The current Child Tax Credit is worth up to $2,000 per child under 17 years old. The credit has two components – a nonrefundable portion and a refundable portion – that ensure the credit phases in as household income rises. Families who have not earned any income in the past year are not eligible to receive the credit.

The nonrefundable portion of the credit gives families a dollar-for-dollar reduction in federal income tax liability. Because many working-class families have little or no income tax liability, Congress added a refundable portion that families can claim above and beyond their federal income tax liability, to extend the credit to more working families. The refundable portion, often called the Additional Child Tax Credit, provides families with a credit equal to 15% of their earnings that exceed an initial $2,500 earnings threshold, up to $1,600 per child. The remaining $400 can only be claimed as a nonrefundable credit.

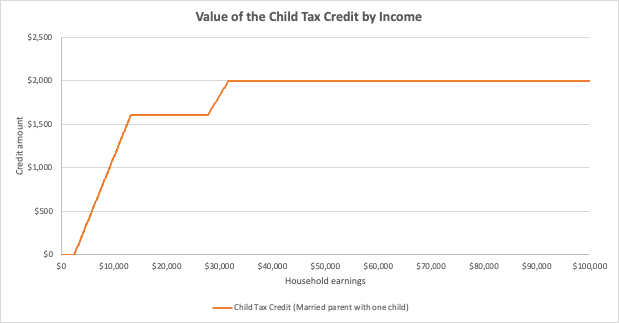

Figure 1 illustrates how this works for a married couple with one child. The credit phases in at a 15% rate between $2,500 and $13,200 in earnings. The credit amount then plateaus until earnings reach $27,700 – the value of the standard deduction for married couples – at which point it phases in at a 10% rate until reaching the full $2,000 credit value.

Figure 1. Value of Child Tax Credit for Married Couple with One Child

The expansion of the refundable portion of the credit has extended access to more low-income working families. Yet, it is still possible for a parent to work full-time and not receive the full credit. This is particularly true for households headed by married parents relative to single parents. Table 1 illustrates how much a household earning $15,000 (about full-time at the $7.25 federal minimum wage) and $30,000 (about twice the $7.25 federal minimum wage) would receive depending on marital status and number of children.

Table 1: Child tax credit based on income, marital status, and number of children

| Earnings | Single, one child | Married, one child | Single, two children | Married, two children |

| $15,000 | $1,600 | $1,600 | $1,875 | $1,875 |

| $30,000 | $2,000 | $1,830 | $4,000 | $3,430 |

Of the eight scenarios here, only the single-parent households earning twice the federal minimum wage can claim the full credit. Married parents earning the same amount would still only be able to claim a partial credit. The credit’s partial refundability (only the first $1,600) and initial threshold ($2,500 earnings) for beginning to phase-in the refundable portion are the main reasons we see this. One of the unintended consequences of the more generous standard deduction for married couples is that they must earn much more than single households in order to claim nonrefundable credits, such as the remaining portion of the child tax credit in this case.

Eliminating the $2,500 earnings threshold and making the entire credit refundable at the same 15% phase-in rate would expand access to more working-class families by effectively reducing the income needed to claim the full credit. Table 2 looks at those same families under these reforms.

Table 2: Reformed child tax credit based on income, marital status, and number of children

| Earnings | Single, one child | Married, one child | Single, two children | Married, two children |

| $15,000 | $2,000 | $2,000 | $2,250 | $2,250 |

| $30,000 | $2,000 | $2,000 | $4,000 | $4,000 |

Of the eight scenarios here, six out of the eight households can claim the full credit. The disparities between single-parent and married-parent households disappear. Households with two children earning the minimum wage still would not receive the full credit but would receive more (an additional $375) than they currently do.

An additional option for ensuring households with two children earning the minimum wage receive the full credit is, in addition to the changes above, to increase the phase-in rate on the refundable part of the credit from 15% to 30% (see Table 3).

Table 3: Enhanced child tax credit based on income, marital status, and number of children

| Earnings | Single, one child | Married, one child | Single, two children | Married, two children |

| $15,000 | $2,000 | $2,000 | $4,000 | $4,000 |

| $30,000 | $2,000 | $2,000 | $4,000 | $4,000 |

Under this reform, any household with up to two children earning the minimum wage or twice the minimum wage would receive the full credit.

Eliminating the threshold and making the entire credit refundable at the same 15% phase-in rate or even an enhanced 30% phase-in rate would be a relatively inexpensive way to help more working-class families raising children while providing more equitable access to the child tax credit across single and married-parent households.