This piece is part of a series of briefs looking at specific state proposals for family tax benefit reforms based on a larger Niskanen report, The State of our Families: Child and Dependent Tax Benefits in the States. You can find other state briefs here.

Only three states in the country levy an income tax on residents but provide no general income tax exemption or credit for children–and Connecticut is one of them.

Governor Ned Lamont (D) temporarily changed that last year when he worked with the legislature to pass a one-time fully refundable $250 child tax credit – for up to three children – available to most families. Still, proposals to extend the CTC by making it permanent were conspicuously absent from the governor’s budget this year. In response, State Senator Martin Looney (D) introduced SB771 to make last year’s CTC permanent.

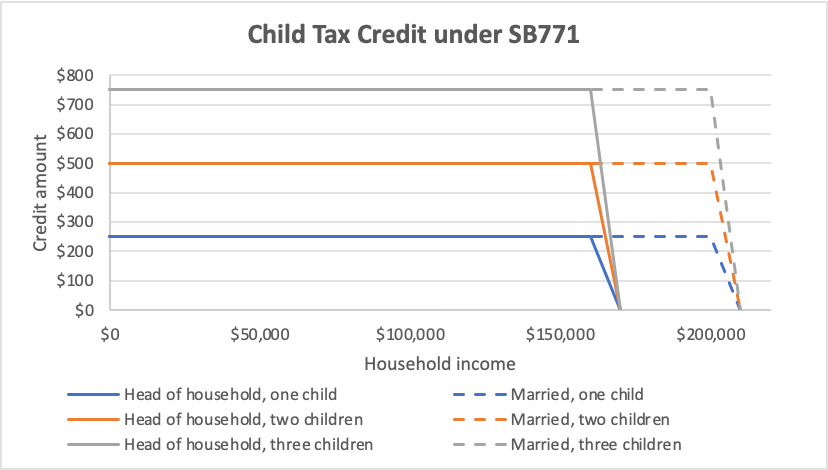

SB771 would (re)introduce a fully refundable child tax credit worth $250 per child, and still cap at three children ($750 maximum per household). The credit begins to phase-out at a relatively high-income threshold ($160,000 for single heads of household; $200,000 for married couples) at a rate that increases with each child, so the credit is reduced to $0 for any family earning $10,000 over the threshold. Figure 1 illustrates the benefits across families.

Figure 1

Benefits

Given that Connecticut is working from scratch, any tax benefit for children is better than nothing. That low-bar notwithstanding, the structure of Senator Looney’s proposed CTC is particularly welcome. Making it fully refundable with a relatively high phase-out threshold ensures that all low- and middle-income families can claim the full credit to supplement their income and help with the cost of raising children.

What’s more, making the credit permanent enables families to consistently plan for their budgets each year in the future.

Drawbacks

As proposed, the bill has three substantive drawbacks related to work, marriage, and large family penalties.

The suggested phase-out threshold and rates are structured in a way that may sometimes penalize marriage and larger families. The threshold is higher for married parents than single parents, but the best practice is to double it to minimize marriage penalties. Provisions that increase the phase-out rate with each additional child (2.5% for one, 5% for two, 7.5% for three or more) exacerbate this problem. The credit’s relatively high phase-out threshold does insulate most families, but this nonetheless remains a problem.

Also problematic is the proposal’s capping the number of eligible children at three, which penalizes larger families who face the same costs of raising additional children.

Finally, like New Mexico’s recent proposal, the last significant drawback is less about what this bill would change and more about which aspects of the existing credit system it would leave intact. Connecticut currently has no child tax credit, but it does have one of the most generous Earned Income Tax Credit (EITC) state matching rates in the country. Connecticut’s 30.5% state match translates into a $2,266 maximum credit for families with three or more children, stacked on top of the federal EITC structure.

While providing a much-needed supplement to low-income working families with children, this structure exacerbates major work penalties for families in the phase-out range of the EITC trying to break into the middle class. Families above a certain income threshold ($21,560 for single parents; $28,120 for married parents) lose about 15-21 cents for each additional dollar they earn. If they are also receiving Supplemental Nutrition Assistance Payment (SNAP) benefits, they may lose another 24-36 cents for each additional dollar they earn.

The result is an implicit marginal tax rate of 39-57% on each additional dollar many families earn, creating a significant barrier to upward mobility. On top of this, Connecticut’s state EITC adds 5-6%. Also introducing a universal child tax credit does not exacerbate these penalties – but it certainly doesn’t do anything to reduce them.

Improvements

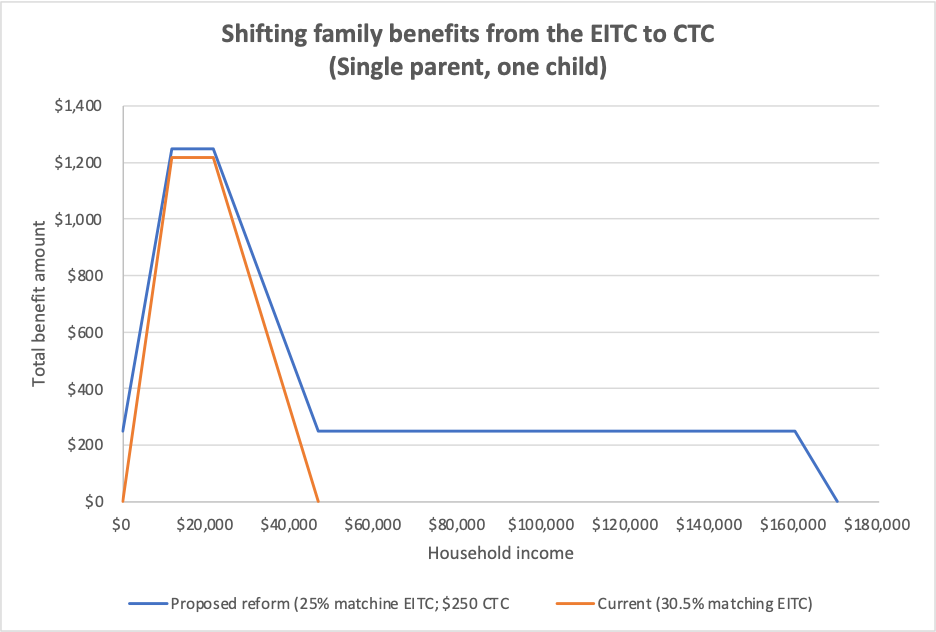

Historically, expanding state EITCs was seen as a viable alternative to introducing a fully refundable state CTC. It had clear drawbacks (e.g., it excluded the poorest children and exacerbated the work penalties discussed above) but was accepted as better than nothing. That is clearly no longer the case in Connecticut – and policymakers should reform their tax credit system accordingly. The best way to do this is by decreasing the state EITC in proportion to the value of the new state CTC to ensure that all families are kept whole or made better off under the reforms. Figure 2 illustrates what this would look like for a single parent with one child.

Figure 2

In this scenario, reducing the state EITC match from 30.5% to 25% in conjunction with introducing a $250 child tax credit would make all families better off than they are now while reducing work penalties and the overall cost of the reforms. The savings from this reform could be used to remove the CTC’s three-child cap or eliminate the phase-out to fix work/marriage penalties on the higher end and make the credit truly universal.

For too long, Connecticut has been a laggard among states regarding family tax policy, so SB771 would be a step in the right direction. Still, more comprehensive reforms would turn Connecticut into a leading tax credit innovator among states. That should be something all Nutmeggers can get behind.