taxed, hence receiving rebates.

Border adjustment is widely utilized throughout the world. The most common example of a border adjustment is that used in value-added taxes. A VAT, like a retail sales tax, is a tax on goods and services purchased by consumers. However, in contrast to a retail sales tax, it is paid in stages by producers along the production process. Each producer’s VAT liability is equal to their sales times the VAT rate minus any VAT previously paid on the inputs to production.

The VAT, used by all developed countries except the United States, is border-adjusted. As such, imports are taxed at the VAT rate as they enter a country and any VAT applied to a good that is ultimately exported is rebated to the exporter at the border.

Although the United States does not have a VAT, states and localities levy a similar consumption tax: retail sales taxes, which are implicitly border-adjusted. For example, goods produced in Maine are not subject to the state’s sales tax if they are purchased in Ohio. Instead, they are subject to Ohio’s sales tax. Likewise, goods produced in Ohio but consumed in Maine are exempted from Ohio’s sales tax, but face Maine’s sales tax.

A border adjustment for state-level tax and federal-level tax are equivalent concepts. Goods are taxed based on where they are consumed, rather than when they are produced. Additionally, the United States adjusts some excise taxes at the border, such as the cigarette tax and alcohol tax.

In principle, economywide border adjustments are trade-neutral. They neither encourage nor discourage imports or exports. The goal of border adjustments is to equalize the tax burden on imported goods and domestically produced goods, as they are both consumed within the same jurisdiction. Maine’s sales tax applies to imports, but exempts its own exports from sales taxation. However, this does not imply a trade advantage for Maine products. This is because a pair of shoes exported from Maine and sold in Ohio will face the same 5.75 percent sales tax as a pair of shoes manufactured and sold in Ohio.

Why is border adjustment important for a carbon tax?

The goal of a border adjustment under a carbon tax is similar to that of a border adjustment under a VAT. It is to ensure imported goods are subject to the tax and exported goods are exempted from the tax. Border adjustment under a carbon tax equalizes the tax burden on imported goods and domestically produced goods.

If the U.S. were to enact a carbon tax without a border adjustment mechanism, companies would have an incentive to shift their production overseas to countries with less stringent carbon pricing policies. Notwithstanding the economic impact, this would run counter to the goal of cutting global carbon emissions, because instead of generating carbon emissions in the U.S., these companies would just shift their emissions somewhere else.

There are thus at least two major reasons to include a border adjustment mechanism in a carbon tax: preventing the carbon leakage described above and preserving U.S. manufacturers’ competitiveness against foreign manufacturers. These two reasons are, however, related. Subjecting imported goods to the U.S. carbon tax means that all goods consumed in the United States would face the same tax. . Meanwhile, rebating carbon tax on exports means that producers in the United States would face no competitive disadvantage in foreign markets. In both cases, border adjustment would eliminate the incentive for companies to shift their production overseas.

A paper by Joseph Aldy, based on work by the Stanford Energy Modeling Forum, gives an idea of the magnitude of potential carbon leakage. Aldy is a professor at Harvard University focusing on climate change policy and energy policy. Carbon leakage can be measured as the ratio of the increase in foreign emissions to the reduction in domestic emissions caused by a given change in policy. For 12 models reviewed by Aldy, emissions leakage rates range from 5 percent to 19 percent, with an average of 12 percent.

Adele Morris, a senior fellow at the Brookings Institution, reviews several research studies on the potential emissions leakage from a U.S. carbon price and concludes that emission leakage is likely to be small compared to total U.S. emissions reductions. She argues that the primary goal of a border adjustment under a carbon tax is to “address the economic and political concerns of the most vulnerable industries, not to prevent emissions leakage.” However, as explained above, these two goals are related.

Designing a Border Adjustment for a Carbon Tax

In contrast to a VAT, a carbon tax is somewhat challenging to apply to imports and to rebate on exports. This is due to the difficulty of evaluating the carbon emissions associated with a product. Unlike sale prices of products that are used in calculating a VAT, carbon emissions are not readily observable. Sophisticated and reliable methods need to be developed to measure the carbon emissions associated with products.

In designing a carbon-tax border adjustment, three important issues need to be considered. First, eligibility, or which industries and products would be subject to the border adjustment. Second, the magnitude of the border adjustment, or how much tax should apply to imports and how much tax should be rebated at the border for a particular product. Third, whether policymakers need to consider the origin of a good when applying import taxes or export rebates.

Border adjustment eligibility

From the perspective of administrative burden and cost, it’s relatively straightforward to implement border adjustments on VAT, since the regulator only needs to know the sale prices of a given product. A levy on an import and a rebate on an export would simply be the sales price multiplied with the tax rate. However, to border-adjust products under a carbon tax, the regulator needs to determine the carbon emissions associated with imported and exported goods, which is a more complex and time-consuming task than merely collecting data on products’ sale prices.

Ideally, a border adjustment should cover a broad base of goods based on the carbon emissions associated with producing the goods. However, this may prove to be too administratively challenging. Therefore, to ease administrative burden and cost, lawmakers might design a border adjustment to only apply to a select list of goods that meet specific criteria.

Lawmakers could identify a list of goods that account for most of the emissions in the economy. Existing carbon tax proposals have included different screening criteria, such as using a threshold to screen goods or specifying eligible goods. Some examples of threshold criteria in existing proposals are screening for goods with at least a certain level of GHG intensity or energy intensity of production. The goal is to target the goods that contribute the most to carbon emissions in the economy, which aligns with the environmental purpose of the carbon tax. Typically, policymakers would adopt the same screening criteria for both exported and imported goods.

However, setting an emissions threshold for goods to be eligible for border adjustment could potentially create an incentive for exporters to game the mechanism. An exporter would have incentive to increase their carbon emissions on the margin to be eligible for an export rebate. To prevent this gaming behavior, policymakers could look at a firm’s average carbon emissions across all its domestic production instead of just looking at the production of exported goods.

There might also be potential issues with using energy intensity as an eligibility criterion. An energy-intensive product is not necessarily greenhouse-gas-intensive. If an imported energy-intensive product uses hydropower as its energy source, it would be subject to import tax despite having relatively low carbon emissions compared to combustion of fossil fuels. A carbon-intensive good also does not have to be energy-intensive. Besides fuel combustion, a chemical process could also generate a significant amount of greenhouse gas.

How to set the magnitude of border adjustment

Once policymakers determine which industries or goods are eligible for border adjustment, they need to design the methodology to calculate the magnitude of border adjustment applied on imported and exported goods. The magnitude of the tax is equal to the rate times the carbon content.

Exported goods

In a VAT, a credit-invoice method is widely used by countries to collect taxes. The Tax Policy Center has a clear explanation of how this works: “All sales by businesses are taxable, but sellers pass invoices on to the VAT-registered business taxpayers who purchase the sellers’ goods and services. These purchasers, in turn, claim a credit for taxes paid but then pay VAT on the full value of their sales.” Once a good gets to the border for export, the government knows how much to rebate because that information is on the invoice the exporter received from its domestic supplier.

This same mechanism could be used to administer the export rebate in a carbon tax. Resources for the Future (RFF) proposes a framework that is analogous to the credit-invoice method used in VAT. The framework is designed to measure the cumulative GHG emissions from suppliers to manufacturers. It has two key elements: first, track the cumulative GHG emissions from all inputs and add those to the firm’s emissions from all its domestic facilities; second, apportion across the firm’s product portfolio and assign emissions to a specific product. Once a good is at the border for export, there is sufficient information for how much of the good was subject to a carbon tax in the production process. The rebate can be applied based on that information.

According to the framework, to track the cumulative carbon emissions across the supply chain, existing voluntary reporting guidelines used by energy-intensive and trade-exposed (EITE) industries can be leveraged. The framework does not require examining each step in the production process. The first few production steps usually account for most of the GHG emissions in the entire production process for manufacturing EITE products. Once these energy-intensive steps are accounted for, the remaining production steps can apply simple rules such as “based on the carbon content of the processed fuel” or “average emissions per unit weight of precursors incorporated in the final product.” The framework suggests that firms, trade associations, and regulators need to work together to develop appropriate guidelines for allocating emissions to certain products, especially for some facilities that manufacture multiple products using different technologies and processes.

While some exported goods and their inputs are produced entirely domestically, some exported goods use inputs that are imported from other countries. If an exported product uses imported inputs, those imported inputs would have faced border adjustment at import. In other words, the products that go into the final exported good as inputs would have been taxed as if they were produced domestically and have receipts from the border adjustment. The question then becomes how the carbon content of goods imported for final sale in the U.S. should be accounted for. That is the subject of the next section.

Imported goods

It’s pretty straightforward to determine the carbon emissions of exported goods that are produced entirely domestically. But it’s not as obvious for imported products. One option would be to apply the same methodology used in calculating domestic products’ carbon emissions to imported products, which would require a significant amount of work by foreign governments and manufacturers to track cumulative emissions along the supply chain. This could potentially cause fraud issues in which foreign governments or companies underreport their emissions numbers. It would also be a heavy administrative burden for the U.S. government to manage and validate data provided by importers. Moreover, in some cases emissions data might not be available for a specific company or manufacturing facility, which makes implementation of the tax difficult.

Alternatively, the U.S. government could tax imported products based on a “like” product approach. This approach would levy a tax on an imported product that is equivalent to the carbon tax on a “like” domestically manufactured product. Jennifer Hillman, previously a member of the WTO’s Appellate Body, argues that the safest option from a WTO law perspective would be to “assume that the carbon content of the imported product is equal to the carbon content of the like product produced by the ‘predominant method of production’ or even the ‘best available technology’ in the United States.”

In this way, administratively, the Treasury only needs to find a credible way to “match” an imported product with a “like” domestically manufactured product, and apply the same methodology to the imported product to determine its associated emissions as if it were produced here in the U.S. Not only would this approach significantly decrease the administrative burden and cost, it would also reduce the risks of violating the applicable WTO rules.

There are implications to a “like” product approach. If a country has higher carbon emissions associated with producing a product than the “like” product in the United States, this approach would underestimate the actual carbon emissions with the imported product. However, as discussed above, it would be administratively burdensome to account for imported products’ carbon emissions accurately.

If a country has lower carbon emission associated with producing a product than the “like” product in the United States, a government agency would be needed to investigate and rule on foreign companies’ disputes on import taxes. Since the Department of Commerce has experience in enforcing antidumping and countervailing duties, it has the capabilities to establish an entity to deal with petitions from foreign companies if they can demonstrate that their products are associated with lower carbon emissions than they are charged for in the imports levy.

Consideration of a good’s origin or destination

Whether the import tax assessed under border adjustment should vary depending on the origin of a good is a question policymakers should evaluate on three grounds: legal, administrative, and economic.

From the legal perspective, it is important that a border-adjusted carbon tax comply with WTO rules. The literature generally agrees that it’s challenging but nonetheless possible to design a carbon tax policy that would be permissible under the WTO rules. An in-depth analysis of the WTO rules is not included in this paper, but should be an important topic to address in further research.

The WTO agreements that are applicable to a border adjustment mechanism are different for imports and exports. The General Agreement on Tariffs and Trade (GATT) restricts the ways in which WTO members impose taxes on imported goods, and prohibits discrimination among member countries through the most favored nation (MFN) clause. The Subsidies and Countervailing Measures (SCM) agreement prohibits countries from giving subsidies to exported goods. However, both these agreements have exceptions that allow countries to border-adjust imports and exports to account for consumption taxes.

Should the origin of a good be considered when applying the import tax? Scholars and researchers disagree on whether a border adjustment should consider the origin of a good when applying the import tax. The primary disagreement is how climate policies, or the lack thereof, in foreign countries should be counted when goods are imported. Some argue that all imports should be border adjusted at the same rate as the domestic carbon tax rate, while others argue that the rate for imported goods can be adjusted based on the carbon pricing policies in the jurisdiction of origin.

Those who are in favor of adjusting the import tax based on the origin of the imported good see this as potential leverage in diplomatic engagement. They believe that granting other countries with domestic carbon pricing policies exemptions or partial reduction of the import charges (assuming the policy can survive the WTO rules) can pressure trading partners to enact carbon policies to keep up with the United States’ carbon pricing ambitions. Additionally, if an importer already pays for a carbon tax in the origin country of production, then it’s not necessary for the importer to incur the full amount of the U.S. import tax. Such an importer might only need to pay for any difference between the origin country’s and the U.S. carbon price, if the origin country’s carbon price was less than that of the United States.

While it may be a well-intentioned effort to incentivize other countries to establish carbon tax policies to keep up with the U.S. carbon tax level, establishing a border adjustment mechanism with differentiated treatment for different countries is problematic on legal, administrative, and economic grounds.

From a legal perspective, it could violate WTO’s MFN treatment. Levying a reduced amount or even waiving the import levy on some countries while charging a full amount to other countries could be considered as discrimination based on country origins. Jennifer Hillman argues that if the U.S. decided to take into consideration foreign countries’ carbon policies, then it would need to defend its decision under the General Exceptions provisions in Article XX of the GATT. This article grants exceptions to measures “necessary to protect human, animal or plant life or health” or “relating to the conservation of exhaustible natural resources if such measures are made effective in conjunction with restrictions on domestic production or consumption.”In terms of practicality of administration, it would be extremely complex and difficult to determine other countries’ domestic carbon pricing, especially if a country’s carbon policies consist of a combination of a carbon tax or a cap-and-trade program, subsidies, and regulations. Even if carbon prices in other countries can be determined, more resources would still be needed to update the prices on a regular basis. Additionally, it would be almost impossible for the U.S. government to deter evasive trans-shipping behaviors. If the U.S. determined that imported goods from certain eligible countries are exempted partially or fully from the import tax, then importers would have an incentive to ship their products to the exempted countries, and then transport the products to the U.S. from there to avoid the import tax.

From an economic standpoint, one issue that is often overlooked is that if the U.S. decided to modify its border adjustments to accommodate other countries’ domestic carbon tax policies, then foreign governments would have incentives to max out their carbon tax rate to collect revenue that could have been collected by the U.S. government.

Considering the challenges discussed above, some have proposed implementing a carbon border adjustment mechanism that does not recognize other countries’ carbon policies. The carbon tax proposal from RFF proposes a border adjustment approach that “does not take account of GHG policies, regulations and costs already imposed in the exporting nation” and applies “equally to all nations.” The authors believe that this approach is not only WTO compliant, but also helps cut all the administrative costs associated with calculating foreign countries’ carbon cost. Under this proposed framework, the U.S. government would be able to collect import tax revenue to the full extent designated by the policy, without potentially losing revenue to foreign governments. Moreover, if the U.S. did implement the border adjustments disregarding other countries’ carbon policies, then other countries that have domestic carbon pricing policies would have incentives to rebate the carbon tax/fee to their exporters selling to the U.S. market to preserve their competitiveness.

Should the destination of a good be considered when applying the export rebate?

Although the WTO’s SCM agreement prohibits providing subsidies for exports, footnote 1 to the agreement notes that “the exemption of an exported product from duties or taxes borne by the like product when destined for domestic consumption, or the remission of such duties or taxes in amounts not in excess of those which have accrued, shall not be deemed to be a subsidy.” Therefore, it is crucial to construct a transparent and clearly defined methodology to calculate the rebates on exports to make sure they don’t exceed the tax liability incurred by domestic products.

As with a varying levy on imports, treating exports to different destinations differently to account for destination countries’ carbon tax policies would violate the MFN provision contained in Article I of GATT. Again, there are arguments that certain articles in the WTO rules could be used to defend differential treatment based on the country of origin in an export rebate.

In addition to the legal constraints, applying the export rebate to countries differently based on their domestic carbon prices would encounter similar administrative challenges as described in the analysis above on imports.

Administration of a border adjustment for a carbon tax

If a carbon tax policy with a border adjustment mechanism was passed in the U.S., it would take more than the Treasury Department to implement it. It’s important to coordinate different federal agencies to administer the policy effectively and efficiently. Treasury is specialized at collecting taxes and managing large amounts of financial flows; the Environmental Protection Agency already has programs in place to collect facility-level GHG emissions data; and U.S. Customs and Border Protections collects tariffs.

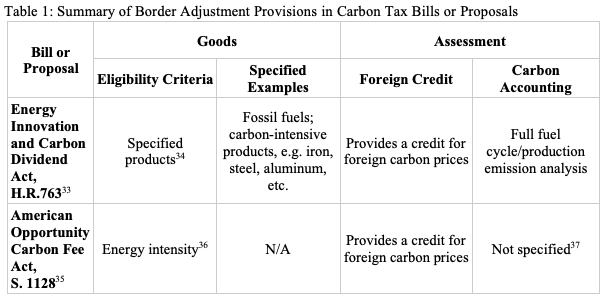

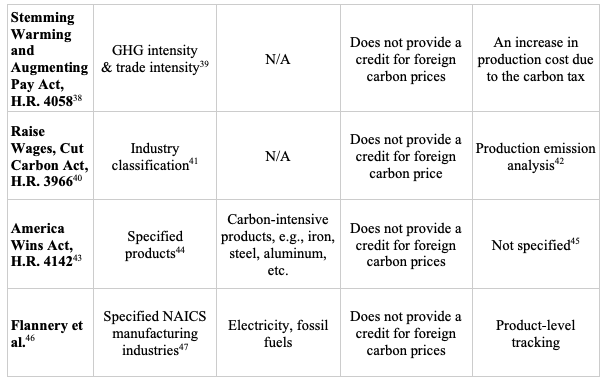

Review of Existing Carbon Tax Legislation

Eight carbon tax bills were introduced in Congress in 2019. Seven included some form of border adjustment. Table 1 reviews five of the bills and provides a high-level overview of the border adjustments they propose. The RFF proposal is included in the comparison because they have created the most specific framework for tracking carbon emissions through the supply chain.Different eligibility criteria are used in these proposals to screen goods for border adjustments, including carbon intensity, energy intensity, and industry classification. Carbon intensity is used in three of the six proposals.

Most of the proposals do not provide a credit for foreign carbon pricing, but the Energy Innovation and Carbon Dividend Act and the American Opportunity Carbon Fee Act both propose accommodating foreign countries’ carbon pricing when determining the border adjustment magnitude.

The RFF framework is the only proposal that provides a methodology for tracking carbon emissions through the supply chain at the product level. Other proposals use production emission analysis or increased cost analysis to determine carbon emissions associated with products.

Recommendations and Future Research Questions

- A border adjustment under a carbon tax should cover a broad base of goods based on the carbon emissions associated with producing the products, while many current proposals limit the goods eligible for adjustment to emissions-intensive primary products. Whether the administrative costs of border-adjusting a broad base of products, including primary and finished products, would be reasonable is an important topic for future research.

- A “like” product approach — where imported goods are assigned a carbon tax based on the carbon intensity of locally produced goods in the United States — can be used to ease administrative burdens and comply with the WTO rules.

- A government agency needs to be designated to investigate and rule on foreign companies’ disputes on import taxes in cases where foreign companies have lower emissions associated with their products than “like” products in the United States.

- A mechanism like the credit-invoice method used in a value-added tax could be developed to track cumulative carbon emissions along the supply chain to determine emissions associated with manufacturing a certain product at the firm level. An in-depth analysis of how to make such a mechanism economically and administratively feasible needs to be conducted in future research.

- Border adjustment should not vary to accommodate other countries’ domestic carbon pricing policies. This would ensure that border adjustment is compliant with the MFN clause in WTO rules, administratively feasible, and maximizing the U.S. government’s tax revenue. Future research needs to look into what would be effective mechanisms to incentivize global collaboration on climate mitigation efforts.

Conclusion

Border adjustments are widely used throughout the world in a number of taxes, most commonly the value-added tax. The goal of border adjustments is to equalize the tax burden on imported goods and domestically produced goods, as they are both consumed within the same jurisdiction.

A border adjustment for a carbon tax works by applying a tax on imports and rebate on exports. It helps in preventing carbon emission leakage and preserving U.S. manufacturers’ competitiveness against foreign manufacturers.

In designing a carbon-tax border adjustment, three important issues need to be considered: first, what industries and products would be eligible for the border adjustment; second, the magnitude of the border adjustment; third, whether policymakers need to consider the origin or destination of a good when applying import taxes or export rebates. Administration of a border adjustment for a carbon tax is also important and will be addressed in a follow-on research paper.