Larger per-child benefits are a far better way to support children than tax advantages for unmarried parents.

Last week, Republican Senators Mitt Romney of Utah, Steve Daines of Montana, and Richard Burr of North Carolina unveiled their proposal to expand income supports for American families with children. As policymakers weigh the plan’s proposed benefit changes and accompanying pay-fors, a provision they should take seriously is folding the existing head of household (HoH) filing status benefit into such a package.

Overview of the HoH

HoH filing status lowers the tax liability of unmarried individuals who care for a dependent. Prominent voices on the left and right have called for the filing status to be scrapped as part of a broader overhaul of child benefits. The broad ideological appeal stems from the poor design of the HoH status. It not only disproportionately benefits the rich and fails to account for the number of children in a home, but also discourages marriage and needlessly increases the tax system’s complexity.

Head of household filing status reflects outdated policy design principles. HoH was established in 1951 for the expressed purpose of providing aid to single parents with children. At the time, financial assistance to families was delivered through a combination of regressive tax advantages such as deductions and exemptions, along with means-tested welfare for the poor, such as the Aid to Families with Dependent Children (AFDC) program for supporting non-working single parents. In more recent years, policymakers have generally preferred to expand aid to children through the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC), established in 1974 and 1997, respectively. This movement in favor of per-child rather than household-status benefits mirrors international trends. For example, the United Kingdom completed the shift in the 1990s.

HoH is regressive

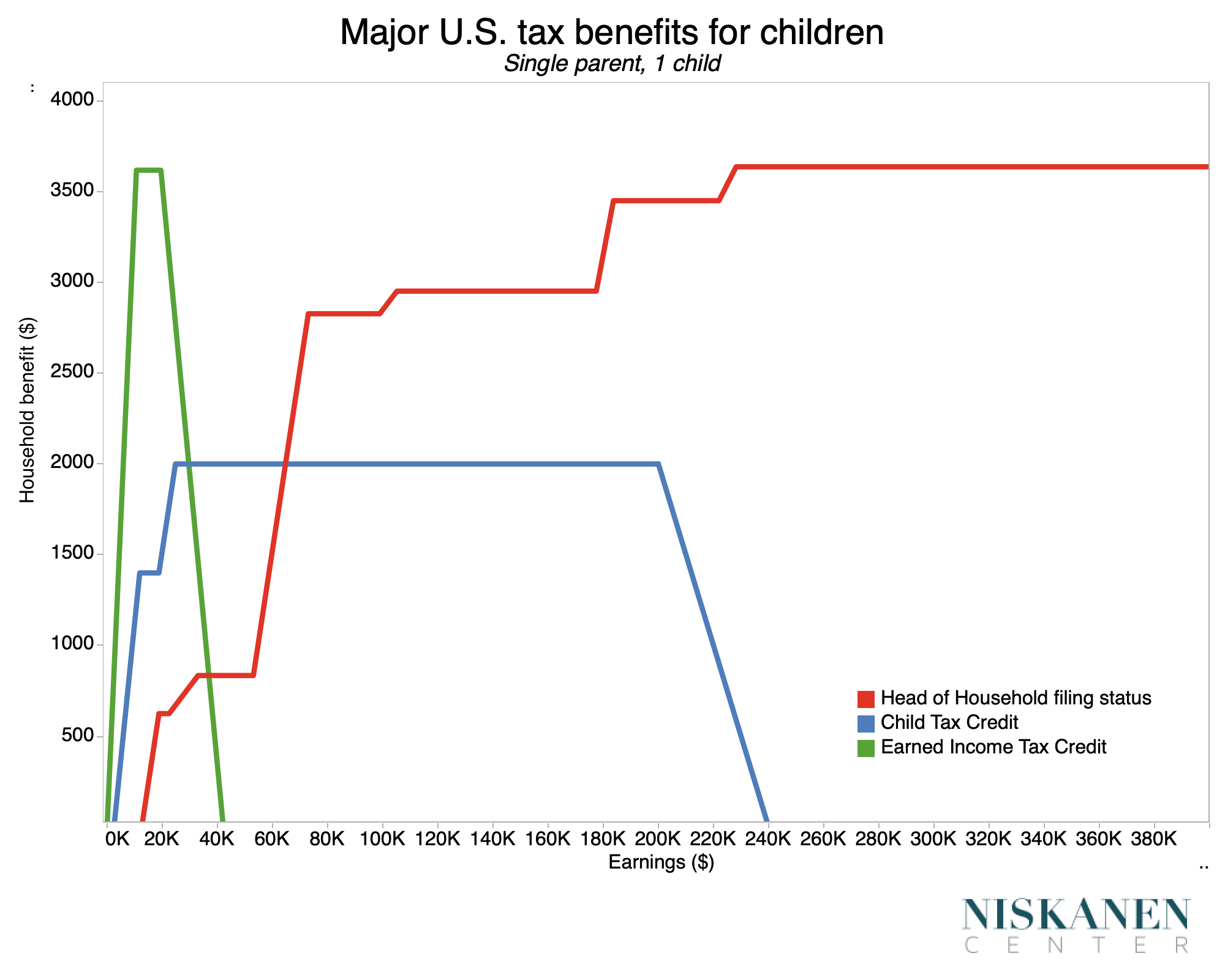

As the chart below highlights, the HoH benefit is extremely regressive. For ordinary income, the HoH benefit provides a boosted standard deduction ($6,450 increase over singles in 2022) and allows the second and third marginal tax brackets to kick in at a higher income. For the lowest-income parents, HoH’s structure provides quite modest relief relative to single-filing because they’d have little-to-no tax liability anyway. But this situation changes dramatically as income increases. Deductions, unlike credits, shave off a set amount of pretax income. They are worth more as filers move into higher marginal tax brackets (the $6,450 deduction is worth a lot more when each dollar is taxed at the top rate of 37 percent rather than the 10 percent rate of the lowest taxable bracket). Delays to the point at which higher tax rates kick in are similarly poorly targeted because of how they exclude households with low incomes. This regressive structure results in the HoH child benefit peaking at a value slightly after the Child Tax Credit has already begun to phase out.

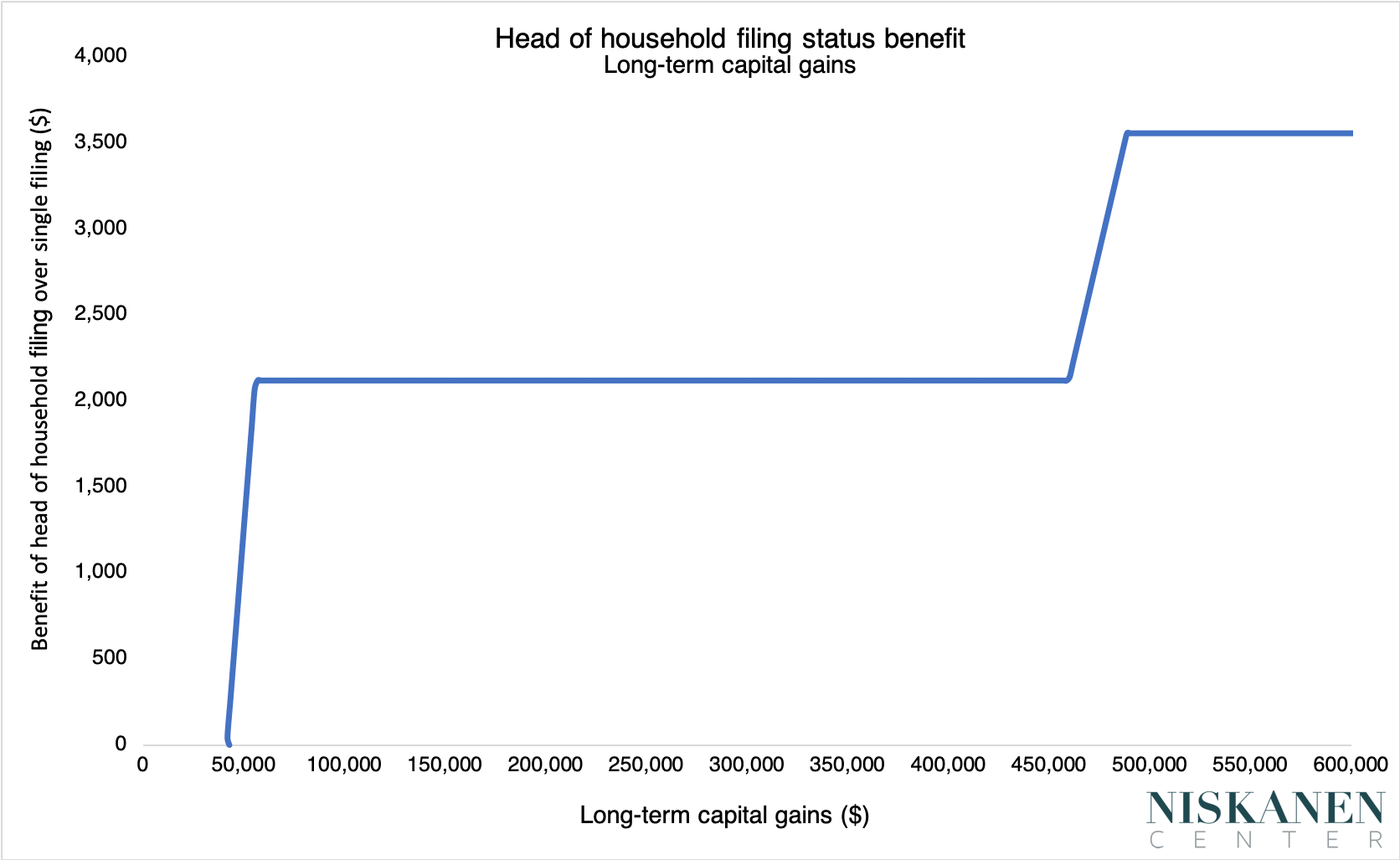

The head of household filing status also benefits single parents by extending lower tax brackets on long-term capital gains. Long-term capital gains taxes are applied to profits from the sale of assets (housing, stocks, cryptocurrencies) that are held for more than a year and feature rates lower than those applied to ordinary income. Yet only the top one percent of filers within a given year will even realize enough long-term capital gains to face the tax (and benefit from its relatively lower rate). And HOH filers’ long-term capital gains tax advantages are further augmented by a $75,000 increase over single filers to the gross income threshold at which the Net Investment Income Tax kicks in (from $125,000 to $200,000). Delivering tax benefits for children on a regressive basis makes little sense because parenting places greater strain on lower-income households. That the head of household filing status currently does exactly this, therefore, reflects bad policy design.

HoH discourages marriage

The head of household filing status embeds a marriage penalty in the U.S. tax code. Marriage penalties in the tax code arise when the combined value of tax credits and deductions for two single individuals arbitrarily drops when those same individuals marry and file taxes jointly—creating a disincentive to marry legally. Since married couples do not receive additional tax advantages similar to HoH for having children, a single filer and an HoH filer with roughly equal earnings can be taxed at a lower rate than if they got married. For comparison, the current CTC does not similarly discourage marriage because the phase-out threshold for married households is equal to that of two single individuals, and the benefit is delivered on a per-child basis.

HoH fails to account for multiple children

Since the HoH is delivered based on the marital status of the parent rather than the number of children in the household, it points to another issue with the benefit’s structure: HoH doesn’t take into account the increased financial strains associated with having multiple children. While the HoH tax filing benefit does provide a boost in income to eligible households upon the birth of the first child, the birth of subsequent children yields no additional benefit. So long as their earnings are equivalent, an HoH-eligible household with six children receives just as much benefit from the tax filing status as a household with one child. As a result, the HoH has the effect of discriminating against larger families when compared to a per-child benefit.

HoH is a source of needless complexity in the U.S. tax code

Finally, the continued existence of the HoH tax filing benefit creates complexity for families filing their taxes as well as for the administering tax authorities. What exactly “head of household” means is not straightforward or intuitive without prior knowledge of the U.S. tax code. Improper choice of filing status, resulting in under- or overpayment of taxes, is common, according to the IRS. Doing away with head of household filing status would be a necessary first step towards entirely replacing separate tax-filing statuses with simpler, more transparent, and less regressive methods of aiding families, as many other countries have done.

Complementary and alternative reform options

Aid to children is best delivered through per-child benefits. Policymakers eager to address the challenge of child care expenses for single parents could best direct their attention to reforming and increasing funding for the Child Care and Development Block Grant. Policymakers worried about the impact on caregivers of adult dependents could consider increasing the value of the Credit for Other Dependents.

Lastly, should policymakers, for whatever reason, determine that single parents come out unacceptably well under a child benefit expansion that folds in head of household filing status, it’d be preferable for policymakers to either increase the value of the per-child benefit further or provide a sufficiently large “family bonus” to the earned income tax credit. These changes would allow low-income households to be made even better off regardless of marital status. However, should policymakers find themselves unwilling to do away with HoH entirely, the next-best option would be to convert the head of household filing status into a single-use, nonrefundable credit, worth $800 or so. A credit of this amount would replace any loss at the bottom of the income scale while preserving most of the benefits of ditching the separate tax-filing status.

Conclusion

The head of household filing status is not only distributionally regressive and insensitive to family size, but also penalizes marriage and needlessly complicates the U.S. tax system. The filing status should be repealed in order to fund larger per-child benefits. Head of household filing status is ripe for scrapping in hopes of a larger child benefit reform package.

Photo credit: iStock