This piece is part of a series of briefs looking at specific state proposals for family tax benefit reforms based on a more comprehensive Niskanen report, The State of our Families: Child and Dependent Tax Benefits in the States. You can find other state briefs here.

In 2006, New York became the first state to introduce a permanent fully refundable child tax credit. The Empire State Child Credit (ESCC) was a classic kludge, assembled in a manner that got it passed but made it ugly in the process. The credit is worth 33 percent of the federal child tax credit as it was structured before Congress’ 2017 tax reforms. It (in)famously excludes children younger than four years old. Legislators in New York have been exploring reforms to fix these perceived shortcomings for as long as it’s been law.

Led by Senator Andrew Gounardes (D), a growing cohort of reformers is sponsoring an ambitious bill (S277) that would consolidate the ESCC and the children’s portion of New York’s state Earned Income Tax Credit (EITC) into a single expanded Working Families Tax Credit (WFTC) that would provide $500-$1,500 per child.

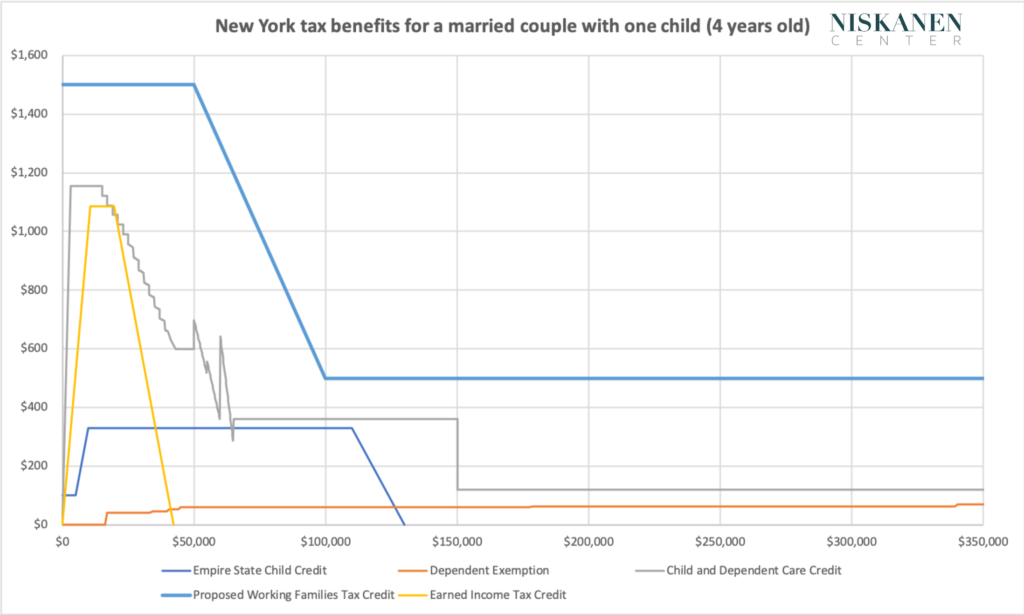

Instead of the ESCC and EITC, each child would be eligible for a $1,500 fully refundable credit in single households making up to $25,000 and married households making up to $50,000. Beyond these thresholds, the credit is phased down at a 2 percent rate until reaching a minimum of $500 per child after that. Figure 1 shows the distribution of the proposed WFTC alongside the ESCC, EITC, Child and Dependent Care Credit (CDCC), and Dependent Exemption (DE).

Figure 1: Distribution of dependent exemption and proposed CTC benefits

Benefits

The structure of the proposed WFTC is a marked improvement over the two refundable tax credits it would replace. As a fully refundable and universal credit, it would reach all families with children, providing them with support to help with the cost of raising them. The WFTC expands eligibility to children under four years old, finally fixing one of the worst features of the ESCC.

Moreover, by consolidating two existing credits into one, the WFTC reduces complexity for families and helps keep the overall cost of the reforms lower than it would be relative to layering new credits on top of existing ones.

The phaseout threshold for the WFTC is lower than that for the ESCC but higher than that for the EITC. These threshold level changes are less significant than the added adjustments it makes for marital status and reduction in phaseout rates. The marriage penalties built into the federal EITC and pre-2017 CTC, on which New York’s EITC and ESCC are modeled, are well known. The same is true for work penalties stemming from the phaseout of both credits. By doubling the phaseout threshold for married couples, streamlining the phaseout rate down to 2 percent, and phasing credits down but not out altogether, the WFTC substantially reduces work and marriage penalties for families.

Overall, the credit is a great example of the benefits of “targeting within universalism,” where all families receive support, but additional support is provided to lower-income families with the greatest need.

Drawbacks

The WFTC would require a substantial fiscal commitment. The current proposal overlooks potentially significant cost savings and simplification by going even further and consolidating additional overlapping family tax benefits. Replacing the EITC ($807.5 million) and ESCC ($616 million) provides the bulk of the savings but the dependent exemption ($279.5 million) and CDCC ($167 million) are also big-ticket items in the budget that similarly provide benefits to families.

The CDCC is particularly ripe for consolidation. In theory, the CDCC is most generous to the lowest-income households but only some of these families have the out-of-pocket qualified expenses to meet the eligibility requirements. As a result, families making over $100,000 per year are substantially more likely to receive the credit than those making less than $30,000 per year (where the average credit for the very few that actually benefit is a more modest $559 relative to the theoretical maximum of $1,155).

Improvements

Consolidating the EITC and ESCC into the WFTC is a great first step.Still, there is no reason to stop there when the dependent exemption and CDCC could help defray its overall cost, radically simplify benefits, and leave the vast majority of families better off than they are under the status quo.

Drawbacks aside, New York’s proposed WFTC is the boldest state proposal we have seen since the introduction of the ESCC almost two decades ago. With enough hindsight to avoid the mistakes of the past, the WFTC could be the model for comprehensive state tax credit reform.