The Tax Cuts and Jobs Act of 2017 successfully and comprehensively reformed our federal family tax benefits system for the first time in decades. The impending expiration of the law’s major provisions in 2025, including its family tax reforms, provides an opportunity to consider the value of these reforms and options for building on them with a bolder set of reforms.

One of the law’s goals, as laid in Speaker Paul Ryan’s A Better Way tax reform blueprint, was to simplify what were then two distinct tax benefits for families with children “each with its own rules, eligibility criteria, and calculations” – the personal exemption for dependents and the Child Tax Credit (CTC) – into a single, more generous Child Tax Credit. Beyond simplifying family tax benefits, the reforms would also reduce marriage penalties and fraud/improper payments. While the original blueprint proposed a $1,500 child tax credit to replace the dependent exemption, the law ultimately provided a more generous $2,000 Child Tax Credit.

In the wake of TCJA, there have been several proposals to rationalize our maze of family tax benefits further. The most comprehensive is the Family Security Act 2.0, which would consolidate five distinct tax benefits — the CTC, Earned Income Tax Credit (EITC), Child and Dependent Care Tax Credit (CDCTC), Head of Household (HoH) filing status, and State and Local Tax (SALT) deduction — into just two: an enhanced child benefit and simplified EITC.

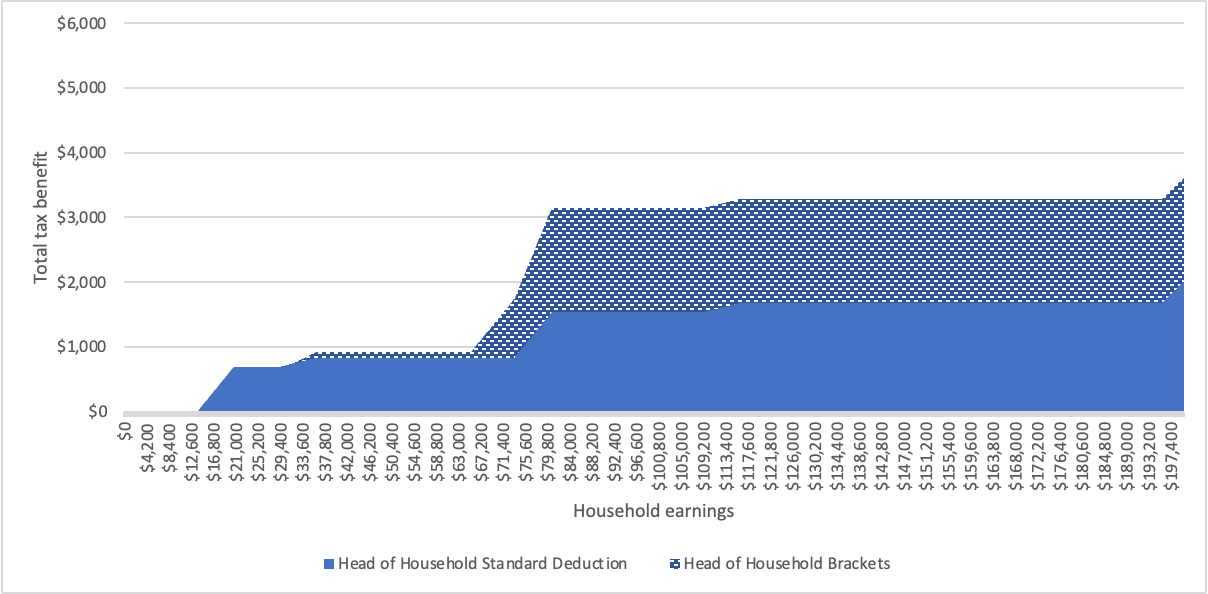

But what about more incremental reforms? One option worth considering is further changes to the HoH filing status. The 2017 tax reforms, which also eliminated personal exemptions and replaced them with a larger standard deduction, increased the overall proportion of households who choose to take the standard deduction. As we discussed in a recent report, single individuals caring for dependents – often children – can file as head of household. HoH filing status has two components: wider bracket thresholds relative to single filers and a more generous standard deduction amount relative to single filers. A similar filing status is not available to married couples with children. Figure 1 shows the value of HoH status relative to single status for those earning less than $200,000.

Figure 1: Value of head of household filing status relative to single

Like the personal exemptions used to expand the CTC in 2017, the benefit of HoH status increases with household earnings. It is worth about $65 to a single parent working full time at the federal minimum wage versus about $3,600 for a single parent earning $200,000. HoH filing status has several problems, including marriage penalties, unnecessary complexity, and not adjusting for family size, which makes it ripe for reform. One option that builds on the 2017 reforms would be eliminating HoH status (single parents would simply file as single) and further expanding the CTC for all families with children, regardless of marital status.

Three options for reform

Congress is divided on the merits of making the CTC “fully refundable” by eliminating the current phase-in altogether, but there is relatively broad support for reforms that change the refundable portion of the credit to phase the credit in faster for low-income working families. Based on recent proposals, we consider three “flavors” of reform (see Table 1).

Our TCJA style reform keeps the current earnings threshold and phase-in rate but makes the entire credit refundable,increasing its value to $3,500 per child. Our Rubio-Hinson style reform reduces the earnings threshold to the first dollar, slightly increases the phase-in rate to 15.3%, makes the entire credit refundable, and increases its value to $3,500 per child. Finally, our Smith-Wyden style reform keeps the current earnings threshold but changes the 15% phase-in rate to be per child rather than per household, makes the entire credit refundable, and increases its value to $3,500 per child.

Table 1: Summary of changes under each scenario

| Current | TCJA style | Rubio-Hinson style | Smith-Wyden style | |

| Earnings threshold for phase-in start | $2,500 | $2,500 | $0 | $2,500 |

| Phase-in rate | 15% per household | 15% per household | 15.3% per household | 15% per child |

| Credit amount | $2,000 ($1,600 refundable/$400 nonrefundable) | $3,500 (refundable) | $3,500 (refundable) | $3,500 (refundable) |

| Filing status options | Single, head of household, or married | Single or married | Single or married | Single or married |

We do not examine married parents more in depth here because they are not eligible for HoH status’ benefits. Any expansion of the CTC means they would be net winners or held harmless across the board. The interaction between HoH status and the CTC for single parents can be more complicated, so we provide overviews of the net impact – how much households would gain from an expanded CTC minus how much they would lose from eliminating HoH status – for each of the three options.

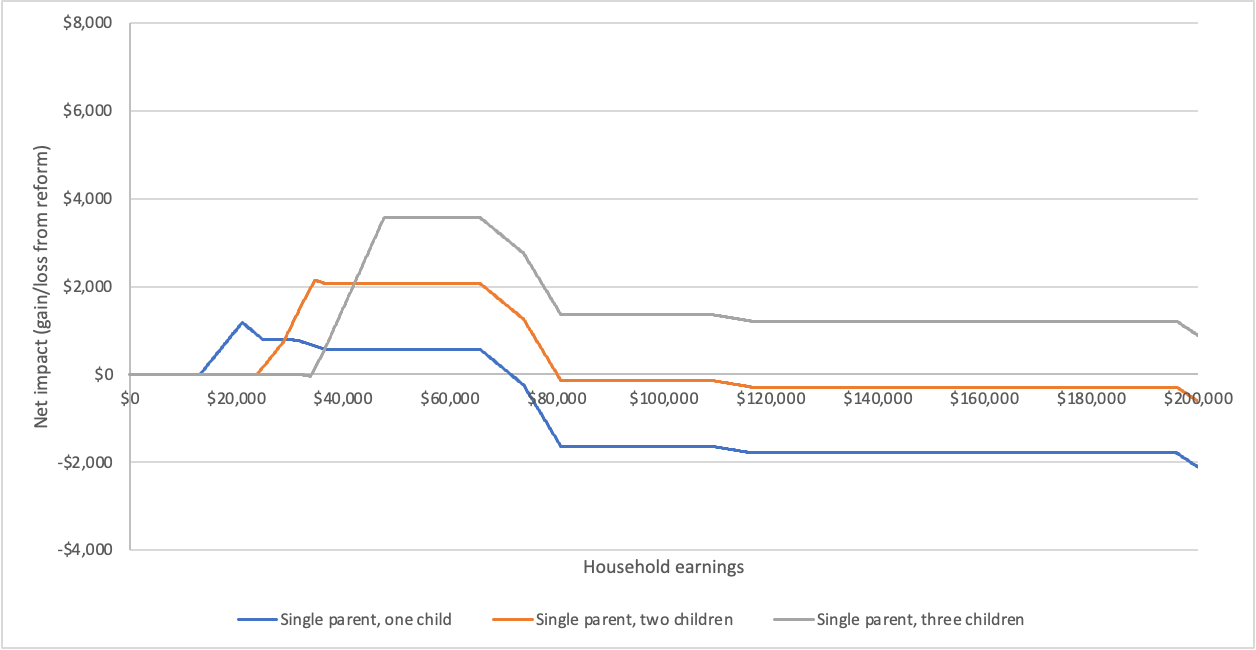

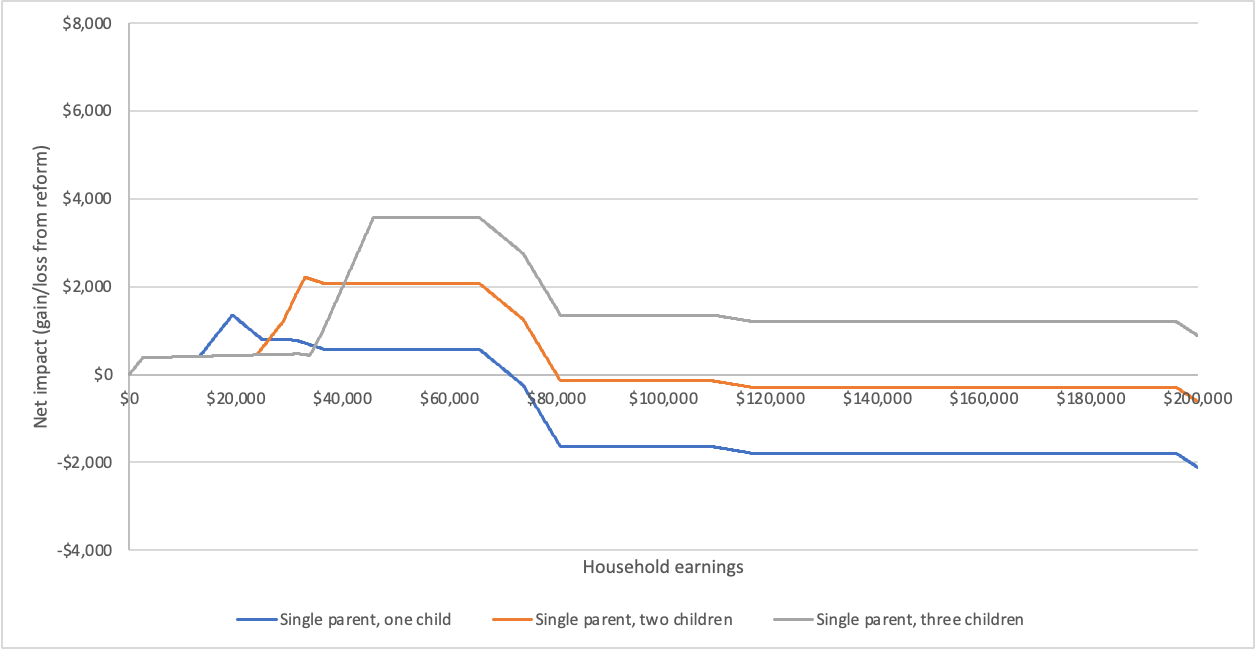

Figures 2-4 below show the net impact of eliminating HoH status and replacing it with an expanded CTC worth up to $3,500 per child – with differing refundability provisions – for single parents making up to $200,000 with one, two, or three children.

Figure 2: Net impact of TCJA style reform

Figure 3: Net impact of Rubio-Hinson style reform

Figure 4: Net impact of Smith-Wyden style reform

Single parents with one child earning less than $73,100 would be net winners or held harmless under all three reforms. That threshold rises to $80,000 for those with two children, at which point benefits are moderately lower overall. Single parents with three (or more) children are better off across the board. This stems from the nature of refundable tax credits, which tend to be more valuable to lower-income households, relative to HoH status, which tends to be more valuable to higher-income households. To put these thresholds into perspective, about 85% of HoH filers earned less than $73,000 in 2021.

For the vast majority earning less than $73,100, the positive net impact varies substantially across the three reforms depending on how they structure the phase-in rate. The TCJA style and Rubio-Hinson style reforms both provide more generous benefits to lower-income single parents. The net increase in the maximum ranges from about $1,000 to $1,200 per child depending on earnings and number of children.

The Smith-Wyden reform is similar to the other reforms for those with one child. Still, the shift to a per child phase-in makes it substantially more generous for single parents with two or more children – particularly those working full time at the federal or state minimum wages.

Looking ahead to 2025

While much of the debate going into 2025 will focus on which TCJA provisions to make permanent and which to let expire, Congress should also consider options for building on the aspects where bipartisan consensus is that reforms moved in the right direction. Nobody would doubt that our current child tax credit is an improvement over our more complex pre-2017 system of distinct tax credits for children and exemptions for dependents.

By building on these reforms with a further consolidation of family tax benefits, which eliminates HoH filing status and redirects the savings to a more generous and inclusive child tax credit for parents and families, Congress can enact bold, common-sense changes that reduce marriage penalties, overall costs, and complexity for families.