President Biden is fond of saying, “Don’t tell me what you value, show me your budget, and I’ll tell you what you value.” Illinois policymakers recently had the opportunity to transform how they support children and families with a state child tax credit (CTC). However, this opportunity depended on getting the policy details right, as we recently outlined. Unfortunately, the compromise that emerged fell short, getting key details wrong.

In February, Governor Pritztker proposed a so-called CTC for children under three years old. However, it was so narrowly-tailored that it excluded the most impoverished children and middle-class families. In fact, the proposal resembled an Earned Income Tax Credit (EITC) boost for the youngest children rather than a true CTC.

In contrast, the Illinois legislature considered a bill proposing a “fully refundable” child tax credit worth up to $300 per child. This credit would be structured similarly to what we saw with the federal CTC in 2021, which halved child poverty that year. As proposed, the full credit would be available to single parents earning up to $50,000 and married parents earning up to $75,000; with a gradual phase-out as family income rises. This version would position Illinois as the 12th state to implement such a policy to reduce child poverty and support middle-class families.

While this proposal is sound in theory, it came with a steep price tag. Citing cost concerns, budget negotiators moved away from this version. The final bill was a more generous version of Governor Pritzker’s original proposal, adding an additional EITC worth 20% of the existing state EITC for children under 12 years old (rising to 40% next year) on top of the state’s existing EITC (which is stacked on top of the federal EITC). This compromise would cost $50 million in FY25 and $100 million in FY26 – more expensive than Pritzker’s original $12 million proposal but much less costly than the legislature’s initial proposal.

Budget negotiators correctly trimmed their original proposal’s cost when faced with budget constraints. Still, there was a much better way to spend $50 million on children than adding another complicated EITC–which excludes the poorest children and is rife with work and marriage penalties–to the state tax code.

Fixing what’s there is the better option

Illinois could have looked to New England for cost-effective reform models. In 2021, Massachusetts converted its tax exemption for children under 12 into a fully refundable child tax credit. Similarly, Maine converted its dependent exemption into a nonrefundable child tax credit in 2018 before making it fully refundable this year. The changes demonstrated that state policymakers can make relatively minor and inexpensive tax policy tweaks that have a transformative impact on families. In both cases, previously excluded low-income families could finally claim these tax benefits for the first time.

Illinois did not need to reinvent the wheel (or the EITC in this case). It just needed to take a cue from Massachusetts and Maine by similarly converting the state’s dependent exemption into a fully refundable child tax credit. The state’s dependent exemption is already worth up to $137 per child–but only for families who earn enough to claim it. The lowest-income families receive little or no benefits.

How would converting exemptions into fully refundable credits get much more bang for the buck? As we explain in our State of our Families report, tax exemptions reduce the amount of income that is subject to taxation. The amount of the benefit is the amount of additional income that would otherwise be taxed at the highest marginal tax rate. The effective value of the exemption depends on the tax rates facing the family. In this case, Illinois’ dependent exemption allows families to exempt $2,775 of income for each dependent. Under Illinois’ flat 4.95 percent personal income tax, each eligible dependent would be worth up to $137 ($2,775 x 4.95%). But it is only valuable to those with enough earnings to be subject to enough income tax liability to claim the full exemption.

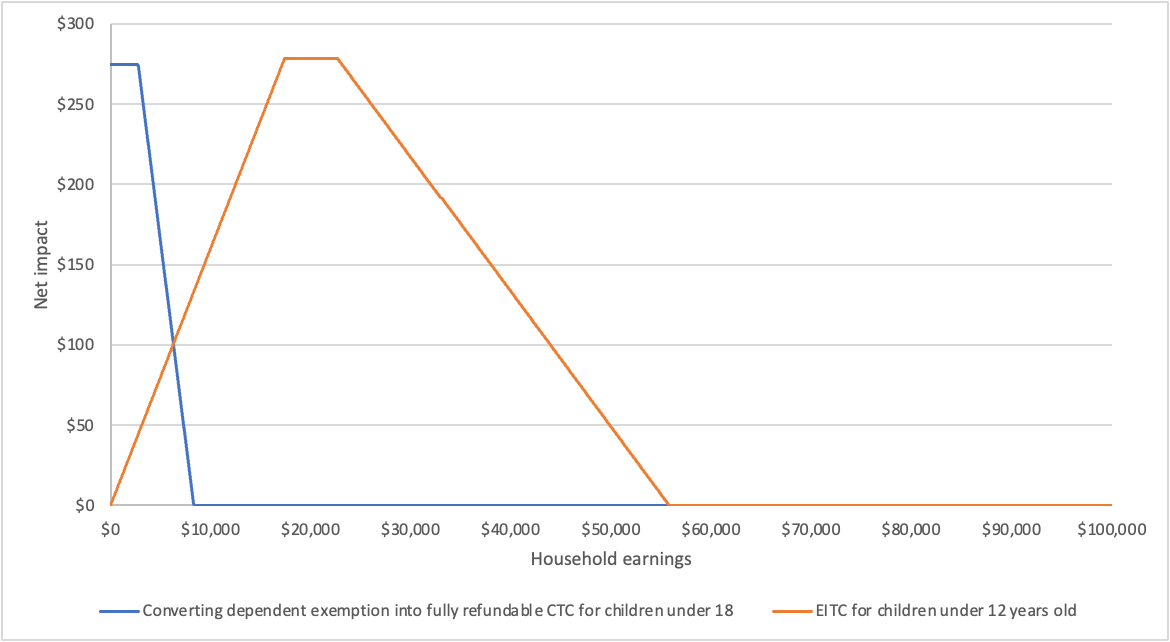

According to PolicyEngine, an open-source policy simulator, converting the state’s dependent exemption into a fully refundable child tax credit for children under 18 would cost about $50 million this year and reduce deep poverty among children by 11%. Concentrating the expansion of benefits on those with the lowest incomes allows it to reach a broader age range. Figure 1 looks at the net impact of these changes relative to what was enacted for a single parent with two children.

Figure 1: Net impact of reforms for a single parent with two children (2024)

The new law provides the most to families in the $17,000-$23,000 range–the families that were already receiving the full benefit of the dependent exemption. If, instead, they had converted the dependent exemption into a fully refundable CTC, the new benefits would be concentrated entirely on families making less than $10,000–the most vulnerable children in Illinois.

Illinois policymakers did not take the latter path but, if they had, it would have created a nearly universal CTC similar to what Maine enacted last year. That missed opportunity would have been more progressive, fiscally responsible, and made the tax code much simpler for families–a much more accurate reflection of Illinois’ values regarding children and families.