Every dollar in carbon tariffs the European Union collects from U.S. heavy industry this year is a dollar Washington could have collected first.

On January 1, 2026, the EU’s Carbon Border Adjustment Mechanism (CBAM) took effect, applying a charge to imports of carbon-intensive goods from countries that have not priced those emissions at home. These include steel, aluminum, cement, fertilizer, and hydrogen. The charge tracks the emissions embedded in each shipment — that is, the carbon released during manufacturing, calculated per metric ton of product. By 2028, U.S. exporters will lose more than a billion dollars that could have stayed in the United States had Congress put a domestic carbon price in place.

The amount may seem modest in the short term, but if the policy gap isn’t closed, it could cost billions before long

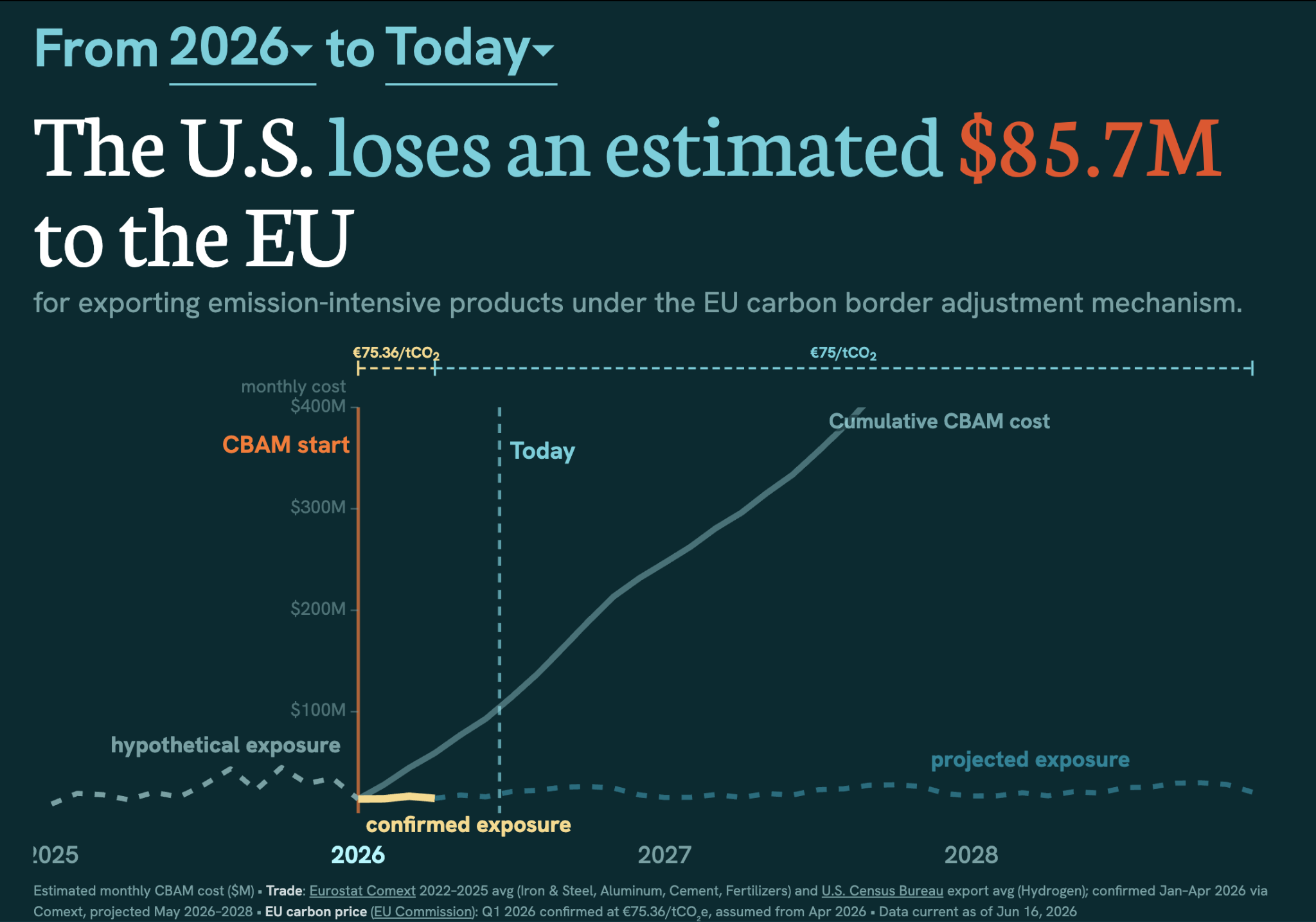

The Niskanen Center’s U.S. CBAM Exposure Calculator estimates Europe’s revenue at U.S. expense, sector by sector and month by month. At the official Q1 2026 carbon price of €75.4 ($88 USD) per metric ton of CO₂e, the U.S. stands to lose about $231 million this year alone, By 2028, with the EU’s planned escalating punishment in place, the costs will grow to roughly $271 million. The three-year cumulative bill could top $752 million.

And that’s if U.S. trade volume and carbon policy hold steady between now and the 2028 presidential election.

Fig. 1 Calculator snapshot showing year-to-date CBAM exposure, based on confirmed Eurostat trade volumes through March 2026 and projected volumes from April through publication.

The cumulative bill U.S. exporters have accrued since CBAM took effect on January 1, 2026. The pre-2026 line segment is hypothetical, showing what the cost would have been at the same prices and volumes before the policy was in force. Source: Niskanen U.S. CBAM Exposure Calculator.

How CBAM works and how we built the estimate

The EU CBAM requires every European importer of U.S. steel, aluminum, cement, fertilizer, or hydrogen to purchase emission permits, called CBAM certificates, at the same price European producers pay for carbon under the EU’s Emission Trading System (ETS). The first payment, for goods imported in 2026, is due September 30, 2027.

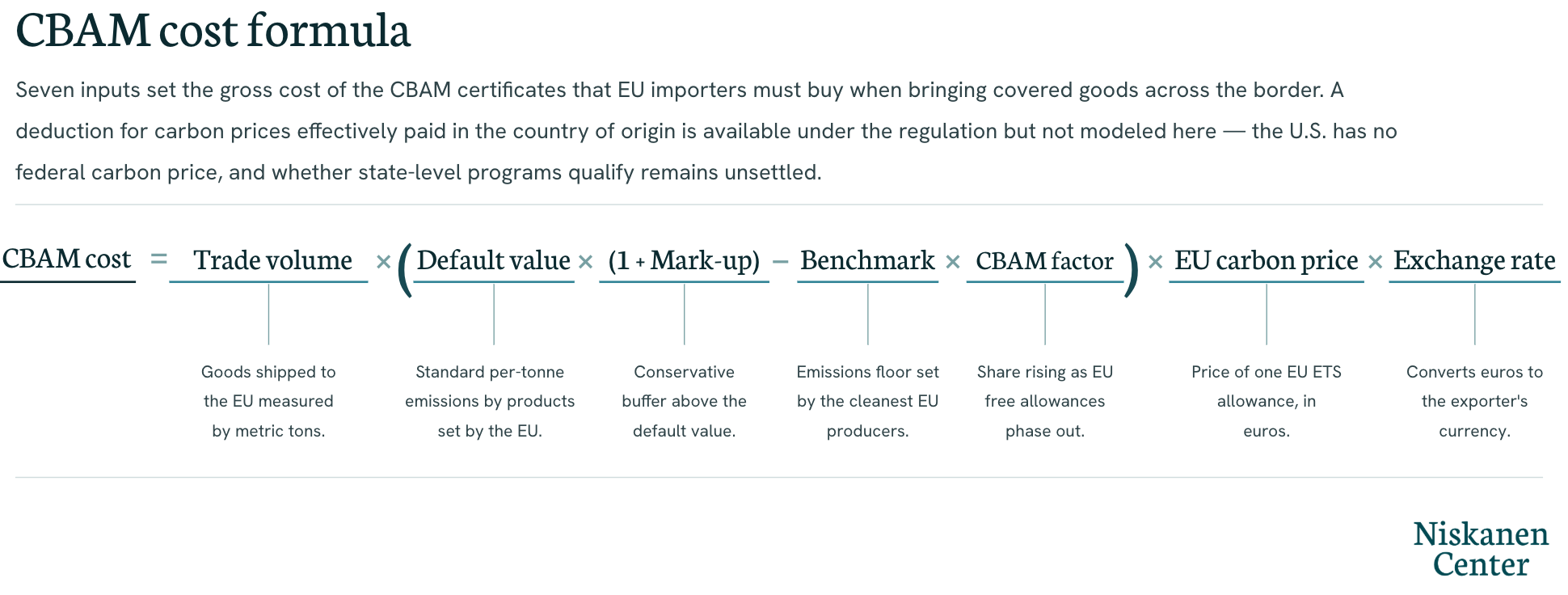

The calculator estimates the dollar value of CBAM exposure for U.S. goods shipped to the EU through the formula below:

Definitions

- Trade volume

- Goods shipped to the EU measured by metric ton. The data is fetched from Eurostat’s Comext database, which publishes monthly with a six-to-eight week lag.

- Default emission-intensity value & mark-up

- An EU-assigned emissions intensity (tCO₂e per metric ton of product) used when self-reported and verified emissions data is unavailable. Default values are typically conservative and may exceed actual emissions, incentivizing firms to report installation-level data. On top of that, the EU even imposed an extra mark-up value, which is a 10 percent–-30 percent surcharge, for companies that choose to apply the default values. The rate grows by year, designed to incentivize actual value submission. The EU has designated these values by country and by year in the EU Implementing Regulation 2025/2621, Annex I.

- Benchmark and CBAM Factor

- Together, these form the deduction that mirrors the free allowances that an equivalent EU producer would still receive under the EU ETS. As with the default value, the benchmark is a per-ton emissions reference level set by product. It represents the lower bound of EU emissions intensity, calculated by averaging the performance of the 10 most efficient EU installations. The CBAM factor is the phase-in percentage that scales how much of that free allocation is recognized each year; it starts at 97.5 percent in 2026 and declines to 0 percent by 2034 as EU free allowances are withdrawn. Multiplying the two gives the per-ton free allocation adjustment, which is the common deduction applied to EU and foreign producers of that product. Both the benchmarks and the CBAM factor are set in the EU Implementing Regulation 2025/2620.

- EU Carbon price

- The CBAM certificate price tracks the EU ETS, which sets allowance prices at weekly auctions. Each quarter, the EU averages those auctions into a single CBAM certificate price for the prior three months. The Q1 2026 price was confirmed at €74.36 ($86.47 USD) in April. For later quarters, the calculator lets users set their own price and will update when the EU releases the new prices.

- Exchange rate

- The rate will be the yearly average per the draft implementing act. We use the 2025 European Central Bank average (EUR/USD ≈ 1.13) as the best available proxy until 2026 closes.

- Year to date

- The year-to-date figure adds up CBAM costs from January 1 up to the date the user opens the calculator. For each product code, the calculator pulls confirmed Comext tonnage where Eurostat has published it and falls back to the 2022 to 2025 monthly average where it has not. The current month is prorated by the share of days elapsed. For example, if the user accesses the calculator on June 15, 2026, and Eurostat has published the March trade data, the calculator uses confirmed Comext data for January through March, the 2022 to 2025 average for April and May, and half of June’s average for the 15 days elapsed.

Why the estimate is an upper bound

The headline figure and all the cost estimates are best read as an upper bound for five reasons.

First, default emissions values are intentionally conservative. The EU’s mark-up schedule, from 10 percent in 2026 to 30 percent by 2028, is a deliberate nudge: defaults are meant to be uncomfortable enough that exporters submit verified data. For U.S. steel and aluminum producers running cleaner facilities than the EU baseline, verified reporting could cut exposure meaningfully.

Second, the projection averages 2022 to 2025 monthly trade to set the 2026 baseline. The first two months of confirmed 2026 data come in well below that mark. Iron and steel are running 85 percent below, aluminum 63 percent below. Whether this reflects firms anticipating CBAM costs or just one-off operational shifts is too early to tell. Whatever the cause, U.S. exporters are either avoiding the tariff or losing the EU market, and both are economic losses.

Third, the EU ETS price itself is uncertain, due to the auctioning nature and the pace that free allowances phase-out. The political environment in Brussels to maintain that pace has been bumpy, and a recent proposal suggests a longer and flatter phase-out trajectory. A slower phase-out would keep costs below the calculator’s projection.

Fourth, CBAM is paid by the importer, not the exporter. The cost passes back to the U.S. exporter only to the extent that EU buyers cannot absorb it or shift to other suppliers. Empirical work on tariff incidence finds that buyers with alternatives push much of the tariff back onto suppliers. How many EU buyers are walking away from U.S. suppliers and how many suppliers are gaining advantage because of the tariff remains to be seen, since the substitution process is still unfolding. The calculator reports the chip value for bargaining, not the net impact that lands on U.S. firms’ balance sheets.

Fifth, what counts as a carbon price “effectively paid” in the country of origin is still in play. The EU is currently consulting on the implementing act that will govern this question. One of the open issues is whether subnational carbon prices, such as California’s cap-and-invest system, count toward a deduction against the CBAM bill. The answer will affect both the actual exposure that lands on U.S. firms and the incentives facing manufacturers and federal policymakers as they consider how to respond.

The policy gap CBAM exposes

On its own, a few hundred million dollars in 2026 is not a crisis. By 2028, with mark-ups rising and the phaseout of the free allowances, the number is accumulating exponentially. More importantly, the EU is openly considering an expansion of CBAM scope to downstream products such as home appliances and vehicle components, and at least four other economies are now designing analogous policies.

There are two ways for the U.S. government to protect both its revenue and its exporting industries from the impact of high tariffs.

First is a domestic carbon price. If U.S. producers pay a carbon cost at home, goods arriving in Europe would be considered to have already paid an EU-recognized price. Whether state-level systems would be eligible remains unconfirmed, but a federal one is certain to count. This measure will bring the producer’s CBAM certificate obligation close to zero, and the revenue would stay in Washington rather than going to Brussels. Sen. Sheldon Whitehouse (D–R.I.), has reintroduced his Clean Competition Act, a sector-specific border-adjusted carbon fee on carbon-intensive U.S. manufacturing, with import charges and export rebates. It has an obvious path through Congress but it is nonetheless the only one aimed at stopping the U.S. from handing this revenue to Brussels.

The second is a Monitoring, Reporting, and Verification (MRV) approach. Congress could designate an agency to establish or endorse a credible, product-level emissions accounting standard so U.S. exporters can submit verified actual values to the EU and avoid the punitive default value. This is the lightest legislative lift, since it endorses a standard rather than imposing a charge. It could also help companies comply with future border carbon adjustments (BCA) that other countries might impose. It would not eliminate exposure, but it might be more acceptable to Congress since it would not impose an explicit fee on taxpayers.

The last thing we want to see is the U.S. losing a market it should be winning. Results from the first two months of 2026 trade already show U.S. firms retreating from the EU. Exporters could shift to other markets for now, but not for long, as several jurisdictions are actively designing BCAs. The question for U.S. policymakers is whether the country will keep ceding policy leverage and revenue to its trade partners, or design an instrument that captures the same economic value here. The European Commission is still finalizing the implementing regulations for CBAM deduction and carbon accounting. Without concrete data or a solid carbon price, the United States lacks a credible position at the bilateral negotiation table. The cost of arriving late will be paid either through tariffs or lost market share, but there will be a price.