Head of Household (HoH) filing status provides single individuals caring for dependents–often children– with broader tax bracket thresholds compared to single filers, along with a more generous standard deduction ($22,500 in 2025, versus $15,000 for single filers). However, as we have previously discussed, no equivalent filing status exists for married couples with children, leading some Republicans to argue that it creates a marriage penalty. Single parents who marry can lose substantial tax benefits each year, discouraging marriage from a financial standpoint.

This has led some Republicans to propose eliminating HoH filing status. By requiring single parents to file as Single, the marriage penalties would be removed. However, this would also result in higher taxes for working- and middle- class single parents. Other Republicans have shown little appetite to follow through on these proposals given the tradeoffs.

A potential solution is to phase out or eliminate HoH filing status while expanding other tax benefits to ensure single parents are not worse off financially. One way to achieve this would be to use the Child Tax Credit (CTC) as a vehicle for reform. There are several ambitious proposals that could eliminate the HoH status while significantly increasing the CTC to offset any negative impacts on single parents.

The impending expiration of the Tax Cut and Jobs Act family provisions presents an opportunity for further reforms. However, it has become increasingly evident that Congress will face significant fiscal constraints that limit the scope of possible reforms. Increasing the maximum CTC to $3,000 or $3,500 per child is no longer feasible. Instead, Congress has shown interest in raising the credit to $2,500 to offset the erosion of its real value due to inflation over the past five years.

Congress can still take a step in the right direction

If Congress moves forward with increasing the CTC from $2,000 to $2,500 per child, it would provide space for incremental reforms to reduce marriage penalties by reducing the HoH standard deduction from $22,500 to $20,000 as part of the same tax package.

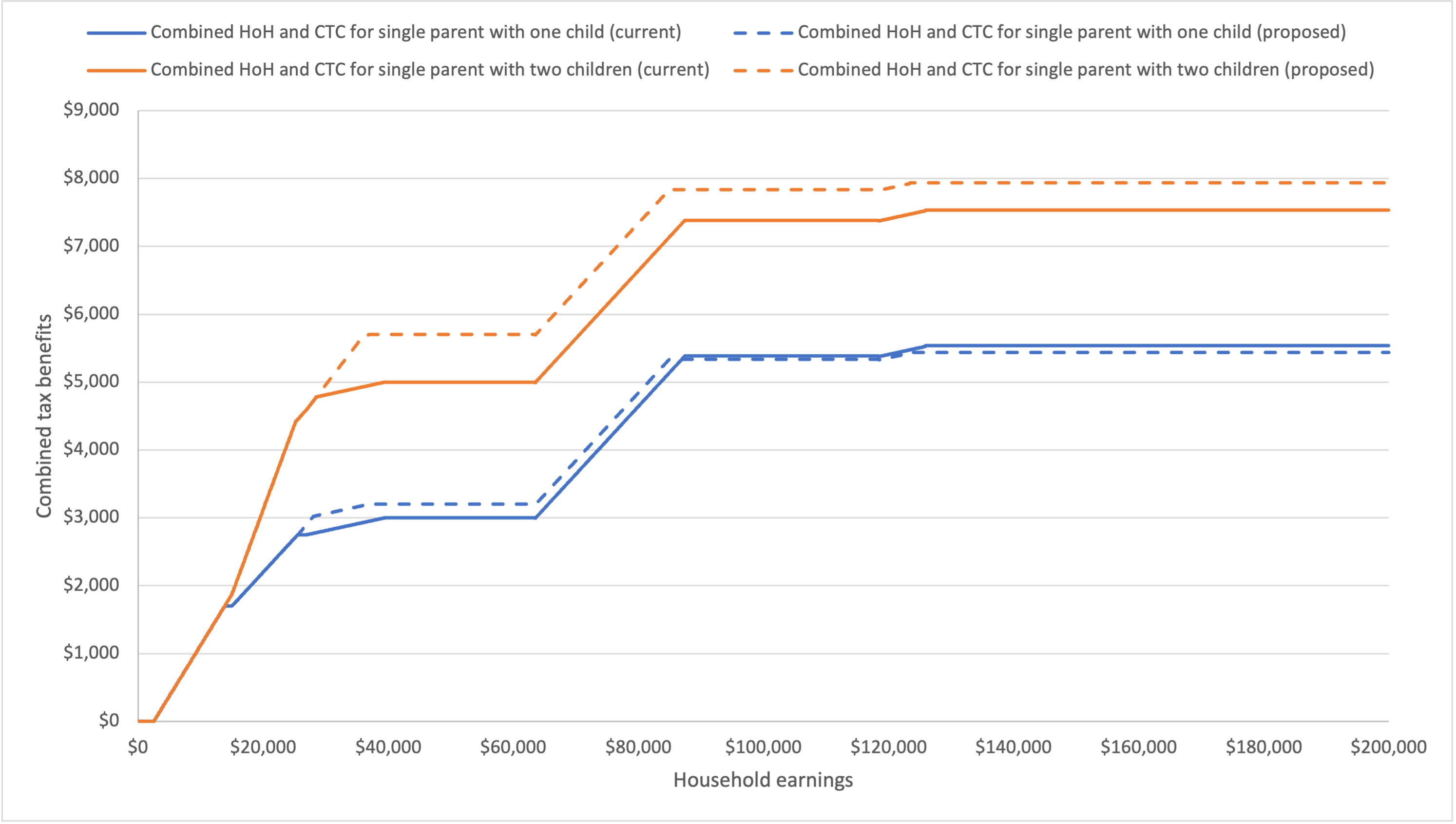

Figure 1 illustrates the net impact of reducing the value of the HoH standard deduction (while leaving the brackets unchanged) in tandem with an expanded CTC worth up to $2,500 per child (while leaving refundability provisions unchanged) for single parents making up to $200,000 with one or two children.

Figure 1: Combined HoH and CTC value under current and proposed reforms

Under these reforms, lower- and middle- income single parents on net are either unimpacted or better off overall. The savings from reducing the HoH standard deduction also help offset the cost of the expanded CTC. Most of the increased benefits (and net costs) are associated with middle-income married parents.

These reforms would also reduce marriage penalties for single parents. Table 1 illustrates this reduction in marriage penalties using a hypothetical example of two parents, each earning $30,000. It compares what happens to their combined head of housing filing status, child tax credit, and earned income tax credit (EITC) if they choose to get married under current law versus under the proposed reforms.

Table 1: Marriage penalties under current and proposed reforms

In both scenarios, the couple faces significant marriage penalties–particularly in relation to the EITC –but the proposed reforms reduce these penalties by $250 for this family. Given the growing class divide in marriage, any reduction in barriers facing working-class families should be a welcome step in the right direction. If Congress does decide to increase the value of the child tax credit, it should seize this opportunity to also address and reduce marriage penalties simultaneously.